SEA Ltd: The Prodigal Son (2Q Deep-Dive)

Positive 6M23 Ecom Contribution + Fortress Balance Sheet + 11% TAM Growth + 12.5x Earnings Multiple. Is Mr Market stupid?

When CEO Forrest Li announced SEA Ltd’s Q2 results in mid-August, he was probably expecting a pat on the back. After all, the team at SEA Ltd had slogged through fire and brimstone over the past year trying to bring the company back to profitability. And to their credit, they had actually successfully done so against all odds, as evidenced by the opening statement of their 23Q2 results:

“In the past couple of quarters, we have not only achieved self-sufficiency, but also demonstrated the profitability of our model and our ability to manage fast and significant shifts in operational focus as we see fit. Given this, we have strengthened our execution capabilities and increased the stickiness of our ecosystem. We believe we are now on firmer footing to better serve our communities.”

“Meanwhile, the economies of our region have remained resilient, and we are excited to see recent ecosystem developments in the growth of diversified user engagement through live streaming, short form videos, and affiliate programs. Such developments offer us further opportunities to grow and expand our long-term profitable addressable market. Given these positive developments and trends, we have started, and will continue, to ramp up our investments in growing the ecommerce business across our markets. We believe that the efficiency gains and stronger footing we have achieved through our past efforts have further strengthened our ability to invest efficiently in growth. As we reaccelerate investments in growth, our strategic focus to build cost leadership and continually improve user experience remains key to our long-term success.” (emphasis mine)

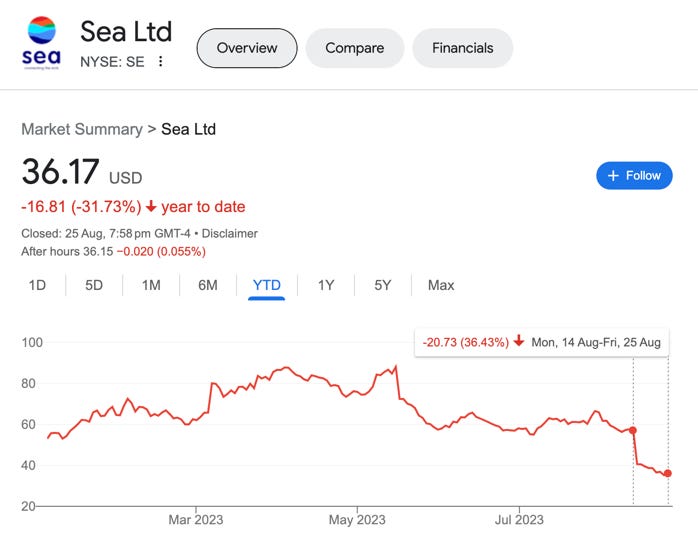

Notice my emphasis above in italics? The CEO’s statements about restarting investments in growth were what caused SEA 0.00%↑’s share price to collapse by nearly -40% overnight — which is where it has pretty much stayed until today.

Ironically enough, a couple of stock commentators who had written about SEA’s latest 2Q results actually had some pretty good things to say about them. And as I’ve actually covered them before in a previous stock report, I had some context to springboard into their latest quarter results. To my utmost surprise, I actually liked what I saw — this article will go into my findings.

Chapters:

Shopee — 40% market share in SEA’s (The Next China’s) E-Commerce

Valuation: 12.5x Earnings Multiple? (50% Margin of safety x2)

Shopee — 40% market share in SEA’s (The Next China’s) E-Commerce

If you’ve read my aforementioned SEA Ltd stock report, you’ll know that I didn’t find its share price particularly undervalued at the time — when it was still trading at $80. At the end of that report, I alluded to potentially considering it undervalued if its share price ever fell to $35 — which according to my estimate implied a normalized PE ratio of ~20x. If it did, that wouldn’t be a bad valuation for what was by far the largest retail e-commerce) operation with 30-50% market share in the relatively high-growth Southeast Asian (SEA) economic bloc — which I’ve described as The Next China — where the regional e-commerce sector sports a TAM growth of 11.5%. 1

In Nov 2022, SEA 0.00%↑ actually fell all the way to just above $40 — but never fell below it. I promptly forgot about it until last week when their share price cratered -40% overnight to $38 or so — where it has continued its precipitous slide to-date.

This was all the more surprising since SEA’s 2Q results were actually in significantly better shape than they were this time last year. At the time, SEA was still bleeding cash from multiple orifices in its business model — with the most egregious being its e-commerce segment Shopee, which at its peak had Sales & Marketing expenses amounting to 70% of e-commerce segment revenues!

As I had already analyzed them before, I immediately knew where their pain points were and thought it was worth a quick 30 minute update — without actually expecting much. Imagine my surprise when I realized that things were actually so much better today! Much of the reasons for their earlier going concern risks have vanished, and as the CEO alluded to their financial results amply demonstrate that they have truly become self-sustainable — we will dive into this below.

11.5% regional TAM growth: This is very much the same business from last year after graduating from rehab, and the same business from two years ago minus all the cash flow excesses. They still have by far the largest e-commerce operation in the relatively high-growth Southeast Asia region with 30-50% market share depending on country (TAM growth: 11.5%) — and most retail industry analysts will understand how winning in the retail industry boils down to having the greatest economies of scale. 2

No moats, no problem: Given SEA’s dominant market share in an industry that is likely to demonstrate similar LT tailwinds as the past decade of China’s e-commerce sector, I would argue that SEA Ltd doesn’t need to be a ‘wonderful business’ with huge moats to justify its current valuation. Neither Walmart nor Amazon are structurally ‘wonderful businesseses’ — they simply had the muscle to push their way through competitive forces via having the greatest economies of scale.

And while there remains an outsized level of regional competition in SEA’s windshield (e.g. Lazada, Tokopedia, Grab), I would make the case that as long as its e-commerce segment Shopee can maintain its dominant market share, the largest e-commerce operation in this high-growth economic bloc can justify my earlier estimated forward PE of <20x. As we shall see later, the actual earnings multiple today is significantly lower.

The Prodigal SEA Returns

In this section, we’re going to be focusing exclusively on analyzing SEA 0.00%↑’s e-commerce operation, Shopee. In essence, the thrust of this analysis is to determine whether Shopee alone is capable of carrying the entire SEA Group’s current market cap of ~$20B.

I won’t be doing a deep-dive of their other two business segments — the high-FCF video game publisher Garena (Digital Entertainment or DE) & the nascent digital wallet/bank initiative SEAMoney (Digital Financial Services or DFS) — because the former is a relatively ex-growth cash cow while the latter’s business is still nascent. If you’d like more insight into their E-commerce segment, I did a deep-dive in my previous SEA stock report.

As SEA has only been profitable (before extraordinary items) for the past 2 quarters, this analysis shall focus on analyzing their past 2 quarters (i.e. 6M23) as a proxy for what their normalized profits could look like. The fruit of SEA’s profit-focused efforts only began to bring them back into the black in 1Q23 (despite them having started early last year), so I think this is as good a starting point as any to begin our profitability analysis.

P&L (E-Commerce): 2Q Revenues, GP & Contribution

The first surprise lies in their E-commerce segment revenues. Cursory scuttlebutting of Shopee’s website in different Southeast Asian countries (you can use a VPN to spoof your country) revealed that Shopee has been significantly scaling back their free shipping & discount subsidies to customers over the past year — they only recently restarted this a couple months ago.

On top of that, Shopee has also exited several global markets over the past year such as France, Poland, Latin America (ex-Brazil) and India — these were all new markets and still unprofitable, but no doubt contributed to revenues of the E-commerce segment.

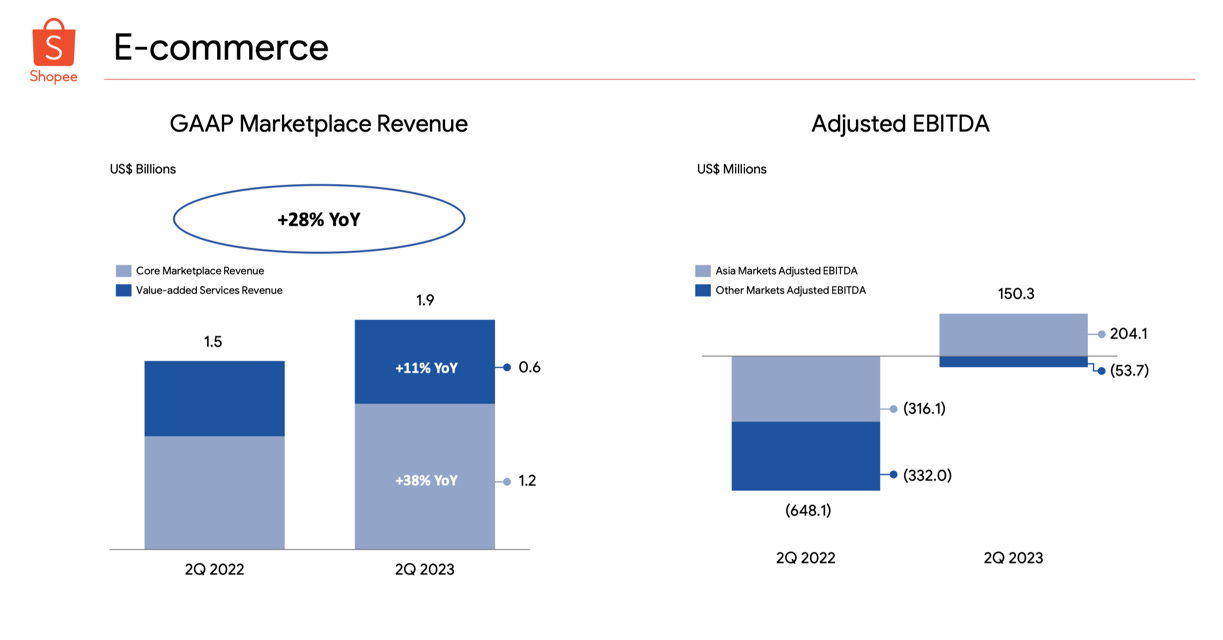

Hence, it was news to me when I saw that their E-commerce segment revenues actually increased by a whopping 210% YoY — from $2.0B in 6M22 → 4.2B in 6M23:

(click this footnote3 to see how I estimated the chart below differently from as reported)

This implies that my earlier fears about Shopee wholly subsidizing e-commerce revenue growth with customer discounts (at the expense of profits) might have been unfounded. While there was certainly some truth to that early-on (I discussed this in my previous SEA stock report), the past 2 quarters have also demonstrated that Shopee has already achieved sufficient critical mass to continue growing e-commerce revenues at low-to-mid double-digit rates (e.g. 20-40%) even without the help of customer subsidies. It may not be the triple-digit YoY growth rates that 2021’s investors were expecting, but 20-40% organic YoY revenue growth is nothing to scoff at — especially at SEA’s current valuations.

Perhaps even more surprisingly, both of SEA’s e-commerce segment GP and Contribution (GP - S&M exp) have taken a dramatically positive turn YoY. If you’ve read my earlier SEA stock report, you’ll know why I find this development to be surprising — and for the uninitiated, I’ll explain below.

Focus on GP, ignore NP: Essentially, what SEA and many other SaaS firms had been trying to claim during the pandemic tech bubble was that their rapidly improving Gross Profits mitigated any concerns around their rapidly deteriorating Net Profits. Their rationale was that this was similar to early Amazon’s profit performance during the late 2000’s, as I’ve discussed before in this article. However, the nature of this divergence between Gross Profits and Net Profits could not have been any more different between early Amazon and SEA.

Early Amazon’s vs. SEA’s economics: As I’ve discussed in my early Amazon article, the reason behind why early Amazon was sporting improving Gross Profits despite declining Net Profits was because they were pulling forward their warehouse CAPEX from future years — by recognizing LT warehouse leases in the form of Fulfillment expenses many years in advance of actual required capacity (fixed costs). Whereas this was not true in SEA’s case — the divergence between their Gross Profit and Net Profit trajectory was almost solely due to their outsized Sales & Marketing spend, which as you might have guessed was going towards customer subsidies of free shipping & discounts (variable costs).

This meant that early Amazon’s flat Net Profit was due to expenses that were actually CAPEX (fixed costs) in nature — which could help improve their future operating leverage as their economies of scale grew. Whereas in SEA’s case, their outsized Sales & Marketing spend was purely variable cost in nature — and once they turned off the marketing spigot, all that excess demand growth (i.e. revenue growth) would dry up.

Accounting Tricks?: Given the aforementioned context, it becomes easier to understand why I was so surprised by Shopee’s rapid GP and Contribution YoY improvements.

Initially, I harbored the suspicion that Shopee’s GP wasn’t actually improving organically — rather they had simply been playing accounting tricks by shifting their e-commerce logistics expenses from COGS (above GP line) to S&M exp (below GP line). This would have had the desired effect of boosting GP on paper, without actually improving NP or the true business economics.

Shopee could have done this by recognizing shipping fees received by customers under Revenues — but given that they were subsidizing customers with free shipping discounts, they could have recognized shipping expenses under Sales & Marketing expenses (below GP line) instead of under COGS (above GP line). If this were true, it implies that they were playing accounting tricks with their GP — and since their Sales & Marketing expenses amounted to ~70% of their e-commerce segment revenues, Shopee’s deteriorating Net Profits actually represented their true business economics (unlike Amazon).

While I have no confirmation that SEA actually did this, that potential red flag was enough to put me off — especially since their $80 share price at the time of my previous SEA stock report was implying a normalized PE ratio of ~37x.

No Accounting Tricks: However, Shopee’s (i.e. e-commerce segment) improving YoY segment GP and Contribution seems to imply that they had not been relying on accounting tricks to boost their GP after all. If they had, the logistics expenses that had been shifted from COGS to Sales & Marketing expenses (as described above) would simply be reversed back, thus reinflating COGS and normalizing GP as they scaled back on their free shipping customers subsidies. And since their e-commerce revenues increased rather than decreased YoY, the attendant increasing logistics expenses would have made it harder to reverse any accounting tricks played with GP.

E-commerce Contribution Turnaround: In any case, the massive improvement in Shopee’s e-commerce segment Contribution is huge — going from almost negative -$1B → positive $1.2B. While this positive trajectory may change going forward given their recent commitment to refocus on growth over profits, investors can take heart that SEA’s E-commerce business unit is actually capable of being self-sustaining/profitable if they so choose.

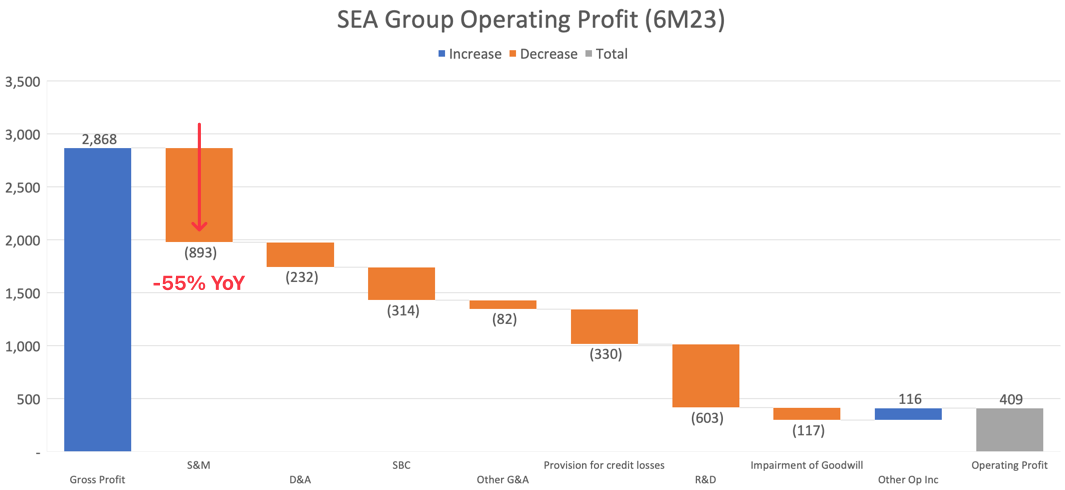

P&L (Group): 2Q Operating Profit & Adjusted EBITDA

In this section, we’ll switch our attention from SEA’s e-commerce segment (i.e. Shopee) to the Group level — since the company doesn’t disclose a full OPEX breakdown at the segment level.

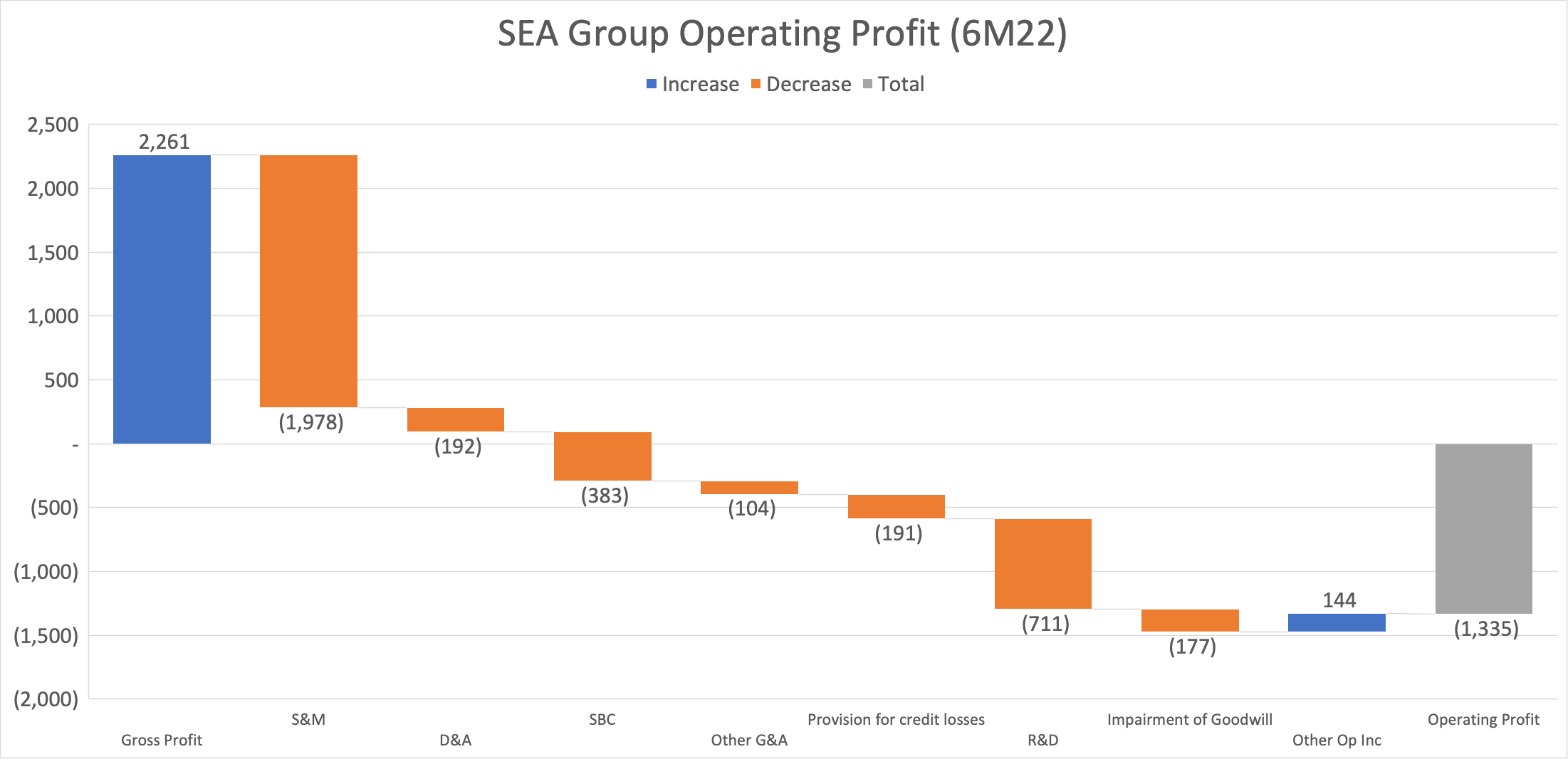

OPEX: What I’d invite readers to do is to compare Group OPEX performance between 6M22 vs. 6M23. As we can see in the charts above, there were really only three large OPEX items which materially impacted Operating Profits in both years — Sales & Marketing (S&M), Share-based compensation (SBC) and Research & Development (R&D) expenses.

SBC expenses: Some might argue that SEA’s management is getting away with murder paying themselves roughly the same in SBC this year despite deteriorating post-bubble performance. However, I personally wouldn’t nitpick on this, since at the end of the day reducing SBC isn’t going to move the needle much on their Operating Profits.

R&D expenses: Why does a primarily e-commerce business need to spend 9.8% of 6M23 revenues on R&D? A quick look into their FY22 10-K reveals that this is largely spent on headcount, and my channel checks revealed that employee salaries for software engineers traditionally fall under the R&D accounting category. So these are likely just basic employee salaries.

S&M expenses: This leaves us with only their Sales & Marketing expenses remaining to worry about. As we can see above, there was a sharp -55% YoY drop in their S&M exp in 6M23 — falling from 34% of FY22 Group revenues → 15% of FY23 Group revenues. At the E-commerce segment level, the equivalent segment S&M exp fell from 42% of FY22 segment revenues → 17% of FY23 segment revenues. Coupled with higher revenues, the massive reduction in S&M exp was singlehandedly the biggest OPEX item in 6M23 which contributed to the massively improved 6M23 Operating Profits.

Net Profit & Adjusted EBITDA: Beyond the OP line, there were some relatively insignificant cost items like taxes which didn’t materially affect Net Profit (6M23: $409M).

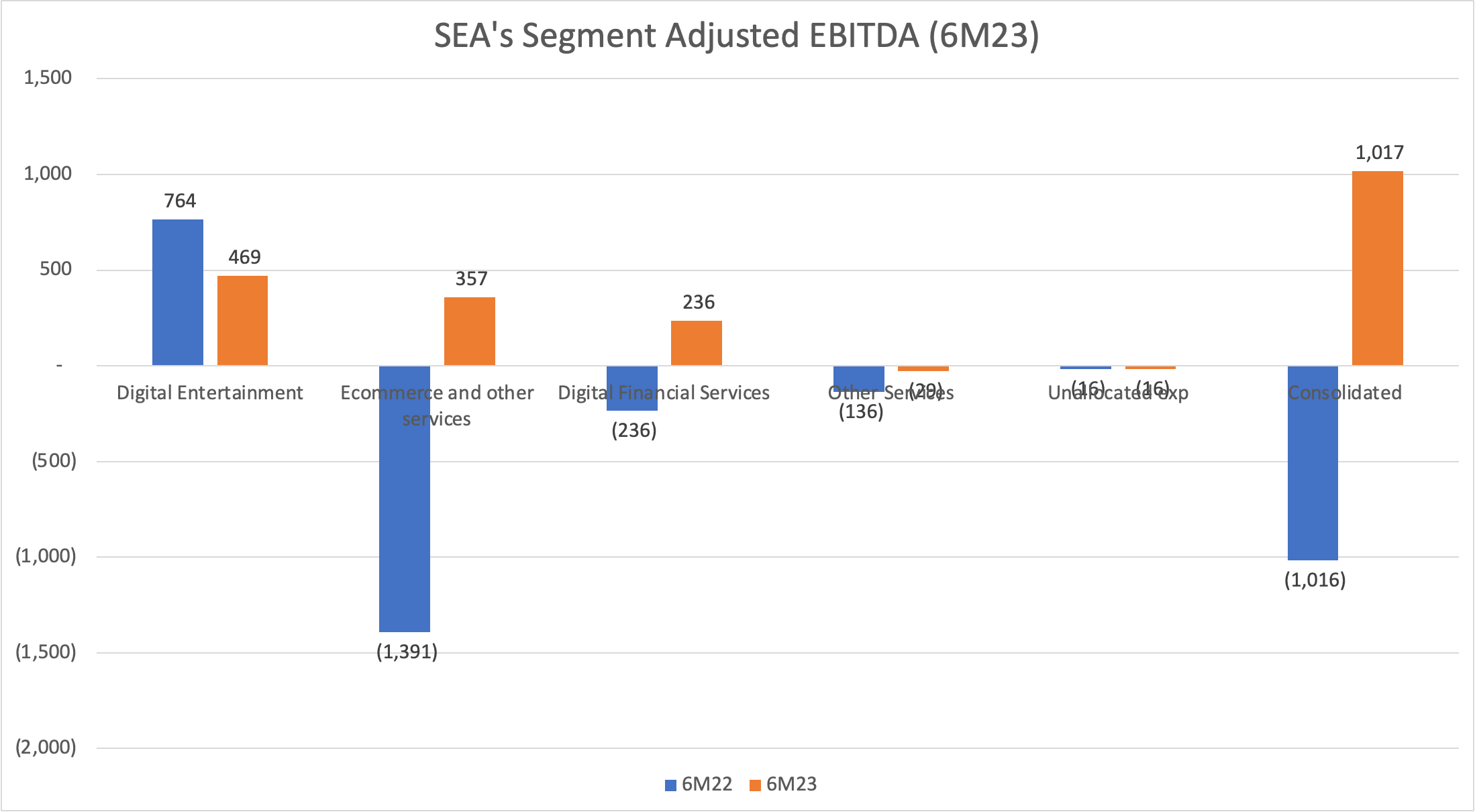

Management also presents the company’s Adjusted EBITDA as their preferred KPI — which mostly just backs out Depreciation & Amortization and Share-based compensation (SBC) from Net Profit. Ultimately, it doesn’t really change the YoY performance narrative of their Operating Profit. I’ll just leave the Adjusted EBITDA figures in the chart below in case anyone is interested:

Cash Flow Statement (2Q)

I want to talk about SEA’s 2Q performance of their Cash Flow Statement (CFS) first before their Balance Sheet, as it relates directly to their P&L performance. As we can see above, the company only provides an abridged version of their CFS in their quarterly reports. However, that’s good enough for us to validate their FCF against their reported profits.

As we can see above, the Group reported positive $1.2B worth of OCF in 6M234 — a stark contrast from negative -$1.2B in the previous year (6M22). As their Depreciation & Amortization expenses was only ~$0.2B, this brings their estimated 6M23 FCF to ~$1B — or an annualized FCF of $2B for FY23.

Some readers might be shocked to see their outsized -$3.8B of negative Investing Cash Flows… but as the disclosure reveals, there’s actually nothing to worry about. The vast majority of it ($3.46B) were simply placements into short-dated instruments for better cash yield management.

I’m actually not quite sure why they described such Investing Cash Flows the way they did, since we can observe on their balance sheet below that only $1.31B of that $3.46B was placed into Short-term investments — the remaining $1.93B was actually invested into Long-term investments:

But as we can see above in the notes of their FY22 10K under Note 7: Long-term investments, there is actually nothing alarming here either— Non-current HTM securities only make up <5% of their total investments.

Balance Sheet (2Q)

Finally, we come to SE's Balance Sheet. For the sake of brevity, I’m just going to highlight the parts that matter and skip the rest.

Assets: On the Asset side of their balance sheet, the only thing really worth highlighting is that in addition to the $5B of Cash & cash equivalents which we also saw in their CFS above, they also have an additional $2.1B in ST investments and $3.2B in LT investments. This brings their total liquid assets to $7.1B, and their Total Cash + Investments to $10.3B. Even if we deduct the Equity securities (ST+LT), Equity method investments (LT) and Investments carried at FV (LT) as seen in their disclosures above, their Total Cash + Investments available to tap in an emergency stress scenario still amounts to a whopping $9.5B at current market values.

Liabilities: On the Liabilities side, adding up all of their Operating lease liabilities, Borrowings and Convertible notes only results in a Total Gross Debt of $4.5B. This implies that their Net Cash position is $0.5B (5 - 4.5); they have a “Net Liquidity Position” of about $2.6B (7.1 - 4.5); and their “Total Funding Capacity” is about $5B (9.5 - 4.5) available to tap in an emergency stress scenario. That is a very healthy liquidity buffer to have on their Balance Sheet relative to their annualized FY23 FCF of $2B (6M23: $1B).

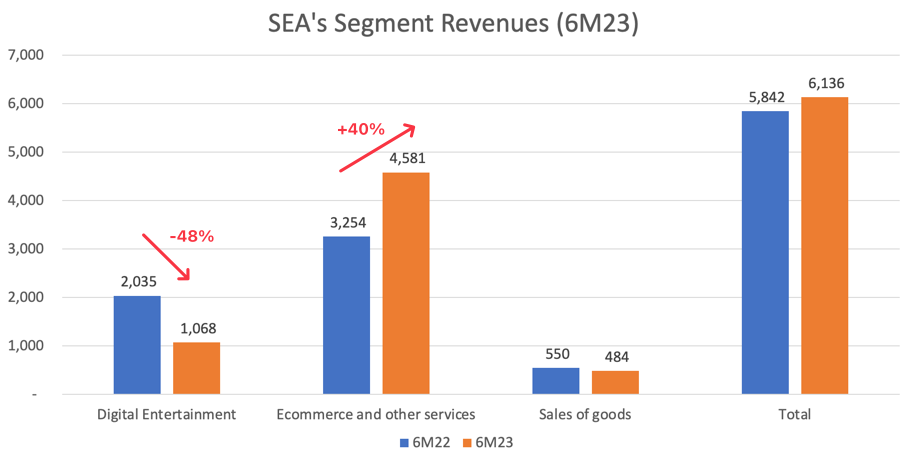

One last thing worth mentioning about SE’s balance sheet is that the two Liability items Escrow payables and advances from customers + Deferred revenue (ST+LT) actually fell slightly in 2Q23 relative to FY22. This is likely due to the pretty steep -48% decline in their Digital Entertainment segment activity being approximately offset by the +40% YoY increase in their E-commerce segment activity — both segments contribute to SEA’s balance sheet float.

Valuation: — 12.5x Earnings Multiple? (50% Margin of safety x2)

Finally, we come to SE’s valuation. As I’ve mentioned in my previous SE stock report, my earlier estimate was that a share price of $35 would imply a normalized PE ratio of ~20x (paid subscribers: check out the full calculations here). Since SE’s current share price is roughly in $35 territory, I’m not going to reinvent the wheel and will just use that 20x multiple as my starting point for this valuation analysis.

“Levered” Enterprise Value $25B: As we saw above, their Net Cash position is $0.5B. Some readers might be tempted to deduct my aforementioned “Net Liquidity Position” of $2.6B or “Total Funding Capacity” of $5B respectively from their market cap of $20.5B to arrive at gobsmacking valuations — but I would prefer to be conservative and assume that these cash reserves will eventually be used for growth investments. In fact, I’ll even go one step further and add their Total Gross Debt of $4.5B to their current market cap of $20.5B for a “Levered Enterprise Value” of $25B (both equity + debtholders).

That’s the multiple numerator — but what about the earnings denominator? In my earlier SEA report, I used a LT normalized earnings assumption of $1B to arrive at my previously estimated 20x normalized PE (assuming a share price of $35, or ~$20B market cap). Given that SEA posted a 6M23 Net Profit of $409M, I’d say that this assumption is conservative given that annualized FY23 earnings are already $818M (409 x 2) — keep in mind that SE is currently operating in trough-cycle conditions.

E-commerce growth: And lest we forget, SEA’s e-commerce segment is still growing at a relatively torrential pace. Not only does it have the greatest economies of scale amongst its peers in a commoditized industry with 30-50% market share, the Southeast Asian E-commerce industry’s TAM growth itself is projected to be 11.5% for at least the medium-term. Call it 10% TAM growth for simplicity — that is unbelievably massive for an entire industry’s growth, relative to the prevailing macro narrative of declining global productivity going forward.

E-commerce norm. earnings $2B : Putting this all together, I don’t see why SEA’s E-commerce segment cannot eventually report $2B in LT normalized earnings into perpetuity. In fact, I find it hard to believe that it cannot eventually do so after everything we’ve discussed. Of course, going concern is a potential obstacle before it reaches that stage — but as we’ve covered in the previous section, the company has a fortress Balance Sheet which pretty much eliminates all cash flow or bankruptcy risks.

High-growth DFS: On top of that, we still haven’t touched on the potential growth contribution of SEA’s other two segments — Digital Entertainment (DE) & Digital Financial Services (DFS). DFS is actually growing at a similar if lesser pace as the E-commerce segment (Shopee) — in 6M23, DFS’s segment revenues grew by 63% YoY to $840M (E-commerce: $4.2B); while DFS’s segment Adjusted EBITDA was $236M in 6M23 (E-commerce: $357M):

DFS norm. earnings $1B: While I don’t want to jump the gun on DFS’s prospects just yet, we can surmise just from DFS’s 6M23 results as shown above that: 1) its Adjusted EBITDA is already 2/3 of E-commerce’s; 2) it can continue to grow at 1/4 the rate of E-commerce; and 3) it has much higher margins than E-commerce. Given this decent historical performance, I’d say that it’s fairly conservative to assume that DFS’s Net Profit contribution to the Group can eventually be at least 1/2 of E-commerce’s on a LT normalized basis. Based on our aforementioned estimate of $2B E-commerce normalized earnings, 1/2 of that would imply normalized DFS earnings of $1B into perpetuity.

DE norm. earnings $1B: Considering that DE’s 6M23 segment profits were already $570M despite the recent cratering in segment revenues, even a 0% growth assumption for the DE segment into perpetuity would safely imply normalized DE earnings of $1B.

Group norm. earnings $2B: If we add up all of the normalized earnings from the above three segments (Ecom+DFS+DE), we arrive at a normalized Group earnings estimate of $4B (2+1+1). Assigning a 50% margin of safety to that would result in a normalized earnings assumption of $2B.

12.5x earnings multiple: Dividing the aforementioned “Levered Enterprise Value” of $25B by the $2B in estimated normalized earnings would result in a very palatable 12.5x earnings multiple. Keep in mind that this valuation completely ignores SEA’s aforementioned liquidity position $9.5B (ST+LT); and actually adds in its $4.5B in Total Gross Debt rather than deducting its Net Cash position. Even just going by the future TAM growth of its E-commerce segment alone, I think that a 12.5x earnings multiple can be safely justified (based on a 50% margin of safety to the LT normalized earnings estimate of $4B).

50% Margin of safety x2: Considering that I was already comfortable with a 20x multiple in my previous SEA stock report in light of SEA’s TAM growth (which hasn’t changed one year later), a 12.5x multiple would imply >50% margin of safety (20/12) to that on top of the the 50% margin of safety that we have already assigned to their LT normalized earnings estimate of $4B.

Investments in Growth: For anyone curious about where SEA might intend to refocus its growth investments (free shipping is one), their 2Q23 earnings call transcript is a noteworthy read. I enjoyed this part in particular:

Wang Yanjun

So let me continue to answer the previous questions. And in terms of level of profit or loss we are willing to sustain during these periods, I think that overall, we want to remain as self-sufficient. That self-sufficiency as a core focus has not been changed. And as shared by our CEO just now, that continues to be our mantra. And also, in terms of cost efficiency improvements over time, we think that these are an important competitive moat. And in fact, the fact that we can become profitable so quickly and while maintaining the size of our ecosystem and our market -- strong market leadership and able to now also invest in growth while many of our peers still trying to manage their losses or are incurring very, very significant losses, that shows that the resilience and the strength of our ecosystem is and will continue to be a competitive -- important competitive moat for us.

As we shared previously, we truly and strongly believe that in the longer run, the competition on e-commerce, it doesn't matter which angle you cut it and where you come from. It's very much a business that focused on fundamentals. You need to serve your users well at the lowest cost possible. So these are simple rules and principles that we follow. There are many ways to engage our users. There might be new ways to engage with them that we will be able to leverage. There are many different service points we can touch and also continue to improve. And there are also many cost points that we will continue to improve upon. And these are the key competencies, I think, that brought us here to the current position of strong market leadership with the lowest cost to serve a platform that allows us to be both a market leader but also profitable and one and only in Southeast Asia so far. I think we will not give up that competitive moat, and we'll continue to strengthen that.

From period to period, we may make decisions and execute based on what we see as appropriate opportunities in the market and make investments. And those investments can be significant. But we will continue to focus on our execution efficiency. And also in the longer run, everything we're doing is continuing to strengthen our long-term profitability and market leadership. So those are the principles that we will always stick to in the long run.

Summary — Is Mr Market stupid?

In summary, I cannot understand why markets would punish SEA’s share price so severely just because they announced a return to a growth focus — when it actually accepted a 2x higher share price at the time of my earlier SEA stock report just slightly over a year ago. Their previously deteriorating businesses are fully healed from a financial perspective, and each of their business units are in much better shape in comparison.

On top of that, SEA has a fortress balance sheet to weather come what may, and their industry’s TAM growth prospects of 10% are as bright as can be realistically hoped for. Going concern risk is practically nil; and they have a dominant 30-50% market share in a commoditized e-commerce industry where competition ultimately boils down to having the greatest economies of scale.

I’m sure I’m missing a lot of negatives since this is primarily a financial statement analysis — but I’m equally sure that I’m missing a lot of positives as well. When your margin of safety is this huge, does it not justify a 12.5x earnings multiple? Even if some might disagree with how I arrived at the 12.5x multiple, is there not plenty of room for error given its projected growth rates? At the very least, we can assuredly say that asymmetric risk:reward exists.

The next thing I’d be on the lookout for is if SEA starts demonstrating large share buyback or insider buying activity — they certainly have enough cash reserves for it.

Is Mr Market stupid?

Check out some of our earlier stock reports:

I’ve also described Southeast Asia as Post-WTO China before, given the region’s current position in the manufacturing stage of its economic development lifecycle.

Keep in mind that we’re not trying to draw comparisons between SEA’s e-commerce operation and the incredible operating leverage as achieved by Amazon or Alibaba — I’ve discussed before in my previous SEA stock report how there are structural impediments which prevent them from doing so in this part of the world. However, they don’t really need to match the latter two — since all their other regional competitors (e.g. Lazada, Tokopedia, Grab) are also not immune to these structural issues.

SEA’s P&L statement reports their segment revenues rather oddly — DFS revenues are split into two parts, and subsequently allocated in an undisclosed proportion towards both the E-commerce and Sales of goods segment. However, investors can find the proper segmentation between E-commerce and DFS revenues in the earnings highlight portion of their quarterly reports.

A good chunk of their OCF in both periods was contributed by the Escrow payables and advances from customers liability item on their Balance Sheet. However, neither of the two line items changed much between the two periods, so I’m assuming their respective incremental contribution to OCF also didn’t change much between 6M22 vs. 6M23.

Great find! I need to do further research but the dislocation seems hysterical

Good stuff. Thanks, Aaron.