Paypal: GARP Discount VISA

Paypal Only Needs To Perform At Half the Performance of Apple Pay When the Former Is Valued At Less Than Half of The Latter. Also, They Can Partner Instead of Becoming Competitors.

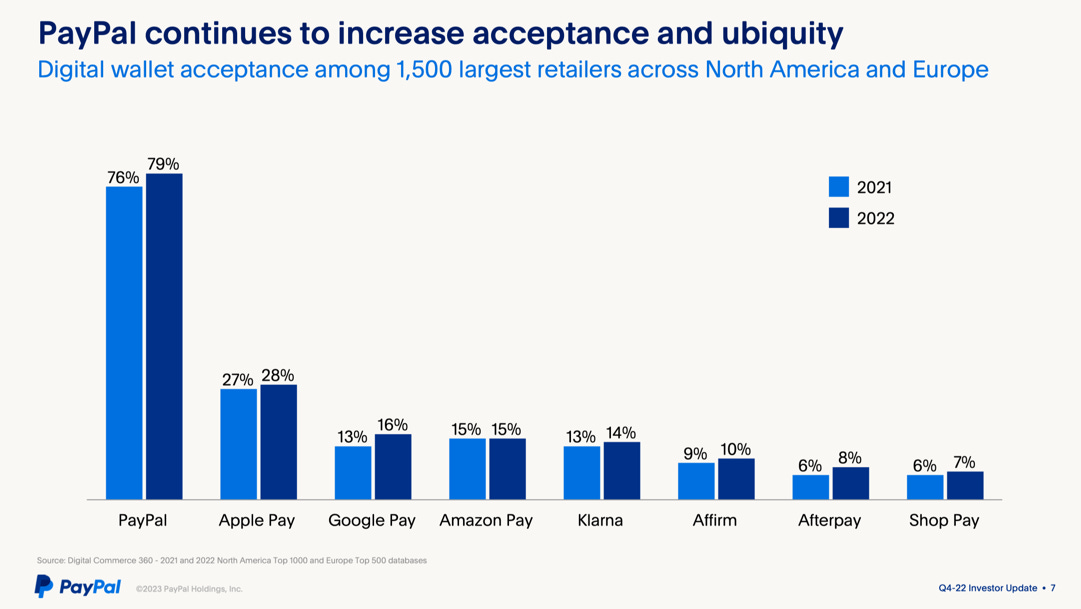

Paypal, the Discount Visa — Prevailing market sentiment about the competitive threat faced by Branded Checkout is overblown. Core PYPL has been here before nearly a decade ago, when the Goliaths were Visa/Mastercard instead of the tech megacaps — it ended up partnering with them instead of going to war, and the competitive balance was restored. Core PYPL’s moat and industry-leading 79% acceptance rate also gives its e-payments industry a similar if inferior moat (“discount Visa”) and like painfully high barriers to entry as Visa/Mastercard’s credit card industry, since both users and merchants have to be acquired piecemeal over decades.

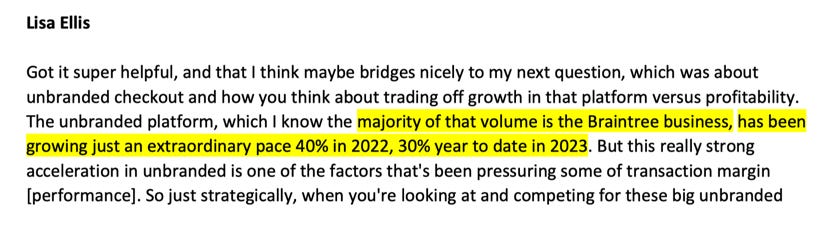

Braintree, 40% Growth in FY22 — Braintree’s industry is still growing at such a breakneck pace, it’s like 2021 never happened. It is truly unheard of for most businesses to be growing 30% during 2023 YTD alone, much less entire industries. Braintree also happens to be a Top 3 incumbent in the oligopolistic Unbranded Processing sector. Plus, why are investors so obsessed with declining transaction margins?

Venmo, the Amaz(on)ing Call Option — Venmo’s new partnership with Amazon has the potential to completely change its historical trajectory, given the “chicken-and-egg” phenomenon of network effects experienced by all platform businesses. I am unsure why markets are still sleeping on Venmo’s potential, because the upside optionality here is truly vast (“call option”).

PYPL Valuation — Given the potential implied growth rates, I simply cannot fathom why PYPL 0.00%↑ is still on sale at just 17x trailing PE. In fact, this scenario invokes nostalgia of when I wrote about META 0.00%↑ after it fell to $90 in Nov 2022 on similarly unfounded doomsday fears — the latter's share price has since climbed by >300% in less than a year, mostly owing to multiple expansion on positively revised market sentiment. The same could hold true for PYPL.

Chapters:

Paypal & The 3 Dwarves

Branded Checkout (“core” Paypal) — The Discount Visa

Unbranded Processing (Braintree) — 40% growth in FY22, 30% in 2023 YTD

Venmo — The Amaz(on)ing Call Option

Paypal’s Valuation

4C’s & a B: Costs, Crypto, CEO, Capital Allocation & BNPL

For the longest time, Amazon didn’t allow customers to use Paypal as a checkout option, despite Visa/Mastercard being allowed since the Amazon’s inception. The reason was simple: Paypal was by then already the dominant digital wallet — and Amazon wasn’t keen on funneling e-commerce transactions towards it and potentially enable it to strong-arm Amazon in the future (the way Visa/Mastercard could). Furthermore, Amazon’s then-fledgling Amazon Pay was also a direct digital wallet competitor to Paypal.

Perhaps those fears were founded after all — over a decade later, Paypal still has a ~79% acceptance rate (rough proxy to market share) in the US digital wallet industry today, and has a 4-5x lead over its nearest competitor (Apple Pay) while leaving everyone else in the dust. If Paypal had been allowed as a checkout option on Amazon since the latter’s inception, there is little doubt that it would have developed sufficient bargaining power by now to demand preferential rates from Amazon — the same way Visa/Mastercard tend to demand it from their merchants.

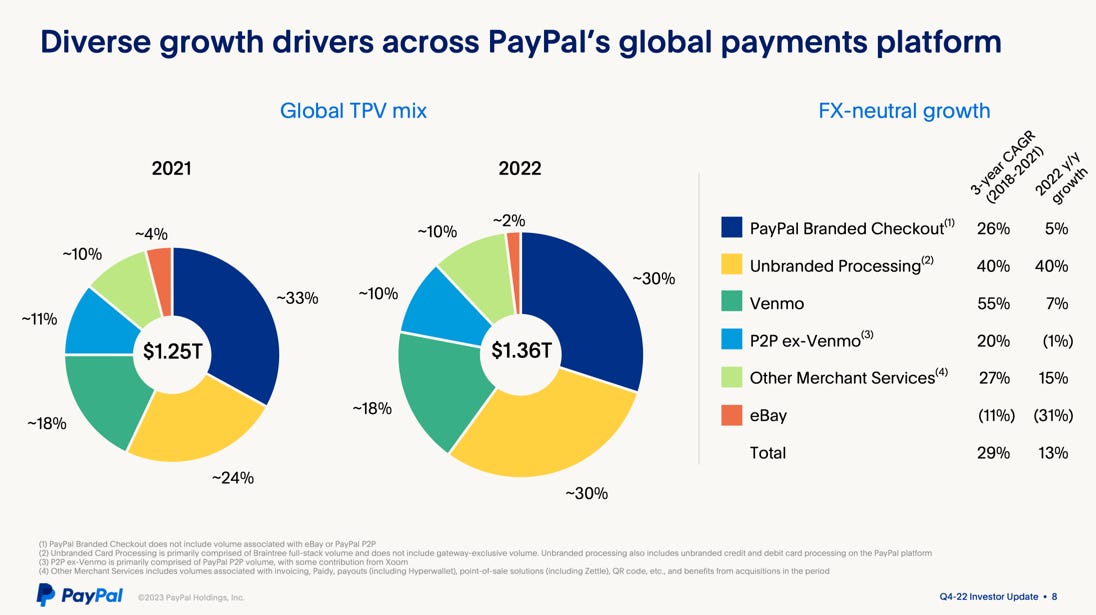

However, Paypal’s subsidiary Venmo was recently introduced on Amazon as a checkout option under the heading ‘Pay with Venmo’ — perhaps due to Amazon also having developed its own bargaining power by now. While investors have known for awhile that Venmo was historically unprofitable due to its predominantly student user base, what is perhaps less known is how their merchant program ‘Pay with Venmo’ actually charges roughly half the fees of core Paypal. And as we can see in the chart below, it still represents a huge chunk of Paypal’s transaction volume at ~18% of Total Payment Volume (TPV):

We’ll dive into Venmo a little deeper below, but for now a quick business primer on Paypal is in order. As mentioned above, Paypal has by far the largest acceptance rate in the US digital wallet space at 79% in 2022, which leaves all its competitors in the dust. However, it’s worth mentioning this industry-dominant position is only represented by core Paypal’s Branded checkout segment — which as we can see in the chart above only represents ~30% of their Group TPV.

The chart above also shows how another ~30% of Group TPV is represented by the lower-margin Unbranded Processing segment (Braintree) but which has extraordinarily high growth (40% in FY22, 30% YTD in FY23).

Meanwhile, their 3rd significant segment Venmo represents 18% TPV but is still not profitable-at-scale yet — while the other remaining segments contribute insignificantly to the Group’s bottom-line. This means that only the top 3 segments represented by Branded Checkout, Unbranded Processing and Venmo (total: 78% of FY22 TPV) are relevant to the valuation of the entire Paypal Group.

It may surprise investors to realize that Paypal is actually an absolute payments conglomerate with a ton of moving parts, which its ~$65B market cap might belie. This was probably contributed by the roughly 7 major acquisitions it has made over the past decade, which included Braintree in 2013 and Venmo in 2012. There is a surprising level of scale and complexity within the Paypal Group — something which caught me off guard at first — and this reports aims to untangle this complicated web to provide investors with an eagle-eyed view towards its future valuation.

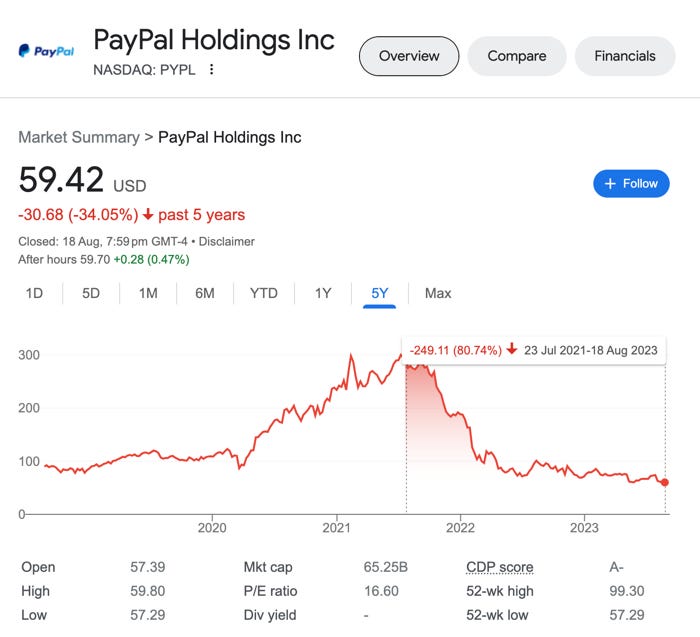

This may be all the more worth doing given how PYPL 0.00%↑ share price has collapsed by -20% YTD — and an astounding -80% since it hit its peak in July 2021:

Investors will also no doubt want to learn about what Paypal’s newly hired CEO Alex Chriss brings to the table (hint: likely the high-growth Unbranded Processing); as well as why Paypal is making its foray into the stablecoin industry at a tumultous time for crypto regulation.

What are the common threads between the different trajectories taken by all of Paypal’s respective business segments, and how do they all tie into the purported endgame of the wider Paypal Group? Keeping in mind its current position as by far the dominant player in the US digital wallet space. We’ll explore all this and more in this Paypal stock report — and why I refer to it as the GARP Discount VISA.

Paypal & The 3 Dwarves

As mentioned above, only 3 of Paypal’s businesses really matter to shareholder returns — Branded Checkout, Unbranded Processing and Venmo. The reason why I segment it this way is because Paypal is actually a huge digital payments conglomerate, largely due to its wasteful acquisition spree under departing longtime CEO Dan Schulman. Other sellside analysts cover these underperforming acquisitions in detail if you’d like to learn more about them, e.g. Honey, Paidy, Zettle — they do have their place, but in my view the top 3 are really all that matter.

By stripping out all of these other smaller businesses and focusing only on Paypal’s top 3 businesses, we gain a clearer view of the latent potential lying dormant within these 3 business segments — especially in the context of Paypal’s currently lazy share price. They are:

1) Paypal Branded Checkout (“core”) — The original Paypal digital wallet business. The main distinction between core Paypal and its Unbranded Processing segment below lies in the Paypal brand, i.e. the extremely recognizable yellow checkout button splashed with the Paypal logo. This is a great way to differentiate between the two, since the back-end processing of the payments infrastructure is actually relatively similar between them. However, this additional branded element allows Paypal to charge merchants much higher fees for the privilege of allowing their customers to “Pay with Paypal”. Core Paypal’s main digital wallet competitors: Apple Pay, Google Pay, Amazon Pay, Shopify Payments, Visa Checkout, Masterpass.

2) Braintree (“Unbranded Processing”) — Braintree was acquired in 2013, and is basically just the back-end payments infrastructure of Paypal without the branded yellow checkout button. Enterprise customers may sometimes not want to associate their checkout experience with a 3rd party like Paypal, but still want to offer their customers a similarly frictionless checkout experience. If they don’t want to host their own payments infrastructure, they will typically outsource the checkout function to a PSP (Payments Service Provider) like Braintree. While a lower-margin business than Branded checkout, Braintree has been growing like bazookas (FY22: 40% growth) and is probably where the incoming CEO Alex Chriss plans to spend most of his attention on given his relevant background in the space. Braintree’s main competitors: Adyen, Stripe.

3) Venmo — Venmo was acquired in 2012 and is basically a direct competitor to Paypal in terms of being a digital wallet — except for being owned by Paypal. Venmo is mainly used by 18-25 year olds and is the dominant digital wallet among the US college crowd with >75m MAUs. However, this demographic is also surprisingly difficult to monetize since: 1) there’s a lot of friction in adding charges to Venmo transactions amongst the mainly student user crowd, and 2) students don’t tend to require or be willing to pay for value-added services like instant bank transfers (1% fee). That is why Venmo still offers free user-to-user transfers (unlike Paypal) and barely represents 5% of Paypal’s transaction revenue mix to this day, despite representing over half of the latter’s TPV as we saw above. However, the economics of the merchant-oriented ‘Pay with Venmo’ checkout option on Amazon is strikingly different from the free user-to-user transfers — as it charges roughly half the fees to merchants which core Paypal’s Branded Checkout does (rather than to customers). We’ll discuss below why I think Venmo’s upside optionality is overflowing due to this phenomenon. Venmo’s main competitor: Cash App.

In the upcoming sections, we’ll talk about the potential of each of Paypal’s three business segments. Unfortunately, Paypal doesn’t disclose the individual performance of the respective three segments in their audited financial statements, so there’s going to be a little bit of guesswork involved — management does provide some granular data such as TPV & transaction revenues in their investor presentation decks, but obviously these are selected data and were likely chosen to put the businesses in their best light. Some sellside analysts have gone out of their way to make contorted assumptions about segment revenue and mix — by extrapolating from Group metrics and assigning industry comps — but honestly, I find that they are imputing so many assumptions so as to render their analysis & forecasts guesswork at best.

Instead, what I plan to do here is to stick to much more reliable data taken straight from their audited financial statements, and focus instead on demonstrating that a sufficiently large margin of safety exists in Paypal’s valuation — value investing style. Not only will this rely significantly less on my own financial modeling assumptions, there is also less pressure to get all my (pinpoint accurate assumptions) ducks in a row, only to miss the forests for the trees. Some of the sellside analyst target prices compound on so many valuation assumptions that you start to wonder what happens if just a few of those assumptions turn out to be grossly inaccurate — the way many of them have turned out over the past two years. (e.g. using comp historical growth rates to forecast future revenue growth)

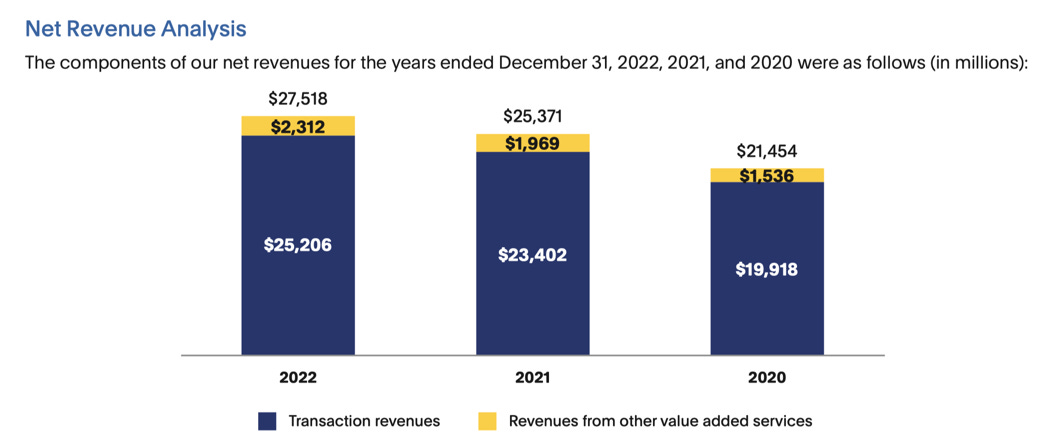

The other benefit to taking the margin of safety approach to valuation is that we don’t actually need to be pinpoint accurate about our estimates of future business segment performance. For instance, some of the sellside analyst reports go into so much detail regarding Paypal’s revenues from other value added services (OVAS) — given the legitimate complexity involved — when ultimately they only represent <10% of net revenues (see chart below), and even less than that in contribution margin.

To be fair, Paypal actually is an exceedingly complex global business and they’re just doing their job — but in this report, I’ll spare you the torture that I went through of reading through paragraphs after paragraphs of text, only to realize at the end that those parts were relatively irrelevant to the valuation exercise. Instead, I’ll be mostly focusing only on the actual needle movers, and just cursorily touch on the mindboggling amount of miscellaneous stuff under the Paypal conglomerate that is ultimately unnecessary to arrive at Paypal’s valuation (e.g. Honey, Paidy). If you’d still like to read about them, you can find plenty of detail on the respective businesses and acquisitions on sites like Bloomberg, VIC or Seeking Alpha.

Assuming a significant enough margin of safety exists in Paypal’s Group valuation, it should more than absorb any impact that all these little raindrop businesses might have on the final valuation — while cutting the length of this report by at least half, and saving you a ton of time determining whether their shares are undervalued or not.

Branded Checkout (“core” Paypal) — The Discount Visa

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.