✨ Much Ado About Netflix - House of Cards, or Queen's Gambit at 17x PE?

A Business Economics Primer of Netflix and its Streaming Industry - and How Investors Have Short Memories

Click here to read my previous Part 1 article titled: “Big Tech is officially in Value (factor) Investing Territory”!

NFLX’s share price has since fallen by -68% YTD, resulting in their current valuation of 17x trailing PE. This was likely due to three recent changes from the status quo: 1) negative 1Q22 subscriber growth, 2) password sharing crackdown, and 3) their pivot towards an ad-supported business model.

NFLX’s reporting of their Amortization of content assets reflects a true & fair view of their consumption patterns; and their outsized Commitments & Contingencies are all above board. No hanky panky going on here.

We’ve actually seen this story before - investors seem to have forgotten that NFLX actually experienced similar concerns during 2015, 2018 and 2019 - when their share price experienced drawdowns of -30%, -40% and -30% respectively.

We explore the business economics of NFLX and its Streaming sector - their entry into an ad-supported model makes a lot of sense and should be viewed as a net positive, in my view.

If NFLX can eventually rise up to become a media giant the likes of its predecessor Cable competitors, it can easily justify an investment today at 17x trailing PE. Keep in mind that Bill Ackman’s initial stake was acquired at around 40x PE - so new investors in NFLX today won’t have the same exposure as him.

In my previous article titled, “Big Tech Is Officially in Value (factor) Investing Territory”, I discussed how I felt that the ‘FING’ stocks (Facebook, Intel, Netflix, Google) might have fallen into value factor territory (not value investing) - after even some of the Big Tech megacaps saw their share prices crashing by -70% YTD. The tweet below demonstrates how bad the carnage was over just the past half-year alone - with some drawing parallels to 1929 Depression-era crashes:

One of these unfortunate casualties was Netflix (NFLX) - which has fallen by an astounding -68% YTD. At its peak, NFLX was trading at nearly $700 or 60x trailing PE - but since then, it fallen to its latest share price of around $188 or 17x trailing PE. Regardless of whether this makes it a value factor stock today, it certainly caught my attention as a value investor - especially considering that Netflix is currently the world’s dominant streaming platform. My initial screening criteria was that if the market leaders of other highly capital-intensive and commoditized industries can command 30x average PEs despite posting flat growth (e.g. FMCG, O&G, Financials), it shouldn’t be surprising to imagine NFLX one day commanding those valuations either.

Chapters:

Addressing the dominant bearish narratives surrounding NFLX stock today:

Understanding NFLX and its Business:

We also have a sister news blog for daily market news, Value Investing Substack NEWS. Click the box above to check it out!

Why NFLX Fell -68% YTD

If you’ve been following market news recently, it would probably be no “Stranger Things” to you why Netflix’s share price cratered by -68% YTD. On the macro front, surging inflation (due largely to supply-side issues) led the US Fed to announce a 50 bps interest rate hike yesterday - this projection was telegraphed months ago and hit all Big Tech stocks hard, as the purchasing power of their long-tail returns got crushed by rapid inflation.

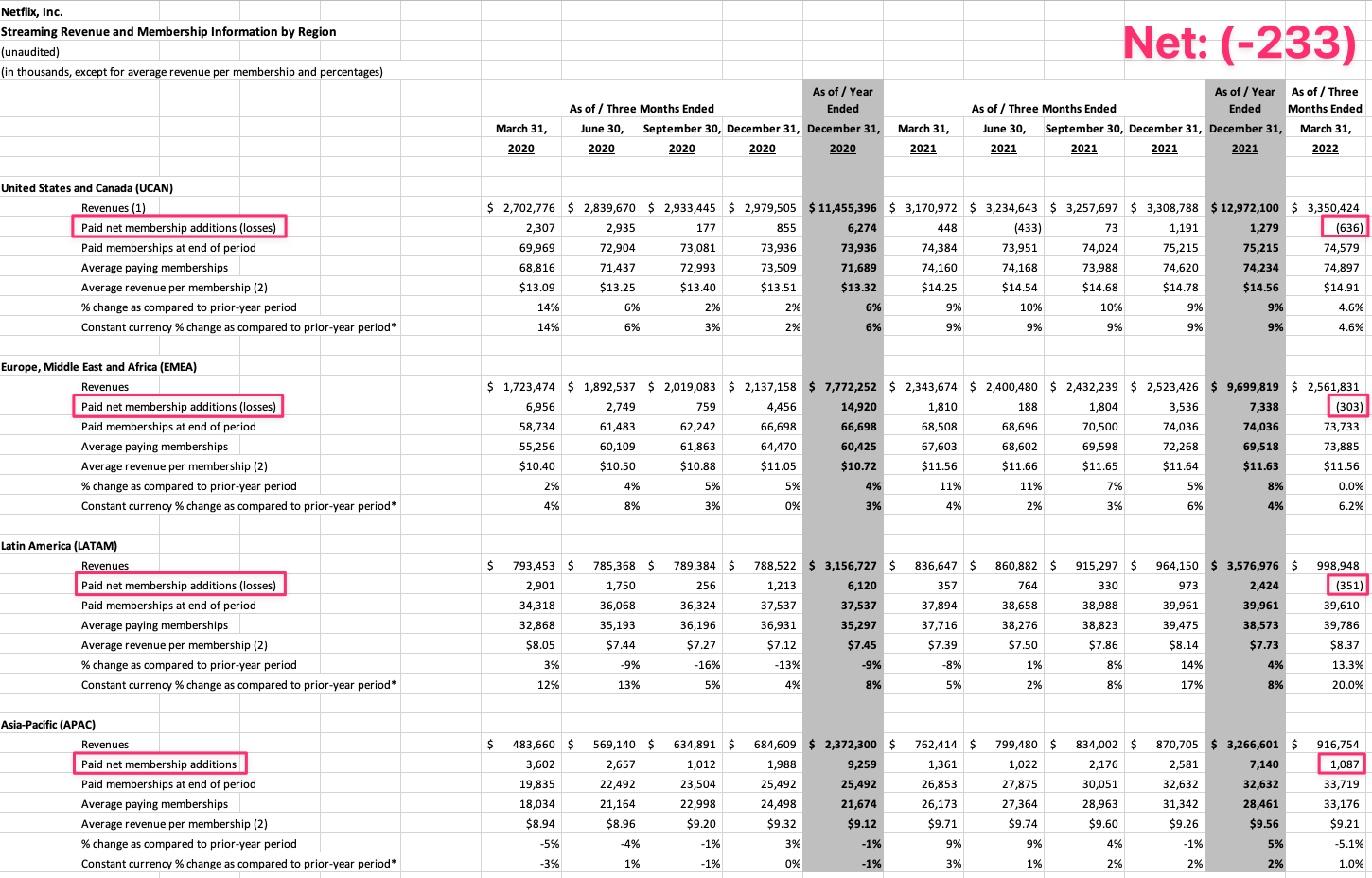

However, NFLX shares part of the blame as well for its calamitous fall from grace. At the idiosyncractic level, management recently announced three changes from the status quo - 1) for the first time in a decade, the company reported negative overall subscriber YoY growth (see below), perhaps resulting from: 2) their decision to start disallowing password sharing amongst subscribers. They also said that 3) they would be entertaining a shift towards a hybrid subscriber-ad business model, which would mark a significant departure from their previous subscriber-only model.

Immediately following the news, famed investor Bill Ackman announced that he would be disposing his entire stake in NFLX - despite announcing his initial position just slightly less than three months ago. The combination of all the above served as a one-two punch in NFLX’s proverbial gut - prompting its share price to fall by -35% overnight after its latest quarterly earnings announcement in mid-April.

While I wasn’t a fan of NFLX’s rich valuation over the past two years, its latest share price reflects a valuation of roughly 17x trailing PE - which caught my attention, especially considering that it is currently the dominant global streaming platform in a New Media era where Streaming has emerged as the incumbent. I’ll share more about NFLX’s future amidst the broader context of its Streaming sector below - but to save us all some time, let’s get some of the easier questions about them out of the way right now.

Firstly, while it is true that their subscriber growth hit a speed bump last quarter, it is also plausible that this was partially contributed by their announcement they they would no longer be tolerating password sharing between users of different households. Anecdotally, I personally know plenty of friends who engage in such privacy shenanigans - and it is not difficult to imagine how this might have pushed some “lurker” subscribers who might have only had enough time to watch 1-2 episodes per month due to work over the edge (I used to be one of them) - and justify cancelling their subscriptions. It might be worth noting that such types of cancellations tend to represent large one-time drops in subscriber growth - which implies that extrapolating these cancellation rates into perpetuity might not necessarily be the correct thing to do. As Munger puts it, “invert always invert” - imagine what might happen if next quarter’s subscriber growth recovers to positive territory.

Now of course, that still doesn’t satisfactorily explain why Ackman might have sold his stake - since he is clearly far smarter than I am and would have foresaw this possibility as well. My current working theory is that his inital stake was acquired at the beginning of this year at closer to 40x trailing PE - so even if he were to average down at today’s valuation of 17x PE, his average cost basis would still be around 30x PE. And I would be inclined to agree that NFLX would be a much harder buy (pun intended) at 30x PE - probably easier to cull the position than to suffer through an endless stream of angry investor calls, financial paparazzi, and Robinhood judges (especially when an actual global monopoly is currently also on sale for 21x PE).

However, for those of you who still have yet to initiate a position in NFLX, your upside exposure wouldn’t be the same as Ackman’s - you’d be getting in at a clean 17x trailing PE - which at least on the surface, sounds like a genuinely seductive proposition.

Content Assets & Amortization

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.