Hibbett, The Oddball Stock: A Genuinely Mispriced Small-Cap Flying Under The Radar (Part 2)

Hibbett, The Oddball Stock: A Genuinely Mispriced Small-Cap Flying Under The Radar (Part 2)

Nike with Operating Leverage + Apple's share buyback-induced EPS Growth

Report Highlights:

Hibbett’s financial model is basically Nike’s revenue growth supercharged with Apple’s share buyback-induced EPS growth.

Management demonstrates strong evidence of optimal capital allocation — as evidenced by an outsized focus on generating growth via improving unit performance rather than volume growth.

Astounding earnings yield “curve” which demonstrates at least 25% undervaluation. Adequately fulfills Buffett’s Rule No. 1: Never Lose Money. Same low risk as Nike.

Extreme deep-dive financial analysis of Hibbett, with objective data-driven analysis behind every claim made. Narratives can be made up, but Numbers never lie.

A genuinely mispriced and undervalued small-cap which has somehow gone unnoticed by supposedly efficient markets. An Oddball Stock.

Table of Contents:

1. Hibbett’s 3Q24 Earnings Call Review

2. AI-Generated Summary of this Report (550 words)

3. Inventories & Payables Performance Relative to Sales

4. Strong Evidence of Optimal Capital Allocation. Also, Comps.

5. Risk: Can Nike Pull The Rug? (Unlikely)

6. Valuation: Apple's Share Buyback-induced EPS Growth

7. Download Hibbett's 3-Statement Model (Excel)At the end of the day, a LT shareholder’s investment consideration boils down to their investment yield (similar to fixed income). This is basically what the PE ratio (or Earnings Yield) represents to business owners — the business’s normalized No. of years to breakeven. In a business context this would normally be represented by ROE — but since investors acquire shares at a premium in public secondary markets, the more accurate ROE equivalent would be Earnings Yield.

As suggested by Benjamin Graham’s preponderance with “safety of principal” in his quote below, the general starting point of value investing in equities should be the risk:reward of fixed income. Risk shouldn’t be avoided as noted by Graham below, but incremental risk should only be accepted where commensurate incremental reward can be justified. This is the essence of what it means to be an Intelligent Investor:

Hibbett makes for a very interesting case study in this vein. Firstly, the reason why I described it as “A Mathematical Nike” in Part 1 is because its business model results in a very predictable earnings yield. Management may not have much control over sales volumes by virtue of their reliance on Nike — but they have done a wonderful job controlling the things within their control and optimizing for operational efficiency.

Furthermore, Hibbett’s highly stable and predictable cash flows results in a long-term financial profile that can be reliably extrapolated quite far out into the future, small business notwithstanding. This makes it easy to estimate its normalized LT earnings yield with lower uncertainty, resulting in a somewhat fixed income yield profile with pretty robust growth over time via management’s financial engineering — even if operational growth is relatively limited.

The fact that most of Hibbett’s EPS growth is cultivated from financial engineering rather than organic business growth is actually a feature, not a bug. Firstly, its revenue growth pretty much mimics that of Nike’s, since around 70% of its Net Sales come from selling Nike sneakers to a very niche customer demographic. This provides Hibbett’s top-line with the same kind of relative predictability as a large global brand like Nike. Subsequently, management assigns operating and financial leverage onto that revenue growth to generate EPS growth, via tightening operational and financial efficiencies (Optimal Capital Allocation). This enlightened combination results in an almost doubling of their 10Y historical revenue CAGR of 7.6% into a whopping 10Y historical EPS CAGR of 13.5% (as we saw in Part 1).

And since both Nike’s revenue growth and management’s tightening of efficiencies can be expected to persist for the long-term, it creates a stream of normalized future cash flows which is easy to forecast. At 8x PE today, there is a sufficient case to be made for a reversion to the mean (13x historical average PE) in Hibbett’s valuations in FY24 — especially in light of a recovering wider US retail environment.

Back in the days before Substack existed, there was a popular value investing newsletter called Oddball Stocks which focused almost exclusively on finding mispriced small-cap opportunities. I would humbly submit that Hibbett’s valuation amply qualifies a spot on his newsletter. The potential earnings yields, low operational uncertainty/risk, and “yield curve” over time under different earnings yield assumptions are simply flabbergasting — as we shall see in the Valuation section of this report below.

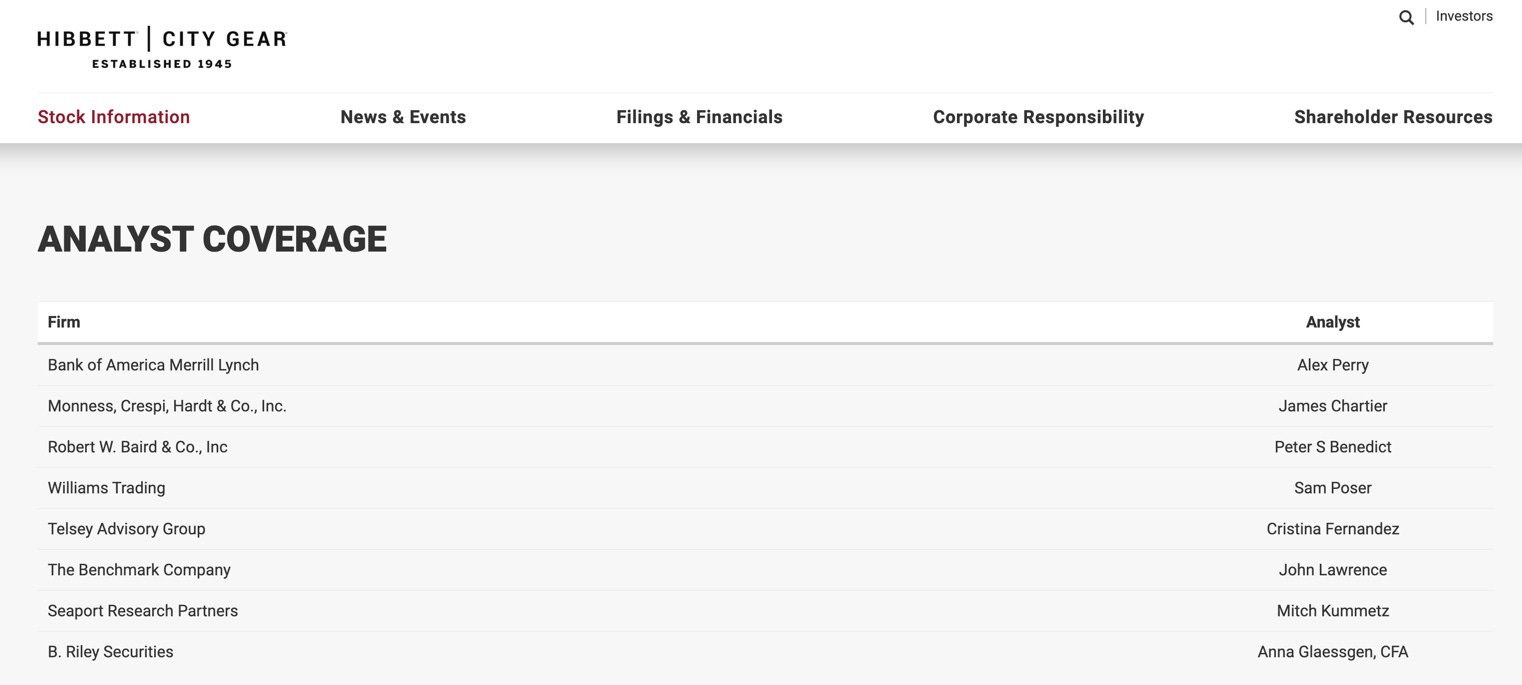

Considering that a stock’s earnings yield is a function of both profit and share price, it’s easy to see why this is the case — Hibbett may not be a wonderful business with large moats, but its share price is simply gobsmackingly undervalued. Nor is it a cigar butt either — it has long growth tailwinds by virtue of its symbiotic relationship with Nike. It’s just one of those underappreciated small-caps that have flown under the radar and are genuinely mispriced. This is actually not too hard to imagine when you review their analyst coverage on their Investor Relations page — only 2-3 of the investment houses listed are recognizable by most people:

Check out our previous stock reports:

Hibbett’s 3Q24 Earnings Call Review

As mentioned in Part 1, Hibbett provides a highly granular review of their earnings performance in their earnings calls. This is relevant for the “Mathematical Nike” reasons we’ve discussed in Part 1.

And given their relatively simple retail business model, just giving their latest 3Q24 earnings call a quick read actually does wonders in providing a decent 360° view of Hibbett’s performance through the last year. Let’s go through it below:

3Q24 Results Highlights :

3Q24 results benefitted from a strong back-to-school season.

Store expansion strategy to add 40 net new stores this year is still in place.

Footwear saw a low-single digit comp increase, driven by a favorable launch calendar and strength in basketball, lifestyle and running silhouette categories.

Apparel and Team Sports were down in the low-teens for 3Q24, influenced by warm and dry weather patterns. Apparel continued to be affected by promotional activity due to elevated inventory levels in the market (oversupply). Men’s category was down low single-digits, while women’s were up low single-digits — with women’s footwear up in the mid-teens, while apparel was weak.

Inventory levels declined slightly both sequentially and YoY. Management expects promotional activity to continue in 4Q.

Comps decreased -2.7% YoY and increased 1% YTD. Brick-and-mortar comps declined -5.4% YoY and declined -2.7% YTD. E-commerce comps increased 12.6% YoY and increased 2.9% YTD.

3Q’s GM decline of 40 bps was driven by lower average product margin, due to higher promotional activity in both Footwear and Apparel. Higher store occupancy costs as % of sales were offset by improvements in freight, shipping, shrink and logistics costs as % of sales.

SG&A as % of sales fell 90 bps YoY due to improvements in store labor efficiency, and strategic reductions in discretionary expense categories (e.g. professional fees, advertising). These savings more than offset cost increases from inflation on wages, goods & services, and the slightly lower sales volume YoY.

Depreciation & Amortization increased $1.4M YoY due to increased capital investment on store development, technology initiatives, and various infrastructure projects over the past 3 years.

Net inventory fell -1.7% YoY and -5.4% YTD. 75% of 3Q24’s CAPEX were allocated towards store development projects, including new stores, remodels, relocations and new signage. 10 net new stores were opened in 3Q, bringing the store base to 1,158 in 36 states.

700,000 shares were repurchased in 3Q24 at a total cost of $32M. A dividend of $0.25 per share was also paid at a total cost of $3.1M.

Loyalty sales grew single-digits in 3Q24 driven by average ticket growth and increased members shopping. Average ticket growth was in turn driven by higher average until retail, while the increase in members shopping was driven by continued engagement by existing members.

Hibbett announced the launched of Connected partnership, which connects Hibbett’s previously standalone loyalty program directly to Nike’s loyalty program. This will further distinguish the Hibbett retail experience, such as by introducing exclusive shopping experiences, personalized content, and early access to Nike and Jordan member products. It will also improve engagement with members across all omnichannel touch points. The launch of the Connected partnership was heavily marketed, and customers have been very receptive so far.

E-commerce sales increased 12.6% YoY, and represented 17% of Net sales as compared to 15% last year. Traffic, conversion and average ticket all increased in 3Q24, driven by footwear and strong back-to-school sales.

4Q Guidance and Earnings Drivers

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.