Zoetis down -50% over the past year

World's leading animal pharma company at 13x PE with 9% EPS growth

Occasionally something crosses my eye which screens well, but after some work is done it isn’t interesting enough to warrant writing about it as a paid article. Zoetis is one such stock. There’s hints of genuine value in the position but I figured there wouldn’t be enough people interested in their single-digit growth. I already finished the analysis halfway, so I thought I’d share it with those who are interested in it.

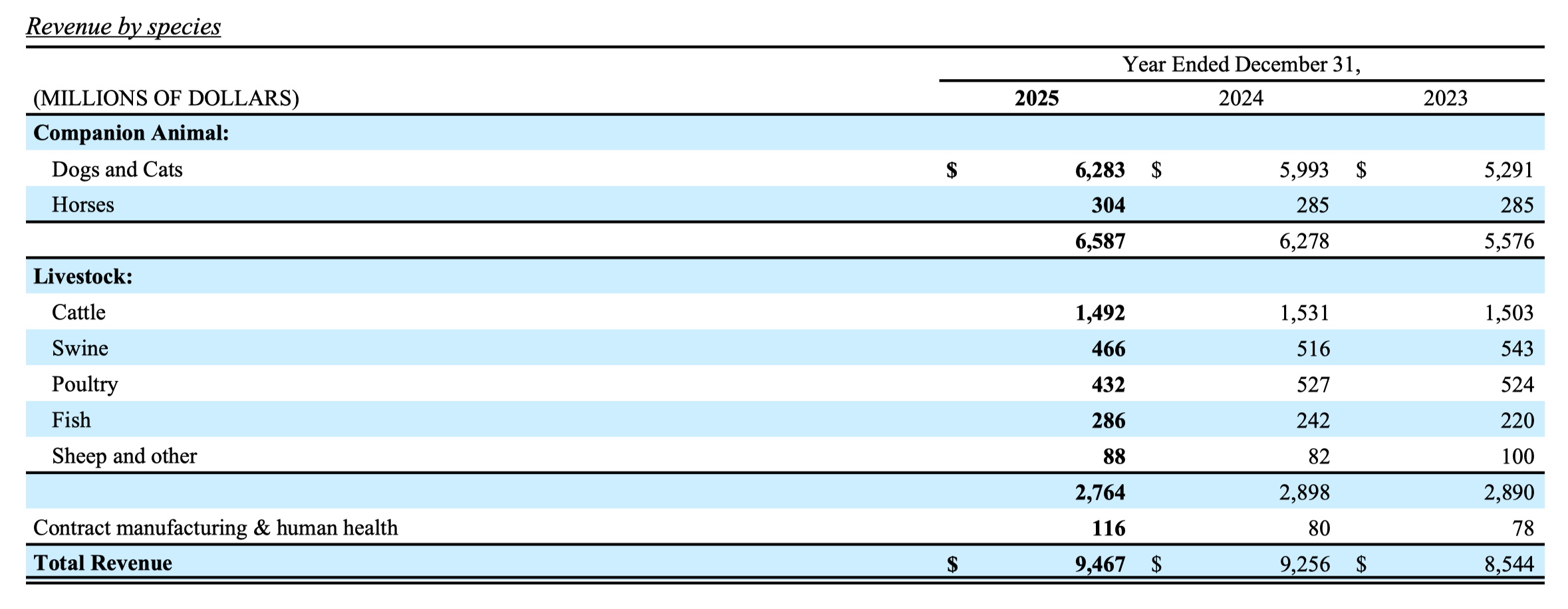

The company was spun-off from Pfizer in 2013 as the “animal pharma” division, and basically makes medicines for pets and livestock. The pet division, which they call the “Companion Animal” segment, does about $6.5B in revenues, with most of it coming from Dogs and Cats. The livestock segment drew in about $2.7B in revenues in FY25, with about half of it coming from Cattle. Think of allergies or diabetes in pets, serious illnesses which warrant pharmaceutical treatment and an expense that households are willing to spend on a “family member”. That’s what Zoetis addresses in a nutshell together with its army of veterinarian clinics across the world.

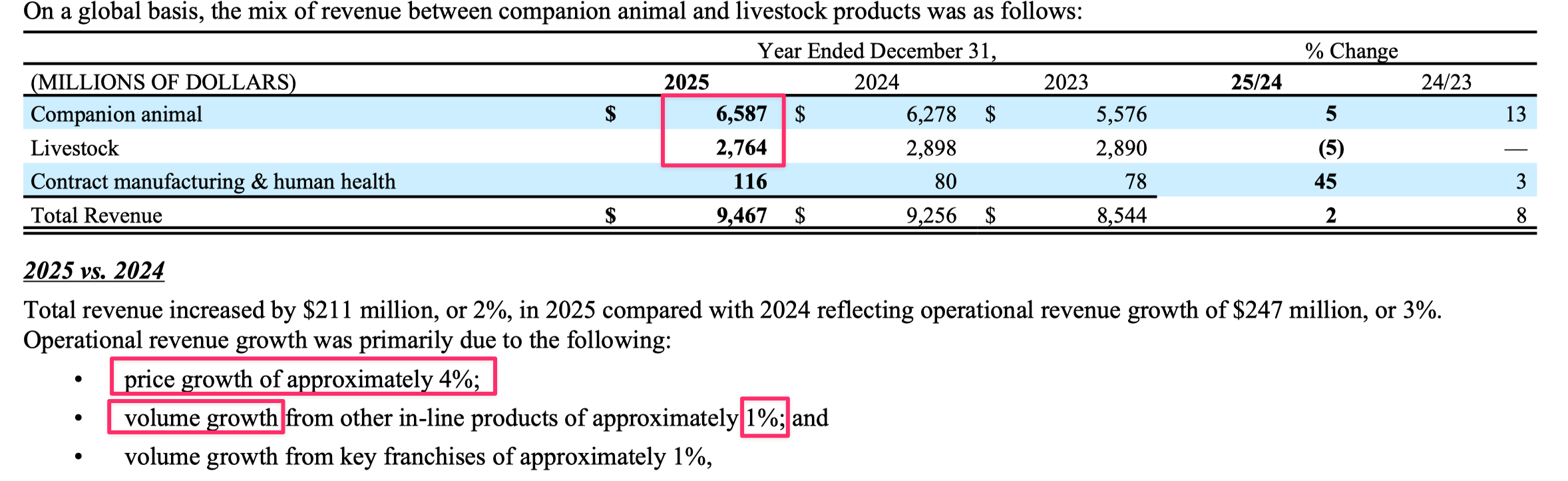

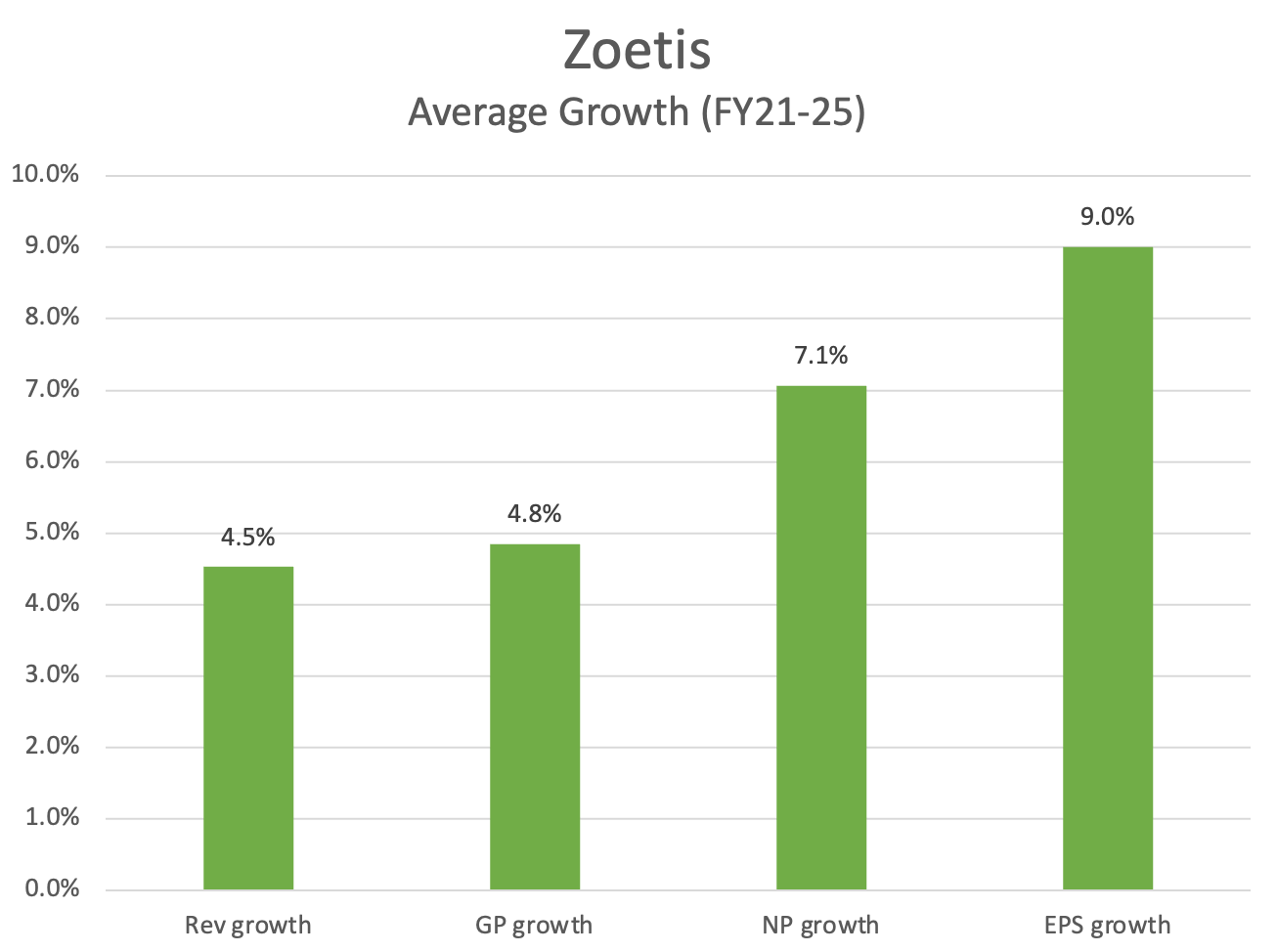

Being the Pfizer of animal health, Zoetis is able to command pricing power from its fragmented global network of vet clinics and raise prices by about 4% per year. Add another 1% in volume growth, and you get about 5% in annual revenue growth per annum. For some reason, this mix only resulted in 2.5% revenue growth in FY25; but as we’ll see below, their 5Y average revenue growth was indeed about 4.5% since FY21.

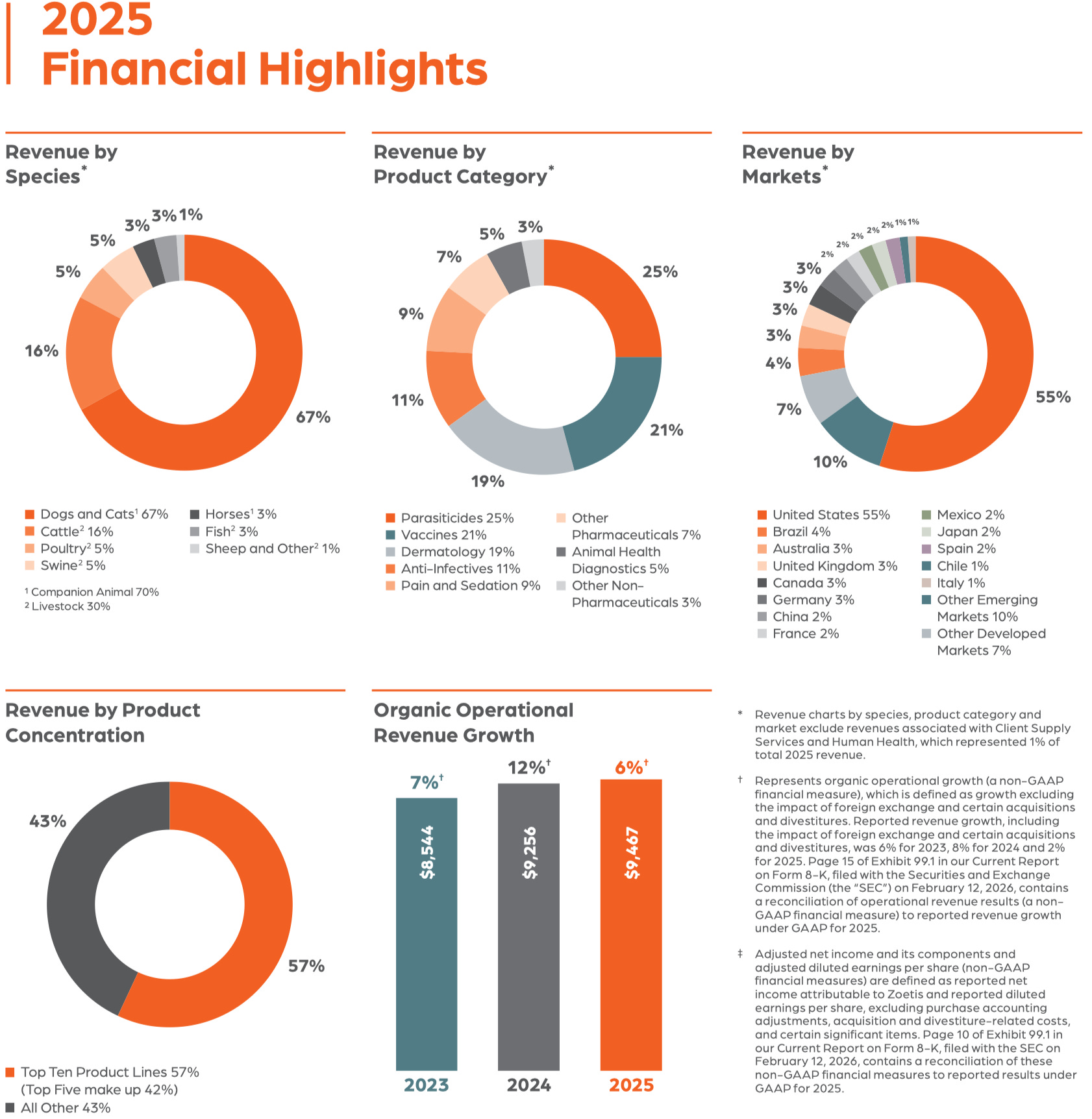

Revenue is split roughly 60:40 between US and International. Notably, nearly 80% of US revenues came from the Dogs and Cats category alone in FY25, so this is very much a Pet business as opposed to a livestock one.

About 40% of revenues was represented by just the top 5 product lines, and about 60% of revenues were represented by the top 10 product lines. The largest customer represented about 15% of revenues in FY23-25; but they didn’t reveal anything about the 2nd and 3rd largest customers, so it’s plausible they could each also represent ~10% of revenues. This makes Zoetis a rather top-heavy business, which has its pros and cons.

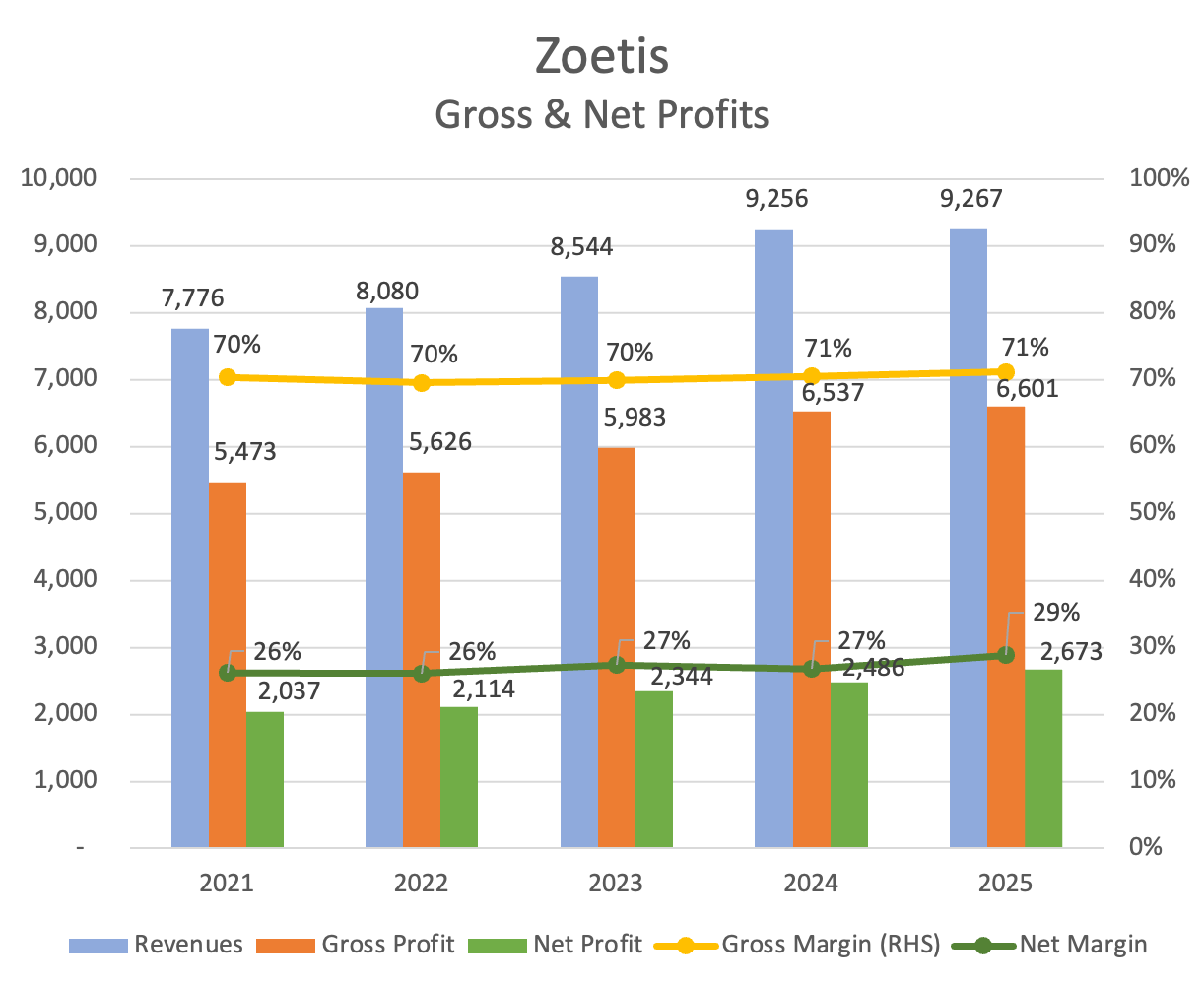

Gross Margins (yellow line) have remained rather stable, so the evidence of pricing power is not showing up in the numbers; I’m just going to take their word for it that pricing growth has been 4% per annum. Net Margins (green line) have actually shown some improvement over time.

Gross Profits have grown in line with revenue growth, while Net Profit has grown at a 50% faster rate than revenues. EPS has grown even faster, at about 9% per annum, showing the presence of share buybacks.

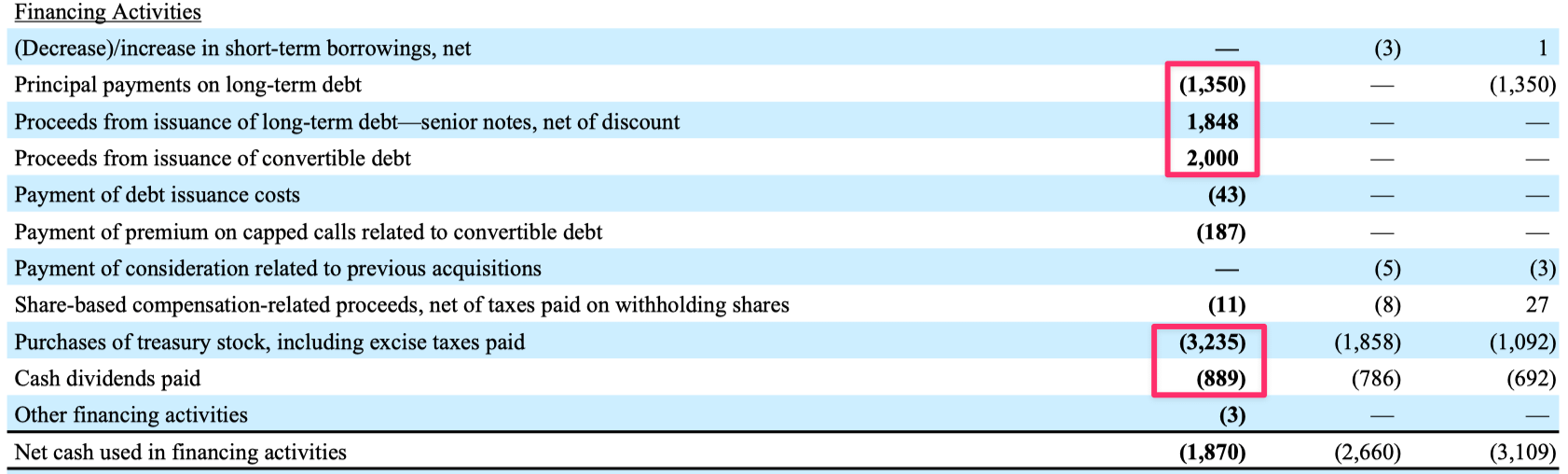

One thing that stood out in the Balance Sheet though was that they funded share repurchases using debt, increasing Total Debt by nearly 50% to about $9B in FY25 (market cap: $34B). The Cash Flow Statement showed that they took on incremental Convertible Debt (strike price: $148.20) to fund their share buybacks, with total shareholder return (including dividends) exceeding FCF in FY25. Considering that the share price has collapsed recently, investors might be able to look forward to more debt being taken to fund share buybacks in FY26.

The main reason for the recent collapse in the share price was because they reported that the US Companion Animal segment saw a 11% YoY decline in segment revenues. As that’s where they’re supposed to be focusing on most — given the higher margins and higher defensibility/moat of profits of the Pet segment — it’s no surprise that it resulted in a 30% drop in the share price after Q1 earnings.

However considering what we’ve seen in the historical revenue trend, this doesn’t seem to be an insurmountable hurdle. On one hand it’s not a business that’s going to grow much; on the other hand, it’s also not likely to collapse catastrophically. Double-edged sword.

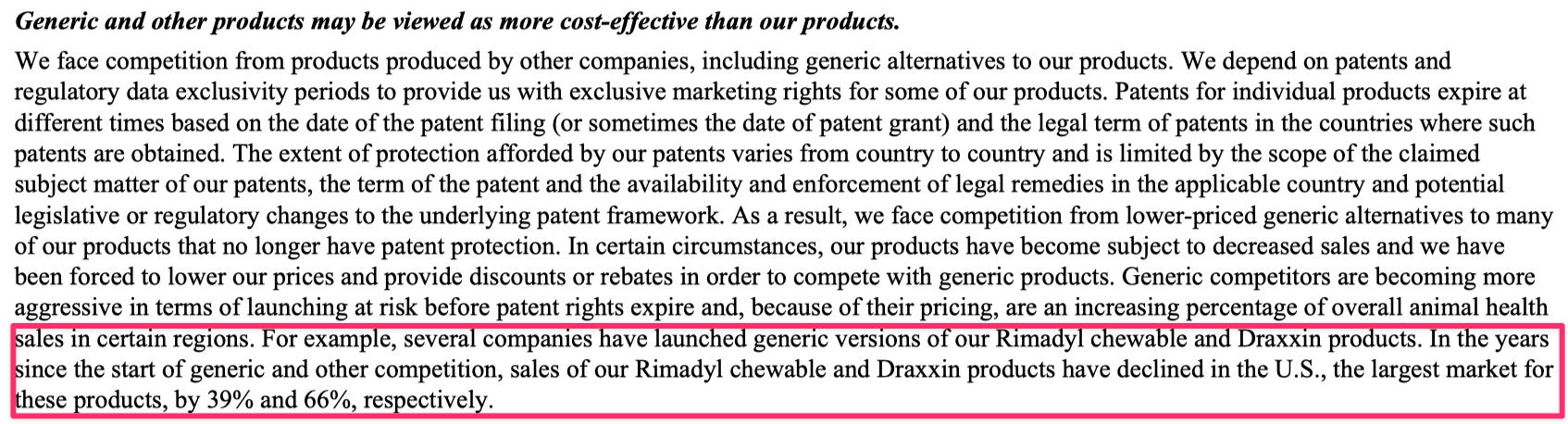

The company cites generics as a potential risk in its financial statements. I’m not sure how much of this could be attributable to the 11% YoY decline in Pet segment revenues, but this is just something to watch out for if you’re interested in investing in the business.

This article is not meant to replace an exhaustive review of the company, but at first glance the 13x PE does seem to be a fair price for 9-10% EPS growth. And there does appear to be a defensible business behind it.