Tap Dancing To Work: What Passion in Markets Really Means

So You Want To Be A Fund Manager? Why deep focus is crucial for alpha generation

“First of all, if they're going in it for the money, they should go elsewhere. There's too many people in the business like me that just love the game and the passion for reasons I just articulated. And they're not going to win. And it's not a fun game if you're losing. It's horrible. I just told you how I respond to drawdowns.” — Stanley Druckenmiller

Something Buffett is well known for is his description of “Tap Dancing To Work”. In fact, there’s even a book named after it.

Perhaps you want to become a portfolio manager one day. This article will help you understand what it takes to win in markets. And why passion tends to be one of the first things employers look for in candidates in this field.

You’ve probably heard that passion is important to win in markets. But what does that even mean? What makes it so crucial for developing sustainable alpha? And how can an emotion from the heart be correlated with a logical investment outcome? This isn’t romance!

This article will spell out with detailed examples what it takes to become a proficient portfolio manager. By the end of this article, it will explain why not falling in love with markets is unlikely to lead to consistent outperformance in markets — value investing or not.

“No CEO has it better; I truly do feel like tap dancing to work every day.” — Warren Buffett, Berkshire 2012 annual letter

"As much as I still tap dance into the office, I'm excited about this transition," — Jeff Bezos on stepping down in his Amazon 2021 letter

TABLE OF CONTENTS:

1. Why Passion Is Important In Valuation

2. Why Passion Is Important In Business & Sector Analysis

3. Why Passion Is Important In Financial Statement & Accounting Analysis

4. Why Passion Is Important In Macro & Portfolio Management

5. What Tap Dancing To Work Really Means

Why Passion Is Important In Valuation

The first thing you’ll need to analyze stocks well is a good grasp of valuation. Typically, this involves understanding the basics of valuation, which usually means the DCF model. To oversimplify, the DCF model attempts to forecast the future FCF of a business and discounts those cash flows by an appropriate discount rate in order to derive the company’s fair value.

To digress, I don’t think most investment practitioners intend for the DCF to be used this way. While in principle the concept of enterprise value being the sum of its discounted future cash flows is true, it remains an extremely clumsy tool when trying simplify it down to a neat model. Almost anyone will tell you that the use of terminal value to represent business cash flows into perpetuity is unrealistic and unreliable. This is why you tend to hear investors discussing valuation on Bloomberg or CNBC in terms of multiples, rather than in terms of the discount rate they’re thinking of (I almost never hear this) — which is actually a more accurate barometer of uncertainty, rather than cost of capital per se.

In any case, the DCF model is still the current valuation standard and part of institutional inertia, so for now we’re still stuck with it. The biggest gripe you often hear when using the DCF model lies in the use of WACC — just changing the discount rate by 1% throws off the entire terminal value estimate so as to render the entire valuation worthless. Value investors will also criticize the use of beta in the WACC calculation to represent cost of capital — it’s a top-down methodology which assumes a static yield spread between a business’s cost of equity capital and borrowing costs, in stark contrast to the bottom-up methodology of how most businessmen think about shareholder return (i.e. profit dilution vs. uncertainty).

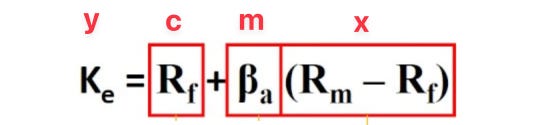

If so, how can we improve on it? If you start digging into the components of WACC, you’ll realize that it seeks to represent the cost of equity as a function of a regression analysis of its historical stock price. The general idea in statistics is that volatility equals risk, since it represents points in history where stock prices have deviated from the long-term mean trendline, thus introducing noise into further extrapolation of stock prices.

If you really think about it, the cost of equity formula is just y=mx+c. The fulcrum of this formula lies in ‘mx’ — where ‘x’ represents excess business returns over market returns, while ‘m’ represents the slope for extrapolating future excess returns from its historical trend.

I’m sure you can see where the problem with this assumption lies. Firstly, the world is chaotically non-deterministic and business returns do not behave nicely the way statistics does, so you can’t extrapolate future business returns from historical business returns in a straight-line manner. Even if you could, stock price trajectory on public markets add another dimension of chaos to the equation.

However, that doesn’t mean that the WACC formula is useless — one simply needs to know where its weaknesses lie, and make the appropriate adjustments for them. It’s like going to plane school and getting your 50-100 hours of pilot training under your belt, so that you know which switch to flip when the plane starts rocking side-to-side. This allow you to course correct for the imperfections within the WACC formula so that they more accurately resemble the real-life business conditions of a given circumstance.

…still with me? The point I’m trying to make is that one needs to be interested enough in markets to actually learn how to tear apart the engine of valuation and put it back together with parts leftover. This is before we even get into a discussion of efficient markets, whichthe DCF model is predicated on.

Why Passion Is Important In Business & Sector Analysis

Apart from valuation, a good fund manager usually also needs to have a deep appreciation for how different businesses and industries work. In this way, he can make the same course corrections in the valuation models as aforementioned for real-life business conditions, which is important since every business and industry operates differently. This is why you can’t apply a rule-based approach to valuation — a 10x multiple means something very different in an underperforming FMCG conglomerate vs. a risky venture-stage quantum computing business.

Rather than explain it, it’s easier to illustrate how having a good grasp of business models is key to understanding the different shades of grey when it comes to valuation. For instance, let’s start with valuing banks. While it’s conceptually true that bank valuations are a function of ROE x BV, their valuations (and worse, capital price trajectory) are based on so much more than that. Regional banks operate on different rules than money center banks, since the former tends to only be exposed to its local business environment. Measuring the risk exposure of money center banks requires understanding the Risk-Weighted Capital Ratio (RWCR), e.g. how the composition of risk-free assets to risky assets affects balance sheet health. Understanding the evolution of banking business models following the 2008 subprime crisis — from primarily spread-based lending to fee-based products — will lend color to why most large banks sport a Tier-1 Equity ratio higher than 10%1; and inform why management incentives are have changed since then. Moreover, understanding the intricacies of central banking with the financial sector is crucial to developing a matured understanding of bank valuations, since many generate tons of trading income while serving as quasi-government intermediaries in an economic regime flush with liquidity.

Then we get to European banks. Oh boy. Let’s move on to the O&G sector instead. Why does Buffett favor OXY so much?

First, it’s important to draw a distinction between deepwater drilling and shale (plus everything in between) — not only are their financial models starkly different, their operating models are nigh incomparable. Just focusing on the shale sector, one needs a good grasp of the history of the industry from the mid-00’s to today — how Oil Boom 2.0 emerged from the revolution of horizontal fracking, founding a race to the bottom amidst excess capacity and the subsequent fiscal discipline of the sector. After understanding how the shale winter of 2014 forced sector developments that dramatically improved unit costs, one should appreciate the uniqueness of the Permian Basin in the context of oil drilling and OXY’s position in it. Now you can start to look into the special capital structure of the Berkshire preferreds and why they resemble a fixed-yield investment for Buffett.

Since it’s topical, let’s try understanding the AI sector next. Firstly, it’s important to gain an understanding of how LLMs work — the conceptual basis of the pre-trained generative transformer and how these bad boys infer semantic meaning by comparing adjacent distances in vector space. At the base level, all of the flagship LLMs are largely commoditized in that they are pre-trained on the same data (i.e. all historical human knowledge) with relatively small model differences. This translates into relatively low differentiation between them from a commercial standpoint.

However, 2025 is poised to be the year of AI as each flagship provider is actively focusing on developing their respective application layers or “useful AI” in different directions. OpenAI has graduated from simply aiming for performance leadership to innovative applications of inference-time scaling with the reveal of o3 and OpenAI’s Deep Research. Users of Claude AI will recognize that it’s somewhat of a frontier model in the space, and has a current focus of integrating with the local environment (MCP and artifacts). Perplexity has been recognized by Jensen Huang as having revolutionized AI-powered search; while Gemini is leaning into its huge hardware lead in TPUs by enabling paid competitor solutions for their free users and sourcing inexpensively from the wisdom of the crowds using AI Studio. Also, who can forget open-source — with Meta’s Llama quickly becoming one of the top-used local LLMs, while Deepseek has leapfrogged the competition via its innovative use of pure reinforcement learning. Qwen is also making strides as evidenced by Apple’s recent decision to partner with Alibaba for AI, while the “indie” space is littered with a plethora of highly distilled reasoning models that can run on mid-tier consumer hardware.

Each of the flagship AI models are innovating in different business trajectories, demonstrating how there is ample pie in the sector for all of the flagship models to share. It also shows how the economics of the AI sector will evolve away from simply taking performance leadership towards designing valuable human-AI interfaces, and that 2025 will likely be the first year where we see laymen truly grasp the integration capabilities of AI beyond simply being a Star Trek tricorder. Investors in the sector will subsequently need to understand how these different business trajectories differ from the fundamental generative transformer abilities that AI was first known for, and how they will likely be integrated in their various specialist domains.

These aren’t the only complicated sectors that a generalist will have to understand— there’s also insurance, media, semiconductors, auto, petrochemicals, commodities, etc. It gets even more complex when there are overlaps between sectors, such as fintech being banking plus technology. As any sector specialist will tell you, I don’t think it’s possible to shortcut gaining a good understanding of each of these sectors — one really needs to just give it time and slowly accumulate knowledge in each of them. And unless you’re Mike Ross from Suits with a photographic memory, that requires having an interest in understanding these sectors, since you’re unlikely to see a dime of sustainable profit from such investments until you do.

Why Passion Is Important In Financial Statement & Accounting Analysis

Remember how we saw earlier that a business’s value is based on their discounted cash flows? Well that’s what financial statement analysis seeks to uncover — following the cash flows of the business.

To do that, one needs to be able to reverse engineer the numbers from a business’s financial statements — which is basically the opposite of creating the numbers from real-world conditions. For instance, the ROUA balance of an airline should tell you what their airline lease conditions are; so too should the SBC activity of a gaming company about their remuneration practices. The goal of reverse-engineering business numbers is to give you a map of real-world conditions, not to simply serve as financial inputs of a valuation model.

To do so, one needs to understand GAAP/IFRS accounting standards and their rules for translating real-world objects into standardized numbers. To illustrate the importance of this, consider how the accounting rules for leases were adjusted during the pandemic. The normal accounting treatment for leases (e.g. warehouses, airplanes, etc) is to derecognize and re-recognize a lease if any changes were made to the original lease terms. However, this practice was obviously counterproductive during the pandemic, when everyone was universally extending their lease tenures. Hence, a temporary exemption on lease reclassification was allowed by the accounting standards bodies to avoid gigantic and unnecessary mark-to-market accounting losses being recognized during already trying times. Understanding the effects of these gave investors and analysts more certainty when reconciling their cash flow impacts.

When investing in value factor stocks with single-digit multiples, I find having a good grasp of accounting standards to be invaluable when sifting through the garbage can for gems. When trying to tell the difference between a mispriced asset and a real dud, it makes a huge difference between being able to see the business assets at play and their respective cash flows, or not. This is in stark contrast to growth stocks, where asset value is typically quite visibly on display. While I can’t speak for everyone, my personal experience with these quasi-cigar butt type stocks has been that the mispriced value is usually hidden just beneath the surface — and that understanding accounting standards makes the difference between seeing past their short-term tragedies to the long-term asset values lying underneath. A great example of this is when I inferred from SE’s gross margin performance that they hadn’t been abusing free shipping vouchers by shifting delivery fees from COGS to S&M expenses (below the GM line) — that alone gave me the confidence to feel optimistic about their trajectory, since that was by far their largest cash burn component.

It usually takes years to accumulate the broad array of knowledge about accounting standards in order to be able to follow a business’s cash flows at granular detail. Being able to do so can mean the difference between having diamond hands when holding a deep value stock and losing your nerve amidst short-term volatility — and being interested enough to actually put in the time to learn about accounting standards requires one to be passionate enough about them to try and understand them.

Why Passion Is Important In Macro & Portfolio Management

Everything we’ve discussed up to now is arguably the easy part. The hard part about forecasting share price trajectory actually starts here — gaining a deep understanding of macro factors and how they impact markets.

As I’ve discussed at length before, this isn’t our grandparents’ markets anymore, where market prices are solely dictated by the Invisible Hand. We live in an economic regime where central bank interference in markets is not only tolerated, but expected — and boy does that impact stock prices. The recent inflationary scares over the past few years were in no uncertain terms contributed by excess Fed liquidity and TGA involvement (which significantly affects bank performance btw); whereas the inverse correlation between 10-year yields and policy rates can be explained by dynamics in real estate refinancing markets. The unravelling of the yen carry trade last year also had a significant impact on stock prices, while having a deep understanding of the contributing factors behind the strong dollar and the respective liquidity facilities at play would have most certainly calmed some market jitters.

Anticipating forex movements also requires having a good grasp over trade balances and geopolitics, while understanding the components of GDP can help investors see through the noise of scary headlines. This is before we get into truly advanced territory over topics like repo plumbing, central bank swaps or derivative impact on passive fund flows, which are the nightmare equivalent of learning in financial markets.

Then we come to implementation. Anticipating the portfolio impact of short-term share price trajectory is an exercise in managing portfolio beta, which requires having an understanding of the correlation of respective sectors and the beta factors at play within each position. The aforementioned central bank actions will also inform how stock prices fluctuate, and these need to be carefully monitored alongside other macro factors (like forex or trade) in order to be correctly implemented as portfolio management. It is also crucial to have at least some sense of how extraneous factors such as options activity and investor expectations impact share prices; and what kinds of black swan events can turn the tables on your portfolio correlations.

As one can imagine, getting a good grasp over these matters is not something which can be done overnight — it takes months just to understand all the financial levers on inflation, and years to understand everything else (that matters). Persevering through the time required to learn these lessons usually requires having a passion in markets.

What Tap Dancing To Work Really Means

This explains why employers tend to look for passion as a key ingredient in their candidates — it takes a long time to acquire these research skills, and someone who finds it boring is probably gonna tap out early. To be fair, there are most certainly easier ways to make money than spending years with your nose in a book — but it doesn’t change the fact that this is what’s necessary for sustainable alpha generation in markets.

As Druckenmiller alluded to above, there are just way too many people in markets who do it for the love of the game to make doing it purely for money tolerable. It’s a bit like soccer — if you’re not doing it because you enjoy it, you’re just not going to make the necessary investments to secure the skills required to consistently generate alpha. This leads to the natural human impulse to take shortcuts — which leads to all kinds of disasters in stock markets.

On top of that, the recent introduction of AI is going to dramatically switch up existing investment methodologies and cause everyone to stand on tiptoes. I can say without a shadow of a doubt that if you don’t start learning how to incorporate AI into your investment process, you are going to be overtaken by someone fresh out of college in 5 years time (outside of manager roles). The introduction of AI represents such a dramatic sea change to the equity research community so as to render many existing processes obsolete — and just like all of the aforementioned items, it takes quite a bit of time to learn how to effectively use it.

This hopefully provides a clear illustration of why passion is an indispensable element in the sustainable generation of market alpha. So is fund management for you?

Disclaimer: This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the authors. To the best of the authors’ abilities and beliefs, all information contained herein is accurate and reliable. The authors may hold or be short any shares or derivative positions in any company discussed in this document at any time, and may benefit from any change in the valuation of any other companies, securities, or commodities discussed in this document. The content of this document is not intended to constitute individual investment advice, and are merely the personal views of the author which may be subject to change without notice. This is not a recommendation to buy or sell stocks, and readers are advised to consult with their financial advisor before taking any action pertaining to the contents of this document. The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties and other factors, most of which are beyond the authors’ control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.might have changed post-pandemic

Nice article. Thank you