I’ve been reading up on some pretty decent research on PYPL, and initially I wasn’t planning to write “yet another PYPL article” about it. Yet something caught my eye — its long-term options are cheap given the risk:reward exposure. This article sums up my views about it.

I’m not going to rehash what others have already said about the stock itself — so if you want to catch up on PYPL’s stock, here are two great articles which will help you do so:

I’m just going to give a quick rehash of the bare minimum that you need to know before we start talking about PYPL’s options.

The Story So Far

Paypal has 4 main business lines — Branded Checkout, Unbranded processing, Venmo and BNPL/Crypto. Branded Checkout is the big yellow button that you see plastered all across the web — it has the highest margins and is treated as kind of a luxury product within the firm, but it has flat growth. Unbranded processing is like the hobo-version of Branded Checkout — it processes large volumes of payments but at significantly lower margins, but it’s growing at a steady clip. Venmo is a successful e-wallet with huge market share in the US; while BNPL/Crypto are exactly what their names imply.

The problem for Branded Checkout, the largest contributor to the firm’s margins, is that there is a healthy amount of competition in the form of Apple Pay, Shop Pay and Google Pay. It is seen as sort of a melting ice cube, which spells trouble given that it’s the firm’s golden goose. Unbranded processing has been tried-and-tested, and so far the verdict is that there’s too much competition from the likes of Stripe and Adyen for it to have any sort of moat — so it’s a race to the bottom in terms of margins, even as management leans on it to make up for the loss of Branded Checkout market share. Venmo is quite successful but has yet to contribute significantly to margins, while BNPL/Crypto are still in their nascent stages.

The big problem and the reason behind PYPL’s -10% share price drop last week wasn’t that revenues or even earnings decreased — it was that their transaction margins declined. This is being read by markets that Branded Checkout is further losing share and Unbranded processing is picking up the slack, which is not good news given how ultra-competitive the latter’s market is compared to the former. If the trend persists, there is a risk that Branded Checkout steadily loses share to Unbranded processing within the firm, which will further commoditize the overall business and potentially result in lower earnings despite higher revenues. Given that the margin gap between BC and UP is pretty large, there’s plenty of room to fall before margins stabilize at a worst-case equilibrium.

On top of that, the company has just welcomed a new CEO, Enrique Lores, who is taking over from outgoing CEO Alex Chriss. Chriss was unceremoniously fired from his position in a shock move to markets after three years of desperately trying to rehabilitate the company — so things aren’t looking great for the new CEO, despite his promises to the contrary.

However, the good news is that all the bad news has more or less already been priced into the stock. At 8x trailing PE, the stock has basically been left for dead with a 12% earnings yield and 14% FCF yield, where the company can basically buy up 100% of its shares within 6-7 years. Management has also announced cost-cutting measures which are supposed to free up more cash for additional capital allocation, which lends confidence that management will bring back operational discipline instead of chasing aspirational pie-in-the-sky goals of returning Paypal back to its former glory.

Successful Turnaround vs. Limited Downside

At this point, we are left with a company that is in the middle of a turnaround which could or could not materialize. The possibilities are bleak — past management has tried and failed to rehabilitate the company, the business is a conglomerate of melting ice cubes, and there are even rumors that it may be scrapped and sold for parts. It really could go one way or another, and for most people the risk of a binary event is just too much for their taste.

However, what if you could gain exposure to the upside of a successful turnaround without the downside of a persistent failure? This is where PYPL’s options come in. They give you optionality to the turnaround working out while limiting your downside exposure should it fail to materialize. Of course, the options premium themselves also represent a cost of entry, so let’s talk about that.

As aforementioned, the stock has already priced in all the bad news and more. The fact that the stock only fell -10% on the poor earnings release tells you that there’s a soft floor beneath the valuation, simply by virtue of how much it has already fallen. Conversely, this also means that if there is any whiff of a successful turnaround, the stock could easily double or triple from here.

To illustrate, imagine if management somewhat successfully engineers a turnaround and normalized EPS grows by 50% from here. This is not particularly hard to do, given that management has already announced that they are planning to reduce the share count by roughly 12% per annum (at current prices) and have announced drastic cost-cutting measures. In such a scenario, markets would most definitely be slightly more optimistic than they currently are about the company’s prospects, and may assign a 2x increase to the multiple (i.e. 16x PE). Combined, the two should result in the share price rising threefold to about $120 in a successful turnaround.

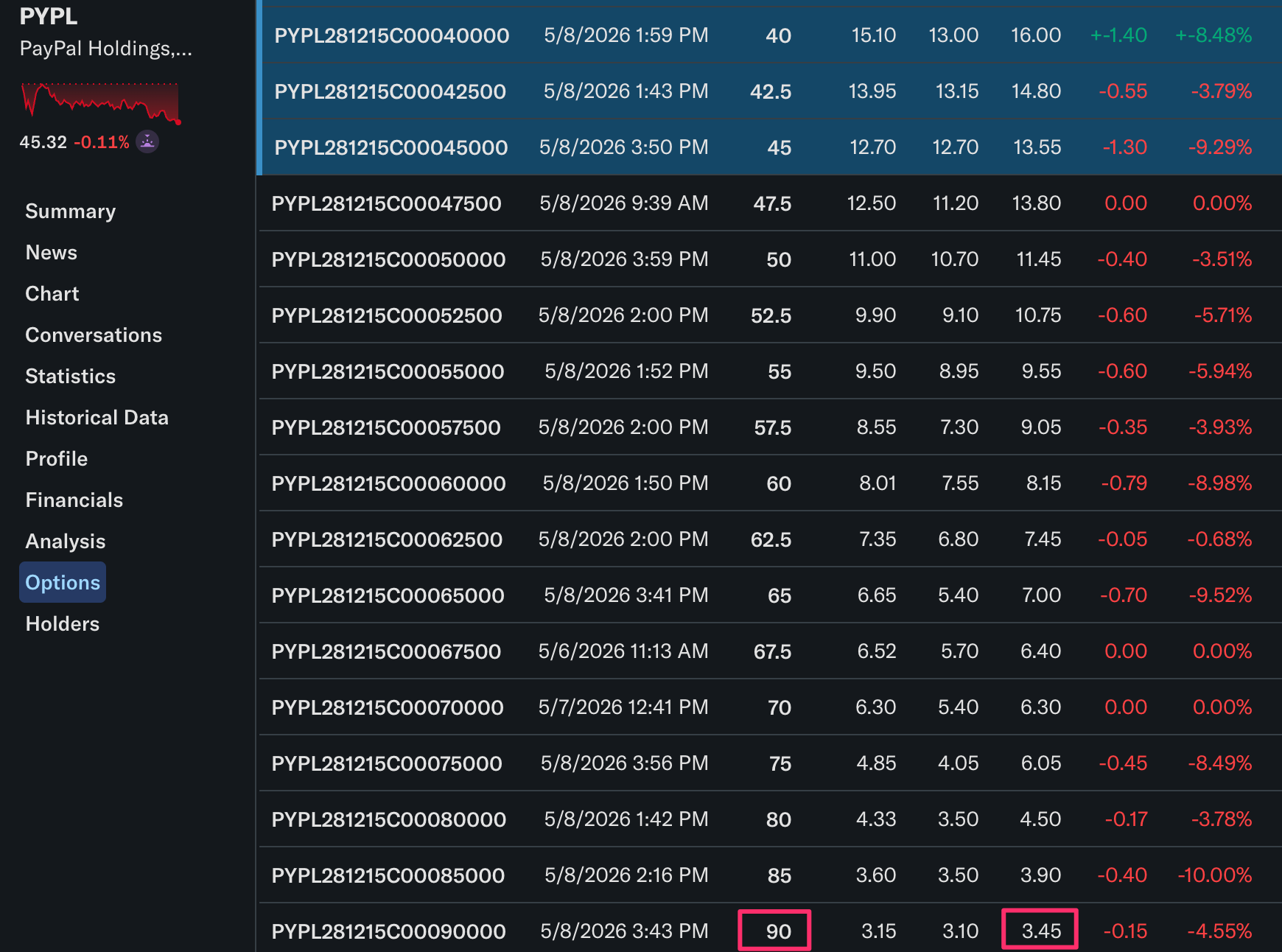

Now let’s take a look at their furthest out-of-the-money (OTM) call options with the latest maturity. As we can see here, PYPL’s Dec ‘28 options with a $90 strike price are currently trading with an Ask price of $3.45. That means the combined entry price you’d be paying would be $93.45/share, and you’d have until Dec 2028 to exercise them.

Compared to the $120 target price in a successful turnaround as aforementioned, that represents an upside of about 30% ($30 upside). And since the options expire in Dec 2028, we’d probably know by then whether the turnaround is successful or not.

What if the turnaround fails? Here’s the good news: you’re not participating in a binary event. Investing in PYPL’s options over their stock means that you can afford to be wrong about their turnaround, as the worst that could happen is that you lose $3.45/share. That represents a roughly -7.5% loss from the current share price, and that would be your maximum loss exposure. On top of that, you’d require much less capital invested to stay exposed than if you had invested in the vanilla shares.

What’s the risk:reward if the upside is $120 at a $90 strike price ($30 upside)? That’s a 1:8 asymmetric risk:reward bet, where you stay exposed to both sides of the turnaround coin simultaneously. Not binary.

Of course, you can play around with the numbers until you land on something you’re more satisfied with. But the way I see it, Paypal’s turnaround could happen or not, but if it does happen it won’t be a small event. It’ll be something big relative to the maximum loss of $3.45/share, even after accounting for the $90 strike. Imagine if it goes to $160 instead ($70 upside), that’s a roughly 1:20 risk:reward ratio.

I've generated income by selling PYPL puts for a hot minute. I also hold a little of the stock, and I am okay with owning a little more. Pretty easy game to play for the time being.