SEA Ltd: Starting To Look Like Amazon (Part 2)

In terms of capital structure

Nobody would call SE’s commoditized e-commerce business Shopee a wonderful business. But what would you call a business which had:

Rapidly improving profits

A negative capital structure

Is the largest incumbent in a 4-5 player oligopoly of a commoditized sector…

…where the industry TAM is growing at 22% CAGR, according to McKinsey?

Table of Contents (Part 2) SEA Ltd & The Three Business Segments: 1. Digital Entertainment (DE): Segment performance since IPO 2. E-commerce: Segment performance since IPO 3. Digital Financial Services (DFS): Segment performance since IPO 4. Fixed Costs: Lack of Operating Leverage Scroll to the end of report for: 5. AI-generated summary (250 words) 6. Download SE's 3-statement model (Excel with ready-made charts)

Disclaimer: This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the authors. To the best of the authors’ abilities and beliefs, all information contained herein is accurate and reliable. The authors may hold or be short any shares or derivative positions in any company discussed in this document at any time, and may benefit from any change in the valuation of any other companies, securities, or commodities discussed in this document. The content of this document is not intended to constitute individual investment advice, and are merely the personal views of the author which may be subject to change without notice. This is not a recommendation to buy or sell stocks, and readers are advised to consult with their financial advisor before taking any action pertaining to the contents of this document. The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties and other factors, most of which are beyond the authors’ control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.At the time of my first SE report in 2021, I conservatively assumed that SE’s E-commerce segment revenues would max out at 200% of their FY21 revenues as a steady-state concern into perpetuity. For reference, their FY23 e-commerce segment revenues has already eclipsed this benchmark.

I had valued SE at a normalized PE of 37.6x based on their share price of $70 at the time. SE 0.00%↑ is currently trading at $54, which would imply a normalized PE of 29x based on those earlier ‘startup’ assumptions.

Things have changed dramatically since then — with the Pinduoduo ex-China recently posting its first annual profit since its IPO. This necessitates a relook at its valuation model — based on actual real profits, rather than the startup metrics I had used in 2021. (e.g. Product Market Fit, Operating Leverage)

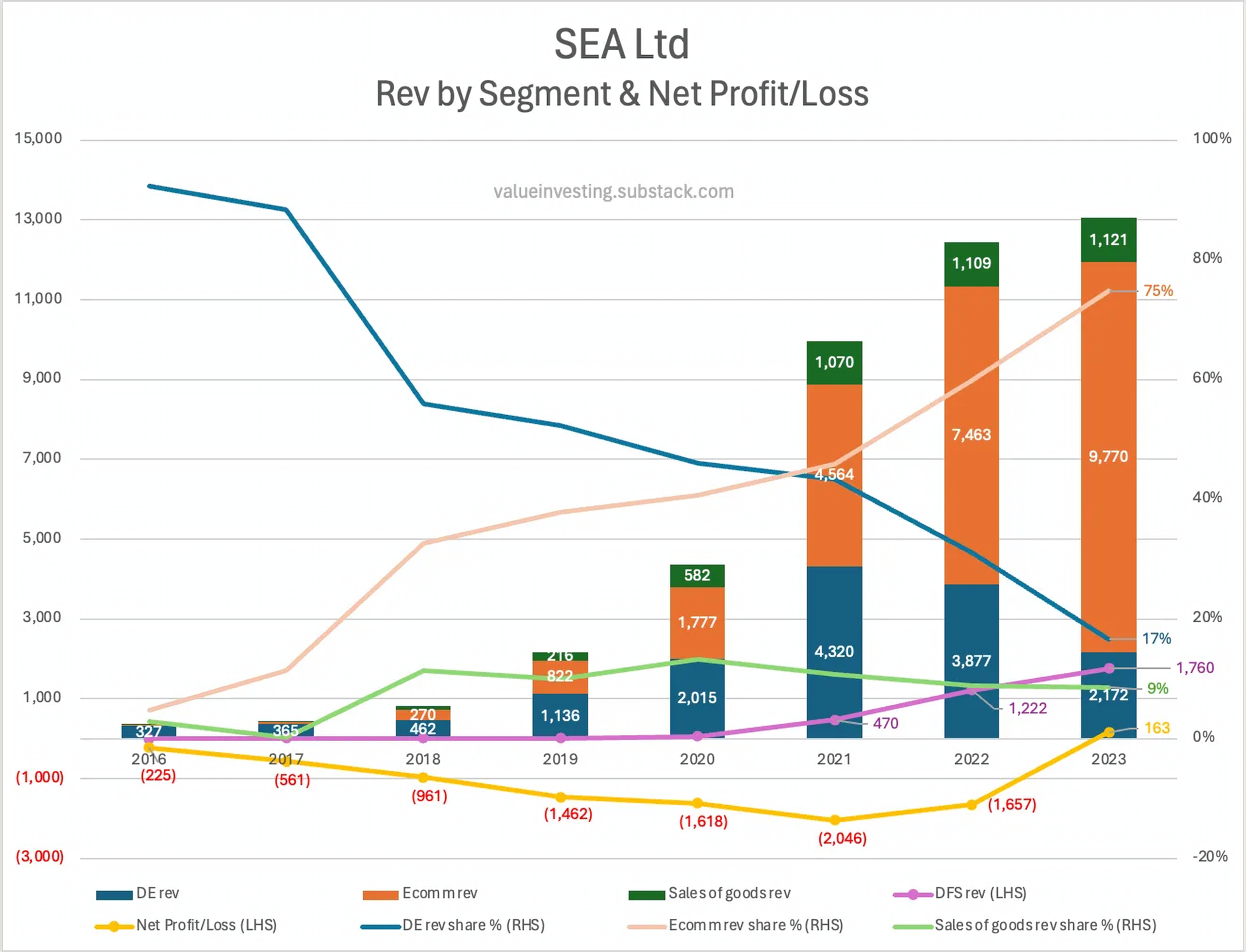

Understandably, many observers might be put off by SEA Ltd’s trailing PE of over 200x. However, this sky-high valuation obscures the fact that it is just newly profitable — having just rapidly grown its way out of deteriorating losses over the past two years. For context, look at their Net Profit trajectory (yellow line) in the chart below and try and imagine where it might end up in just a few years’ time:

In this Part 2 report, we’ll be performing a financial deep-dive into each of SEA Ltd’s individual business segments — in order to gain more color into the future performance trajectory of the Group. Finally, we’ll wrap up our analysis with our valuation of the company in the upcoming Part 3, using what we’ve learned in Part 1 and 2 for context.

As a refresher from our previous Part 1 report, their E-commerce arm Shopee is pretty much already the Amazon of the region today, with 30%-50% regional traffic share in a commoditized Retail industry where economies of scale reigns supreme. If you’d like further details, click the link below to see why I described it as “Pinduoduo ex-China”.

What the early Amazon investors saw

Article: 3,000 words, 20 minutes reading time, 1 Excel file, 6 original charts (best read on desktop)

Digital Entertainment (DE) — Segment Performance Since IPO

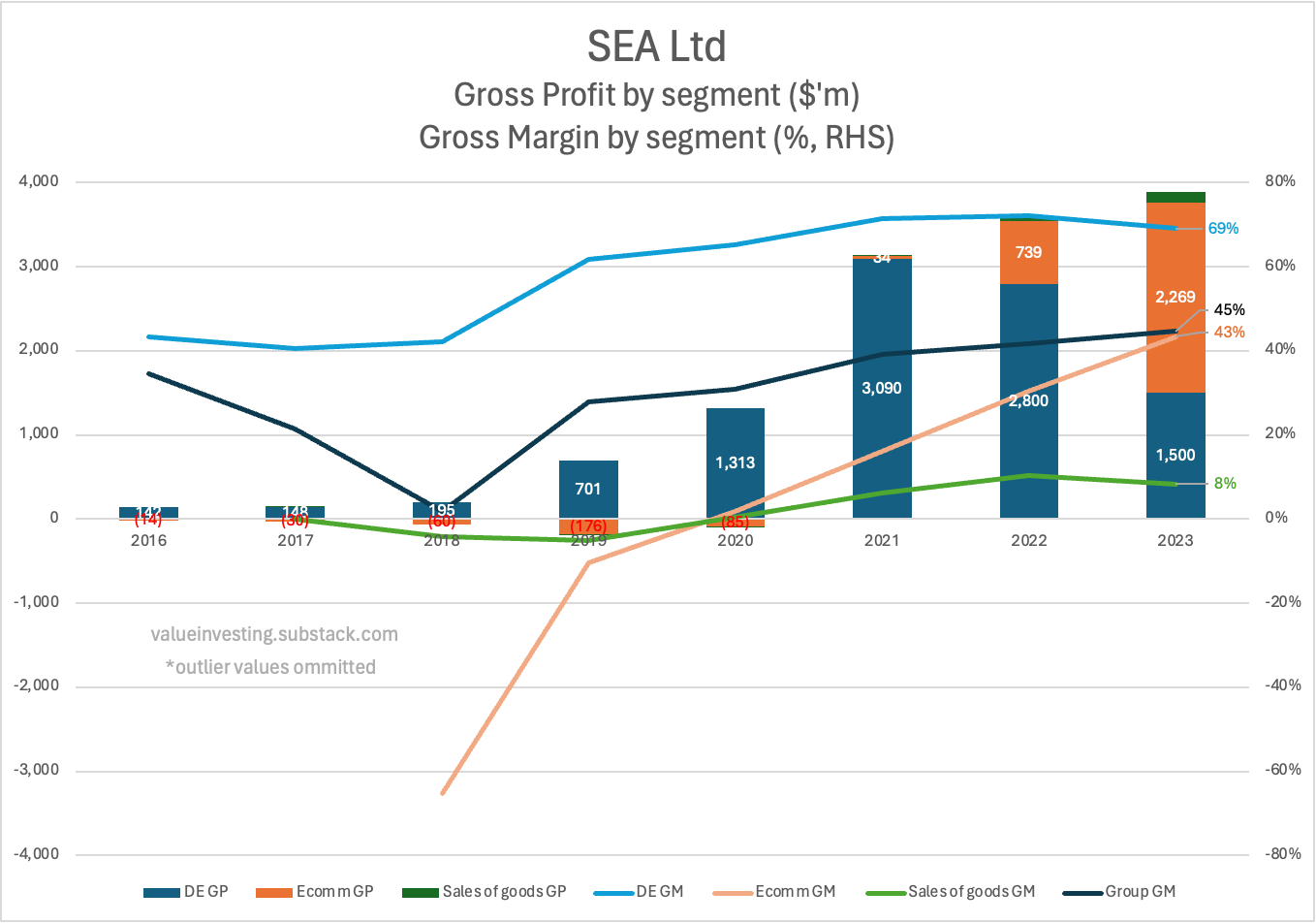

SE’s Digital Entertainment (DE) segment has historically been their main profit generator. As the chart above shows, nearly all of SE’s Group GP were attributable to DE segment GP (blue bars) prior to FY22.

This is largely due to two of their widely-recognized gaming businesses, the cash-churning Garena platform (similar to Steam, which takes a cut of game sales on their platform); and their hit mobile game Free Fire, which benefits from microtransaction abuse as explained in my Gaming Industry Primer. Both of these are highly cash generative, and have funded reallocated spend in other segments.

Keep reading with a 7-day free trial

Subscribe to Value Investing for Professionals to keep reading this post and get 7 days of free access to the full post archives.