Value Investing Substack Portfolio Review | Annual Letter 2023

The equal-weighted VIS Portfolio (US stocks) gained 11.5% in 2023 (no M7, details inside). Over the same period, DCA-ing into the S&P 500 gained 10.0% (ex-M7: 6.3%). VIS Portfolio 2022 updated too.

Highlights

On an apples-to-apples comparison, the equally-weighted VIS Portfolio matched or outperformed the S&P 500 in both up years (2023) and down years (2022).

This implies that the VIS Portfolio is a truly zero-correlation portfolio (in contrast to a high-beta portfolio) that can deliver results consistently through different macro environments via achieving superior alpha.

The VIS Portfolio managed to achieve higher or similar upside as the S&P500 with arguably significantly lower downside risk — by virtue of having a deliberate preference for significantly undervalued positions relative to intrinsic value. (i.e. high margin of safety with natural floor on downside + equal upside as fairly valued stocks)

The worst-performing US stocks in the portfolio chosen with this method only declined by -5% throughout the year. This resulted in a low-volatility portfolio with a high Sharpe ratio, making it suitable for a much wider range of investors than many other portfolios.

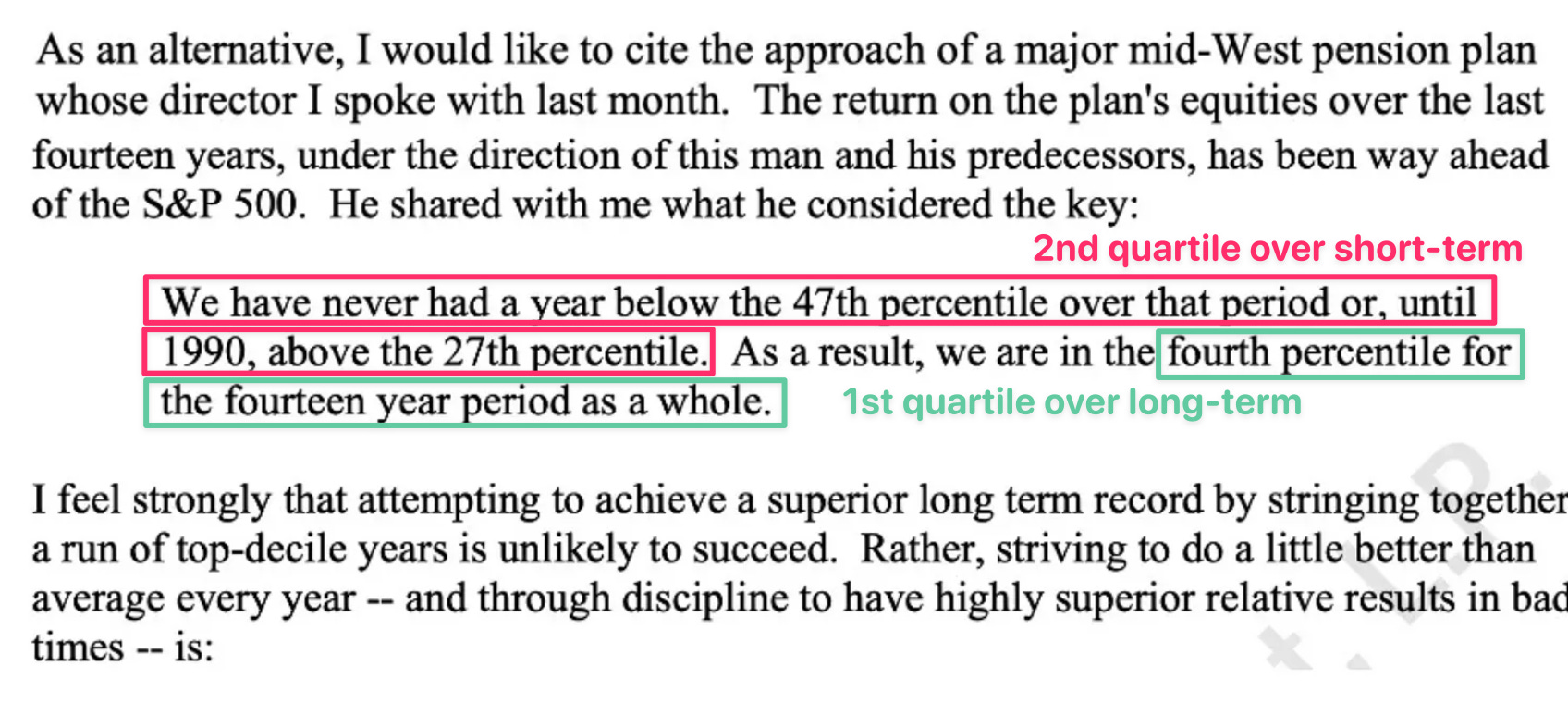

Howard Marks stated in his 1990 memo that LT investors in the first quartile of long-term performance tend to occupy the 2nd quartile of performance in the short-term, by virtue of being an Intelligent Investor with regards to risk-taking. I would humbly venture that the VIS Portfolio amply qualifies this criteria.

Around this time last year, I did a portfolio performance review based on all the stocks I had written about in 2022. This article is a repeat of that for all the stocks I had written about in 2023.

As most of you might know, I switched away from writing about SEA stocks to US stocks in April 2023 — and have detailed the reasons for doing so in this article. This explains why the performance of the stocks in the chart above are split between US stocks (blue bars) and non-US stocks (pink bars). The two yellow bars represent the overall performance of the equally-weighted VIS portfolio (more details on portfolio construction below) — one representing all stocks in 2023, and the other representing US stocks only (i.e. stocks written after April 2023). Lastly, the red bars indicate the performance of the respective benchmark indexes in 2023, assuming they were DCA’d into at the same time as the stocks under consideration.

The publication dates of the respective stock reports were used as the date of entry for each respective stock. These are all publicly available info on this newsletter and can be independently verified. As the stocks on this newsletter were not written with historical performance attribution in mind, an equally-weighted portfolio has been assumed for simplicity’s sake. This effectively produces an equally-weighted stock portfolio, assuming that positions were entered into in a DCA-style manner over time.

These same assumptions were applied to last year’s portfolio regarding the portfolio composition. Using the same assumptions helps with consistency when making comparisons across time, as we shall see below. Furthermore, it also allows easier performance benchmarking against the benchmark index funds. To recap, these assumptions are:

Same Portfolio Construction Assumptions as Last Year:

All the stocks in the portfolio have been invested in an equally-weighted manner (e.g. 7% each of 14 stocks for 2023 portfolio; 11% each of 9 stocks for US-only 2023 portfolio)

The stocks on this newsletter were acquired on its respective date of publication over time (i.e. DCA-style, hold cash otherwise); and a “buy-and-hold” value investing strategy had been exercised to-date (i.e. no stocks had been sold)

In the interest of brevity, please find the full explanations in last year’s portfolio performance review here. We’ve adopted all of the same criteria for this year as well.

I have omitted Dollar General (the last stock written in 2023) from this assessment, as it was published towards the final days of the year and wouldn’t have contributed much to the performance review (we’ll include it in next year’s performance review). For performance benchmarking of non-US stocks (before I switched), I’ve also included the same non-US stock indexes from last year’s review (which have all underperformed the S&P 500 in 2023). Lastly, the figures here do not account for share price declines due to dividends paid.

2023 VIS Portfolio Performance Review

As we can see in the chart above, the two yellow bars demonstrate that the equally-weighted VIS portfolio as aforementioned delivered 11.9% for all stocks written on this newsletter in 2023. Whereas the VIS portfolio (US stocks only) delivered 11.5% when only US stocks written after the switch in April 2023 are considered.

Meanwhile, the S&P 500 (Jan-Dec) benchmark index delivered +13.0% when an equivalent DCA-style approach is used (1st red bar). You’ll also notice that there are two other red bars titled S&P 500 (Apr-Dec) and S&P 500 (ex-M7), which delivered 10.0% and 6.3% respectively. The former assumes that the aforementioned DCA investments only began in April (rather than January) after I started writing about US stocks — to provide a more apples-to-apples performance comparison with the VIS portfolio (US stocks only) return of 11.5%. The latter is my estimate of the S&P 500’s full-year performance if the M7 stocks were stripped out (more details below).

Keep in mind that the S&P 500 owed most of its FY23 performance to the so-called “Magnificent 7”, which together make up an astounding 29% of the index by weight. As the right chart below shows, just 7 stocks contributed to 2/3 of its 19% gain throughout FY23 (i.e. non-DCA). The remaining 493 stocks in the S&P 500 only delivered a cumulative gain of 6% during the year. This is relevant because none of the stocks written about on this newsletter in 2023 were part of the Magnificent 7 (M7).

And yet the VIS portfolio (US-only, Apr-Dec) still managed to achieve an 11.5% gain during the year despite that, against the S&P 500’s full-year 13.0% (red arrow) or 10.0% Apr-Dec equivalent (blue arrow) — which would’ve involved holding onto M7 valuation risk throughout the year (e.g. NVIDIA). Perhaps a better risk-adjusted comparison would be the estimated 6.3% gain of the S&P 500 (ex-M7) above (red arrow); or the 6% FY23 gain (non-DCA) of the remaining 493 companies of the index shown in the bottom-right chart below:

As for how I derived the estimated S&P 500 (ex-M7) gain of 6.3% above, I was fortunate enough to have access to the daily share price data of the respective M7 stocks from Bloomberg. The way I calculated the 6.3% gain was:

Assume each M7 stock was DCA’d into at each date of publication, proportionate to their respective YE index weightings (i.e. same exposure as if one had DCA’d into the S&P 500 as aforementioned);

take the year-end performance of each M7 stock relative to each date of investment (according to said DCA method);

adjust each stock’s performance for their YE index weightings (e.g. MSFT 6.95%);

sum up the weight-adjusted performance of all M7 stocks;

deduct the performance of the weight-adjusted M7 basket from the total S&P 500 performance.

I know this description sounds complicated but it actually involves just a few really simple drag-and-drop functions in Excel. I’ll also be the first to admit that this isn’t the most objective way to estimate the S&P 500’s (ex-M7) performance in 2023 — but it’s likely within +/- 2% of the actual truth. If you’d like to verify the formulas I used, please download the Excel file that I used to calculate it below:

If we include non-US stocks before the switch, the VIS portfolio ekes out a meagerly higher 11.9% gain in 2023. It’s not shown in the chart above, but the average gain for those 5 non-US stocks was 13% in 2023. Compared to the 0.7% gain made by the MSCI ASEAN index, I’d say it outperformed.

Another important performance metric is the lack of downside volatility. If we look at the chart above, we can see that the largest losers for the year amongst US stocks were OXY and Disney — both shedding only -5% of their initial share prices by the end of the year. While it’s true that there are only 9 US stocks under consideration here, it makes the value investing methodology as described on this newsletter incredibly practical amongst a much wider range of investors. This allows the investor to stay invested without sacrificing the upside of a higher-vol strategy, by virtue of buying businesses cheap and dear.

And considering that 2/3 of the S&P 500’s performance this year was due to the traditionally high-volatility M7 stocks, I would wager that the VIS portfolio handily beat the S&P 500 on wider portfolio volatility as well — which would imply that it had a higher Sharpe ratio. If you’re interested in the theory behind why a value investing portfolio should deliver below-average volatility, I’ve explained it before in an earlier article:

Value Investors: How To "Buy & Hold" Forever Despite ST Macro Volatility

A quasi "All-Weather" Portfolio consisting of 20 Stocks (each with >1:3 asymmetric risk:reward) which can weather downside volatility from macro headwinds, designed for pure bottom-up value investors.

2022 VIS Portfolio Performance Review (2022-2023)

In the spirit of full accountability, this section will provide an update to last year’s 2022 portfolio performance review. As aforementioned, these are predominantly non-US stocks, as I had only made the switch to writing about US stocks in April 2023. Furthermore, I have omitted the stocks which I was “merely discussing”, as compared to the ones whose valuations I was truly interested in analyzing.

Netflix’s +160% gain and Meta’s +290% gain to-date might be less obvious in the chart above, as the chart’s axis was adjusted to better accommodate visibility for the performance of other stocks. You can click the link below to find out more if you’re interested in last year’s portfolio review.

The Value Investing Substack Portfolio Gained +16.6% In 2022, While the S&P 500 Lost -1.5%

Click here to read last year's portfolio performance review 2022.

The chart above updates last year’s chart for their latest share prices as of 31st Dec 2023. Again, the assumptions here are that a “buy-and-hold” value investing strategy was adopted, and that none of the stock positions were sold or adjusted since they were acquired. 2 years is not even half of a market cycle for a true LT investor anyway, hence I feel that this is a reasonable assumption to maintain.

Using the same criteria as above, we can see that the stocks written in 2022 achieved a 27.2% gain over the past 2 years — averaging that gives us an 12.8% CAGR for 2022-2023 (yellow bars). Meanwhile, the S&P 500 delivered a 21.3% gain over the same period; or a 10.1% CAGR (red bars). Both the MSCI ASEAN and MSCI World indexes underperformed the S&P 500.

Zooming out over the past 2 years also gives us some additional perspective on the S&P 500’s 13% gain in 2023 (non-DCA: 19%). As we can see in the chart above, the equivalent 2022-2023 CAGR was only 10.1% for the S&P 500. This demonstrates how stock performance in any given year does not tell the full story for the LT investor.

VIS Portfolio Performance Review Since Inception (2020-2023)

Once again in the spirit of full accountability, the chart above aggregates the performance to-date of all the stocks written since this newsletter went paid in Oct 2021. The same assumptions as aforementioned were used, and the chart has been readjusted to show the stocks in order, from worst-performing to best-performing (rather than chronologically).

We can see again in the yellow bars how the equally-weighted VIS portfolio slightly edged out the S&P 500 over this period — at 18.5% vs. 18.2% respectively. This implies a 2022-2023 CAGR of 8.9% vs. 8.7% respectively.

While many could be forgiven for forgetting by now, 2022 was a year characterized by outsized macroeconomic uncertainty and huge risks in various different fields. And it is in times of such heightened uncertainty that a LT value investing methodology really shines, owing to its lower risk (and volatility), thus allowing the investor to stay invested come rain or shine. It also goes to show that, as long as it might have felt, 2 years is far from considered “long-term”, and that investments over full market cycles must be considered to truly participate in LT returns.

Conclusion

In summary, it would appear that the VIS portfolio has managed to beat the S&P 500 on nearly all counts across varying time periods, except when benchmarked against 2023’s dramatic M7 outperformance. And it has done so by mostly investing in “value factor” stocks — which tend to have lower downside risk than “growth factor” stocks, and especially none of the overvaluation risk of the M7 stocks.

This means that the VIS portfolio managed to achieve higher or similar upside as the S&P500 with arguably significantly lower downside risk. Furthermore, the VIS portfolio was able to match or outperform the S&P 500 in both up years (2023) and down years (2022) — which implies that it is a portfolio with truly zero-correlation between its component stocks, and shouldn’t suffer from the significant drawdowns of high-beta portfolios. I would submit this as empirical evidence of asymmetric risk:reward, albeit only across a two-year timeframe.

I believe that demonstrating such outperformance over two years also reduces the chances that 2022’s 16.6% portfolio outperformance over the S&P 500 was just a fluke (S&P 500’s equivalent was negative in 2022). And if we strip out 2023’s M7 contribution and consider the measly 6% gain achieved by the S&P 500 (ex-M7) in 2023, the nearly 2x outperformance of the VIS portfolio in 2023 further emphasizes the relative outperformance of the value investing methodology as described on this newsletter. If you’d like a refresher on it, please have a look at some of my detailed value investing primers below:

Value Investing Primers

2nd-Level Thinking: Exploiting Inefficient Share PRICES (Supply vs Demand)

Why Investing with a 'Margin of Safety' Is Both Low Risk & High Reward - At The Same Time

Howard Marks once pointed out in his 1990 memo ‘The Route to Performance’ how risk-intelligent investors tend to occupy the 2nd quartile of performers in the short-term; but end up being 1st quartile performers over the long-term. I would venture that the VIS portfolio, as simple as its construction may be, qualifies this criteria. I look forward to repeating this performance in 2024, where value factor stocks appear to be beneficiaries given the prevailing macro environment.

Check out all of our US stock reports written this year below!

US stocks in the VIS portfolio: OXY 0.00%↑ EWBC 0.00%↑ COF 0.00%↑ PYPL 0.00%↑ SE 0.00%↑ GRAB 0.00%↑ INTC 0.00%↑ DIS 0.00%↑

What I love about value investing is how it will just sort of fly under the radar for a while, kind of treading water vs benchmarks for a few years, and then (in a bear market) just beating the bricks off of a momentum-based or even market-neutral portfolio. Nearly every decade has been like this.

You can tag your tickers in the article. I recently learned about this and am trying to share the info.

Tagging the tickers will improve Substack’s ability to find the article for people who are searching for that ticker.

For instance: “Apple (AAPL) $AAPL needs to…”

The Substack app, last I knew, didn’t recognize these $ ticker links yet. However, they work on web and e-mail.

I’m encouraging all stock analysis authors to begin using this system more. If we use it as authors, it creates a bigger incentive for Substack to develop it. The more Substack develops their stock searching features, the better it will be for all stock analysis publications on Substack.