Why AI Won’t Disrupt Intuit

Intuit owns the No. 1 brands in the US in two stronghold businesses: the Quickbooks brand of accounting software, and the tax filing brand Turbotax. INTU is one of the rare large-cap businesses on sale which is still growing fantastically — revenue growth was 15% YoY in 9M26, resulting in 20% Net Profit growth. The share price has collapsed on fears that AI will disrupt its seat-based business model, which if true has been completely invisible from its financial statements.

The general idea behind these fears is that a well-funded new entrant will somehow be able to vibe-code a Quickbooks alternative and start selling it for a lower subscription price. Firstly, INTU is no stranger to cheaper competition, with the likes of Xero and Zoho already competing with it in the more affordable accounting software category; and FreeTaxUSA and H&R Block literally offering free alternatives in the tax filing category. So the worry that Quickbooks or TurboTax will lose their pole positions to a cheaper AI vibe-coded alternative is just nonsense.

Secondly, there are high switching costs involved if a small business which has already been using Quickbooks for years wants to shift to an alternative. The small business owner, who is already strapped for time and resources, would have to reinsert years worth of accounting data into the alternative provider before they could start using it. Couple this with how time-sensitive and accuracy-sensitive such data is, and you can begin to see how it would be a nightmare to switch providers, whether AI is involved or not.

Thirdly, small businesses tend to pay for Quickbooks precisely because they don’t want the hassle of having to maintain their own accounting in an Excel sheet. The idea that they will suddenly shift to using AI to do their own accounting sits somewhere in the realm of fantasy, which anyone who has tried to do their own corporate accounting before will attest to. The probabilistic nature of AI transformers also suffers from hallucination, and is not well-suited for precise, exact tasks like filling in accounting or tax forms.

Fourth, TurboTax provides a 100% accuracy-guaranteed clause where they will pay your tax penalties if they file your taxes wrongly on your behalf. This sort of “soft” service is not replicable by AI, nor is the liability management that Turbotax offers.

Fifth, Intuit is already taking initiative on AI by partnering with Claude and OpenAI to embed AI solutions into Quickbooks, Turbotax, and Credit Karma. Far from waiting for a competitor to disrupt it, Intuit is readily disrupting itself with AI as the system-of-record to enable AI-assisted services for its customers. This means that not only would a competitor need to replicate all the private data stored on Quickbooks, it would also need to garner a similar partnership with Claude and OpenAI just to be competitive.

Finally, investors should not think of INTU as a Tech company that is ready to be disrupted by AI. In the same way that Apple is a Retail business, Quickbooks and TurboTax get their moats not from their technical capabilities but because of their brands. It’s the same phenomenon as Coca-Cola, as they’re the first names to pop into customers’ minds in their space when it comes to accounting software or tax filings.

>20% Growth at <20x PE

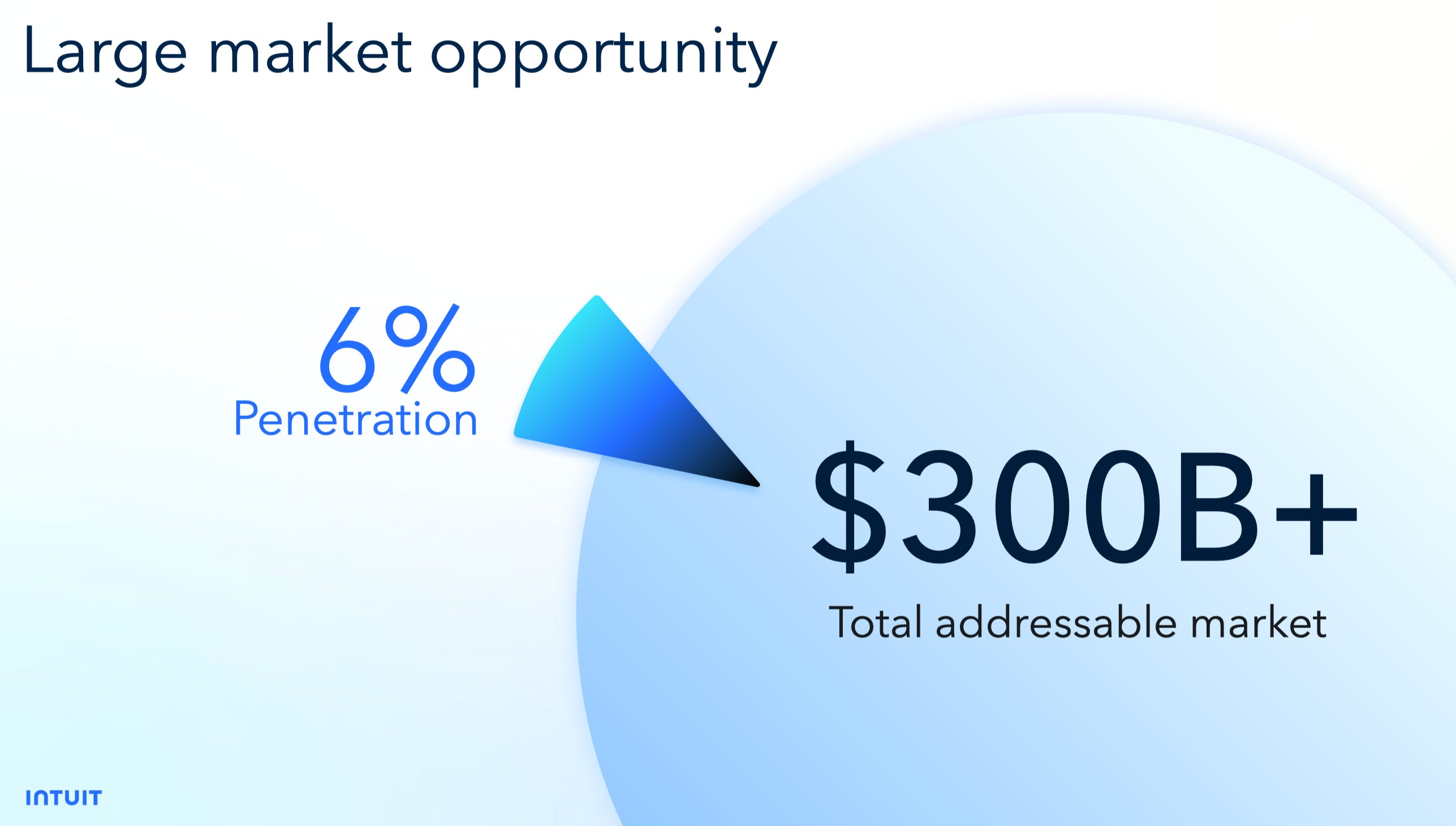

Despite its scale as a $80B market cap company, Intuit still has a large TAM opportunity to pursue. In fact, their opportunity is so large that analysts and investors of INTU typically do not give them brownie points based on their absolute revenues (as many “value” factor stocks tend to be measured) but in terms of how fast their revenue growth is. INTU today actually represents quite the opportunity for “value” investors, who are not used to seeing their companies post torrid revenue growth like this.

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.