GoDaddy: ADBE Without the AI Risk

Similar 14x PE with 20% Operating Profit growth from strong Pricing Power

What if I told you that there was a stock with a similar valuation & growth profile as ADBE, but with none of the AI risk? GDDY, the world’s largest domain registrar, is precisely such a stock — trading at a similar 14x PE as Adobe, with a similar 10% revenue growth, but without any of the catastrophic AI risk. Relative to an investment in Adobe, GDDY offers the opportunity to have your cake and eat it too.

The stock is down -50% over the past year and -22% YTD alone, largely reflecting analyst re-ratings from higher growth projections gone awry. In essence, the stock is normalizing back to historical levels as its Applications & Commerce (A&C) revenue fails to deliver on initial sky-high expectations — more on that below.

However, Core platform revenue is still growing healthily, and more importantly Annual Recurring Revenue (ARR) represents a whopping 87% of total FY25 revenues. The business is not difficult to understand — people need domains to start websites, and once they sign up they typically don’t shift registrars (I’ve personally been with GoDaddy for over a decade). And while there aren’t a lot of switching costs in the industry, people also don’t tend to change hosts just because of an infinitesimally small price hike, which GoDaddy is still pushing strongly as evidenced by ARPU growing by 10% in FY25.

Crucially, this is a management team focused on growing LTV/CAC, by investing in marketing in a methodological, data-driven way. From reading the earnings call transcripts, you get the feeling that management has a map of where they are going and the “GPS” of how to get there. We’ll discuss this further below about how it shows up in the Gross Margins and operating leverage of the company, as well as the KPIs we should monitor going forward.

Investors already entrenched in ADBE will find a lot to like in GDDY. Unlike the former, GoDaddy has significantly less AI disruption risk, yet possesses all the investment trademarks of the Photoshop giant from a valuation & capital growth standpoint. It also benefits from the same recurring sales business model, with none of the seat-based risk that AI can disrupt. The company has plenty of cash, and is diligently reducing outstanding shares at a mid-single digit rate annually. Combined, there is a decent expectation for 20% normalized EPS growth, reflecting a potentially underpriced asset at its current 14x trailing multiple.

Business Model

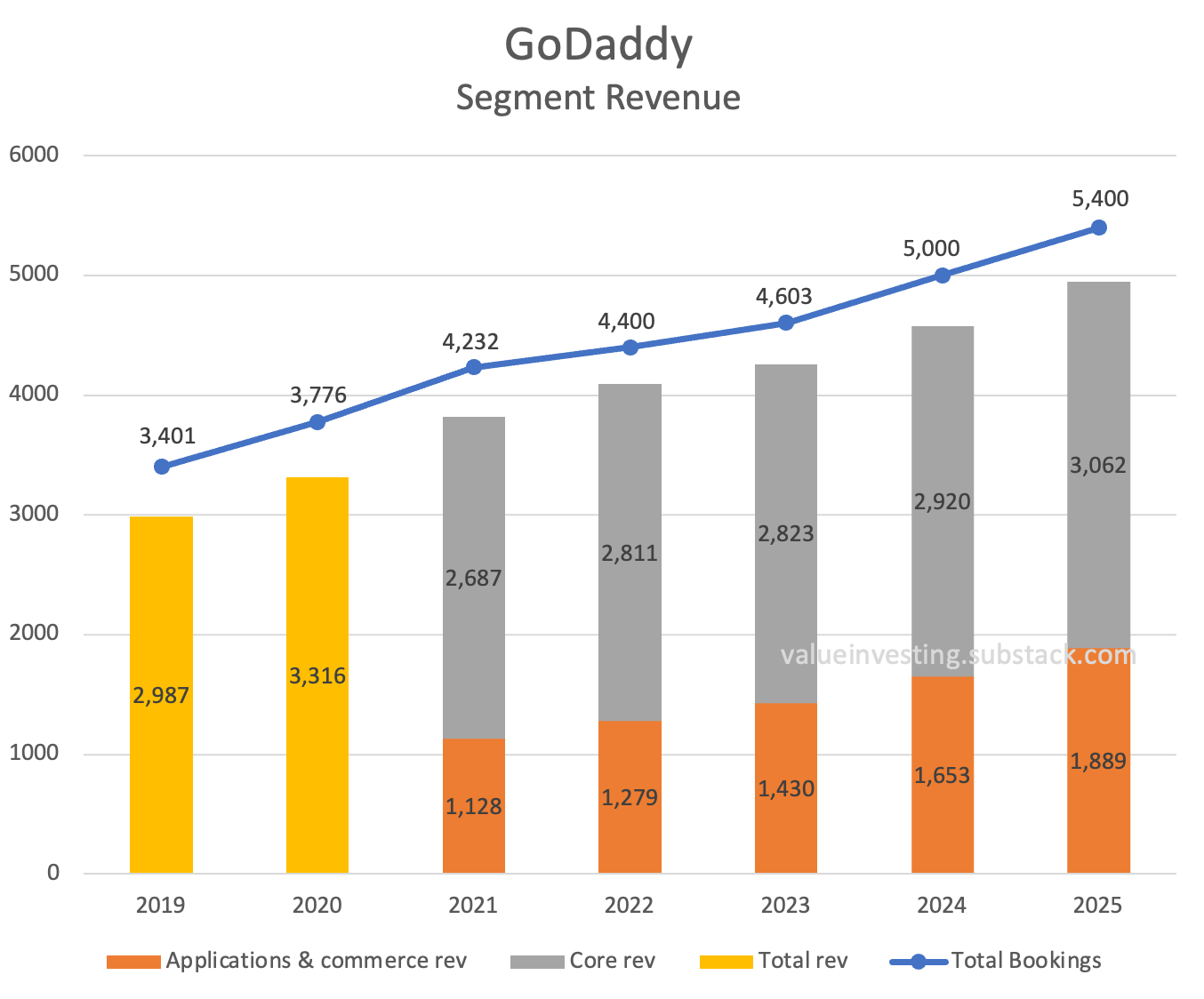

While GDDY reports its revenues under two separate segments — Applications & Commerce (A&C) and Core — they are both the same set of experience to the customer and should be seen as two parts of a bundled offering. Core represents the domain registrar and hosting parts of the business, while A&C represents the Websites + Marketing add-ons that so-called high-intent customers (those with >$500 in ARPU) sign up for in addition to the Core offerings.

Management measures success based on 5 KPIs: 1) Traffic, 2) Conversion, 3) Attach rate, 4) Activation and 5) Renewals. Traffic represents the top of funnel that GoDaddy uses to attract new users via its domain signups, while Conversion represents how many people actually sign up for a new domain. The Attach rate represents customers who sign on for a website or marketing add-on where the real ARPU uplift comes from; while Activation measures high-intent customers via their actions such as setting up a new website or first login. Finally, the four KPIs combine to inform how successful GoDaddy is at encouraging customer Renewals.

Hence, the business model is simple: first, get people into the top of funnel via discounts or promotions, then convert them into paying customers for domains & hostings. From there, data is collected on customers to see who might be potential high-intent customers, and then marketing investments are made targeting those high-intent customers with the goal of upselling and cross-selling secondary offerings. Finally, a high-intent customer is more likely to engage in persistent renewal of services, which represents ARR to GoDaddy.

As aforementioned, the high-intent customer is someone who spends an ARPU of $500 or above. Given that average firm-wide ARPU was only $242 in FY25, there is real revenue uplift from targeting and gaining each new high-intent customer.

Subsequently, GoDaddy uses its AI solution Airo to surface high-intent customers by shepherding small or micro business owners through their product inventory. Airo helps customers not just by automating day-to-day work tasks; but also provides direct agentic advisory through its Airo Care function, which helps small business owners through providing business insights via the 30 years of data inventory that they have on small businesses. This process aims to surface high-intent customers as customers gradually recognize that GoDaddy is able to do more than just host domains and build websites, resulting in higher average order size, higher attach, higher retention and higher renewal. For example, nearly 10% of new bookings in FY25 was attributable to a customer having a touch-point with Airo Care.

Hence, attaining ARPU expansion is a mechanical process of surfacing solutions for high-intent customers via appropriate pricing and bundling. This is done by asking questions like: how to add incremental value to the customer, or what is the right bundle of products they should have for their stage in the business? What are the different attached products that make sense for what they’re trying to do? In this way, GoDaddy expertly bundles business solutions with the domain product driving not just ARPU but ARR growth too.

On retention, there is plenty of data showing that when a customer signs up for a second product, their retention is significantly higher than normal. Hence the tertiary objective is to get the high-intent customer to sign up for a third or fourth product, whereupon the retention rate skyrockets.

In summary, the business objective of GoDaddy is to attract, retain and renew the high-intent customer with an ARPU of $500 and above. This is achieved by reeling in new customers through the sales funnel of domains and hosting, then surfacing further sales intent using a methodological, data-driven approach which tests the waters over what customers want and where to invest incremental marketing dollars. Subsequently, they upsell value-added services to targeted customers by bundling attractive solutions for the entrepreneur, and further cross-sell products in order to encourage retention. Finally, they build on the retention of multiple products to get the high-intent customer to renew in the form of high ARR. These efforts are ultimately expressed in the financial performance of GDDY, which tells the story of how the business model as described above is performing and will continue to perform.

Financial Analysis

download Excel model below

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.