Comcast at 5x PE

Analyzing the bankruptcy risk, and what the downside looks like from here

Amidst record-high valuations in equity markets today, it can be hard to find stocks which are valued appropriately. Comcast is one of them, with the stock trading at just 5x trailing PE and down nearly -50% over the past 5 years.

The investment case is simple: as long as they’re able to service their debt adequately, the stock is priced at a straightforward 20% earnings yield, which is hard to beat. By comparison, NVDA which trades at 40x PE only yields 2.5%, which needs to grow by 800% (11% CAGR over 20 years) just to match CMCSA’s current yield today. Or put another way, at 20% yield you’d be breaking even on your investment in just 5 years. That’s some serious math.

Perhaps more importantly to shareholders: what’s stopping CMCSA from dropping another -50% from here? That’s what our “risk-first” value investing analysis aims to answer. If investors can put a floor on losing money in CMCSA, I think many will agree that the current valuation is highly tempting. Hence, we’ll do a financial deep-dive of CMCSA in this report to analyze what the downside could look like for Comcast.

This CMCSA analysis will apply a margin of safety approach to the valuation, and identify which are the biggest needle-movers for the stock that could impact its mouthwatering 20% earnings yield. Given the super-low valuation, this eschews the need to look for needles in haystacks and simply reduces the analysis to “what else could go wrong from here?”. It will be a very risk-based analysis and simply aims to preserve the straightforward 20% shareholder yield thesis, by identifying problem areas and without having to make any heroic assumptions about growth.

The Important Math: Debt

As aforementioned, the general thesis is to ensure that CMCSA manages to deliver its headline 20% yield without there being any nasty surprises up its sleeve to disappoint shareholders down the road. In this sense, debt serviceability is paramount and we want to ensure that their debt load has no potential for turning into trouble sometime in the future.

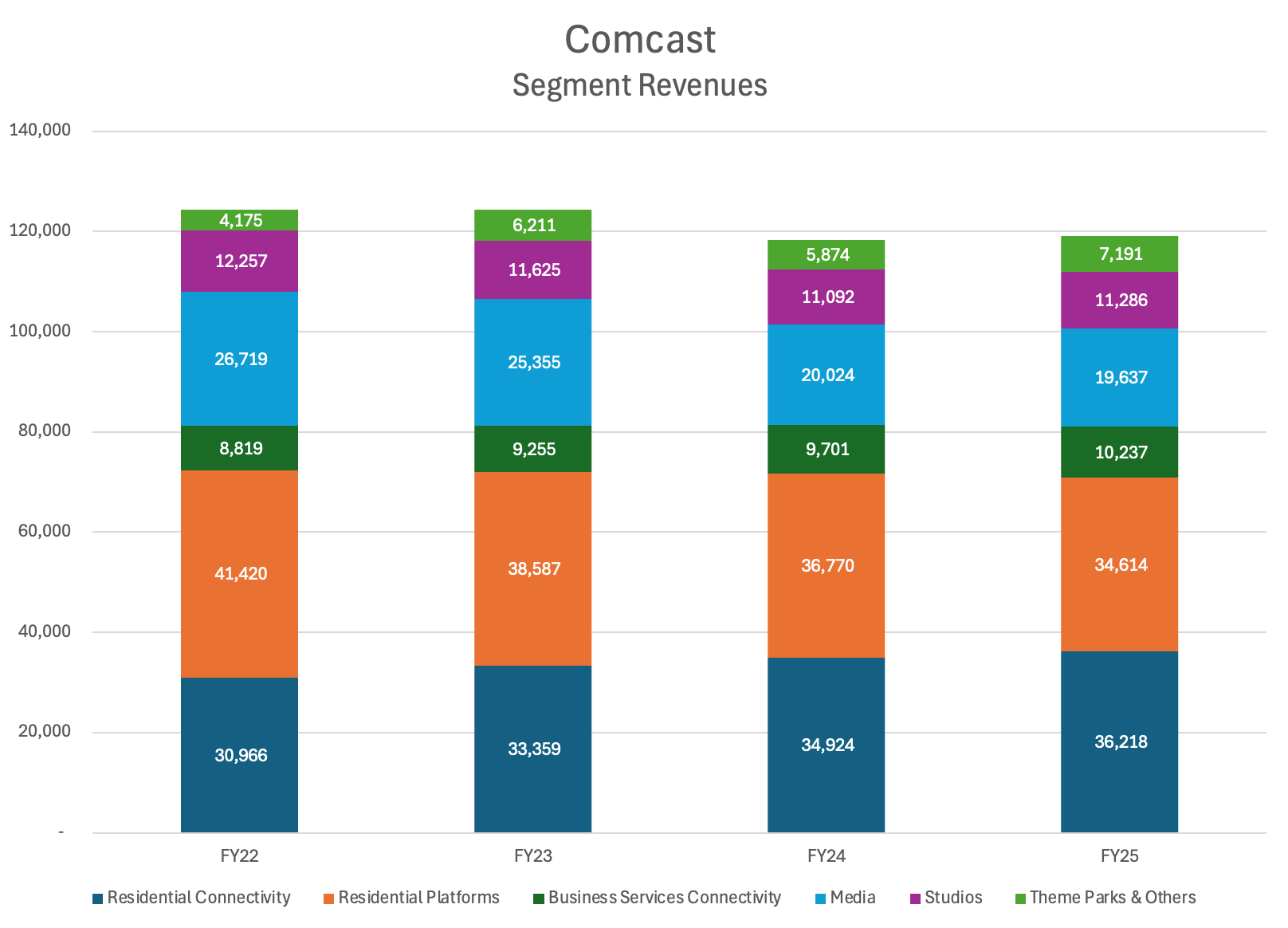

Firstly, it’s heartening to see that like-for-like Total Revenues are actually still growing. This demonstrates that CMCSA actually has other healthy businesses, despite its Broadband business (20% of revenues) getting all the headlines for being a melting ice cube.

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.