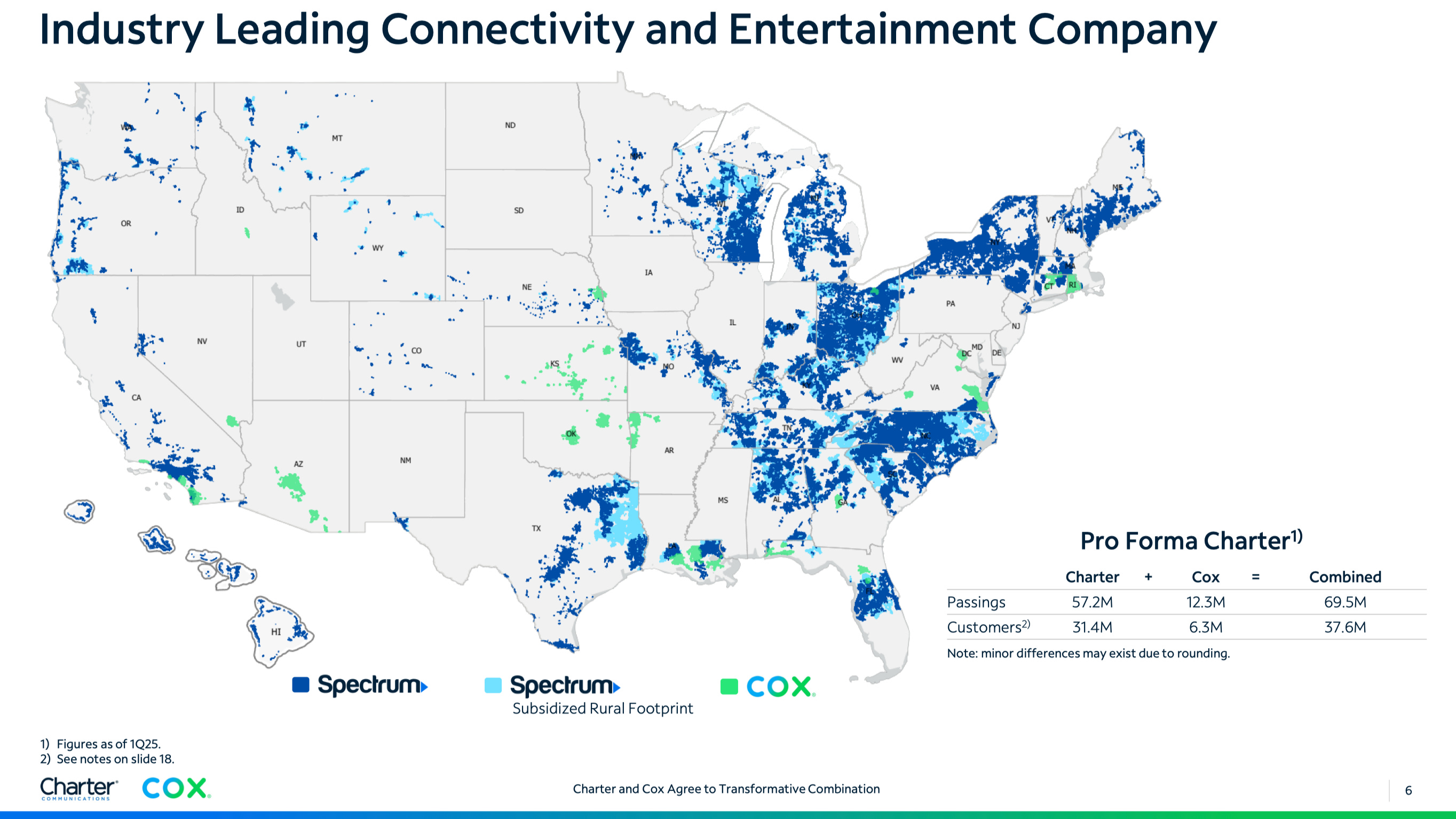

Charter is the 2nd largest provider of broadband internet in the US, after Comcast. Currently, its equity is yielding in excess of 28% at 3.5x PE, and investors rightfully want to know what’s the catch. In this article, we’ll explore:

Charter’s business and its debt situation

The Cox merger and the post-merger valuation

Why its Internet business is NOT the melting ice cube to be concerned about

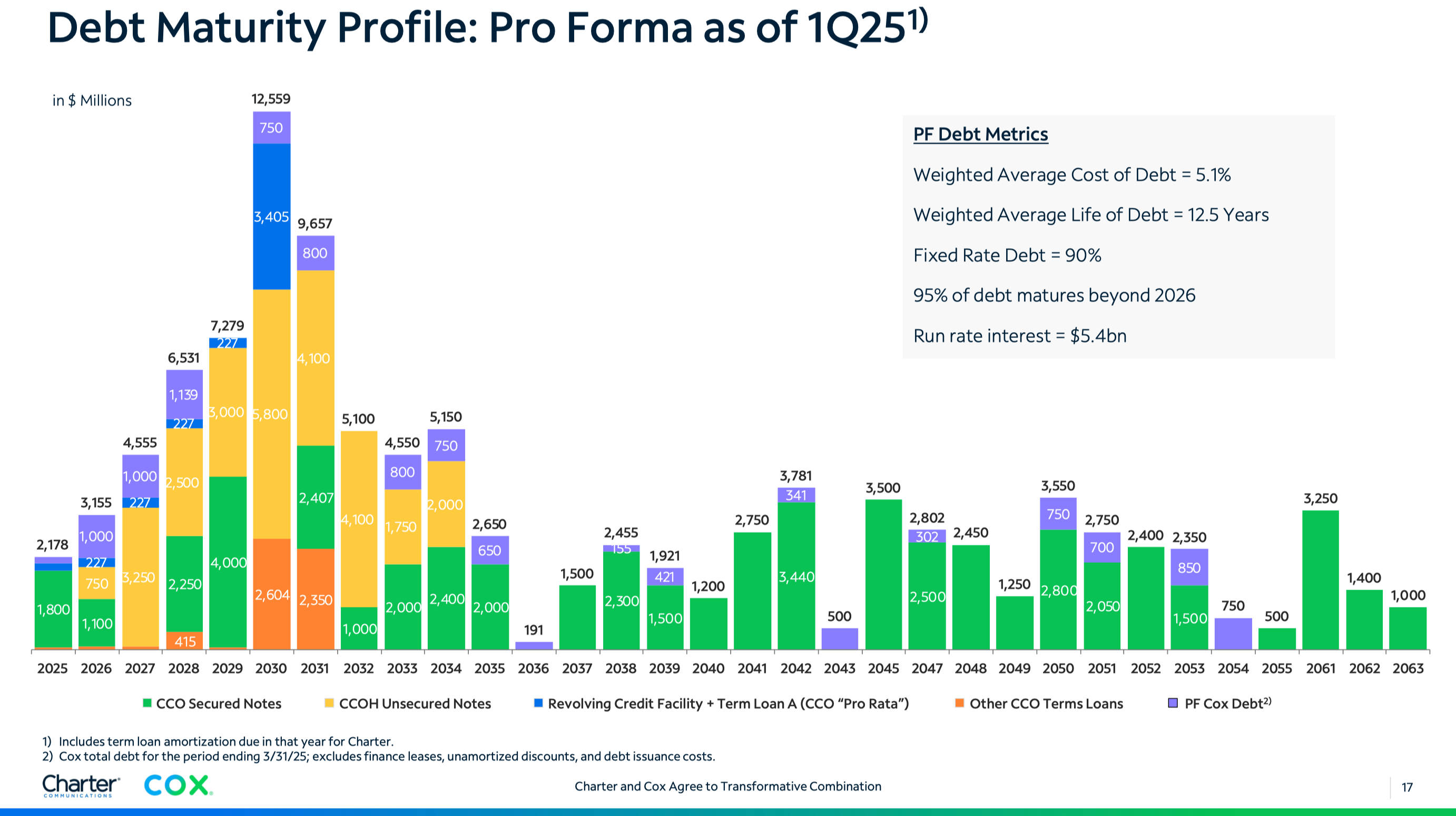

First things first. There’s a good reason why Charter’s PE is so low — it has a lot of debt. As of FY25, Charter held about $95B in Net Debt, which is humungous relative to their market cap of $16B. It’s probably worth pointing out that CHTR bought back its shares at a 9% CAGR since FY21, so their market cap could’ve been nearly double what it is today even at the prevailing share price.

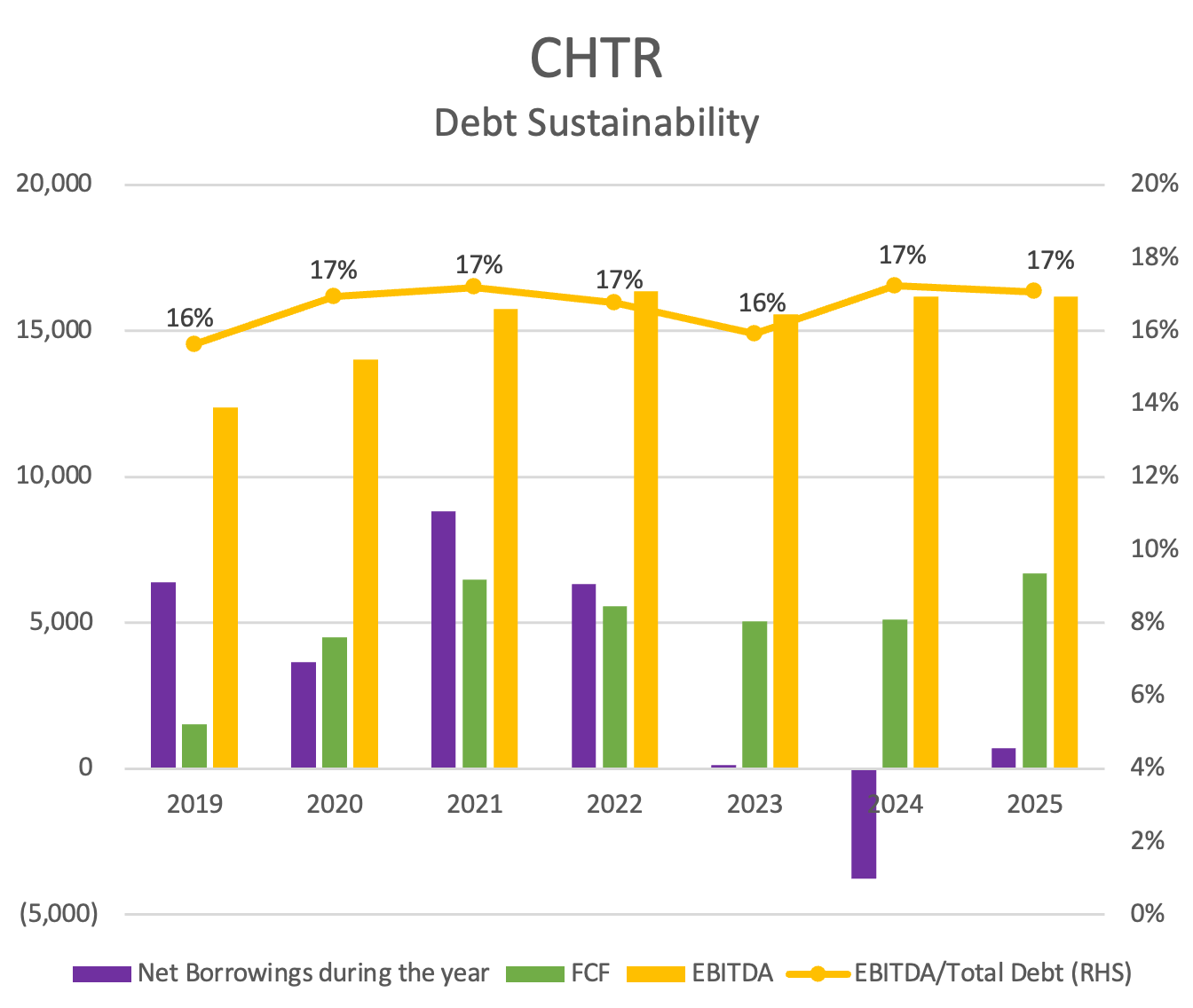

However, this debt is highly manageable. Firstly, 90% of the debt is fixed rate in nature, so there’s very little interest rate risk. Secondly, most of the debt is maturing in staggered stages, with the exception of two balloon payments in 2030 and 2031 (which will likely be refinanced), so the debt payback visibility is high and there’s little risk of bankruptcy. We can see below how CHTR’s debt is easily managed (FY25 FCF: $6.6B) and can be refinanced to further stagger out the debt stack as they have done before.

The chart above shows how CHTR’s Net Borrowings are very manageable relative to both their FCF and EBITDA. Furthermore, EBITDA as % of Total Debt has been quite stable, hovering at between 16-17% over time.

The implication here is that CHTR is able to service its debt, and is not taking on more debt over time in order to service past debt obligations. The debt load is simply a static fixture of the capital stack. This demonstrates how unlikely it is that things will come crashing down anytime soon as far as the heavy debt load is concerned.

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.