VLRS: Lowest-Cost Airline in the World in 2020 (Part 1)

VLRS: Lowest-Cost Airline in the World in 2020 (Part 1)

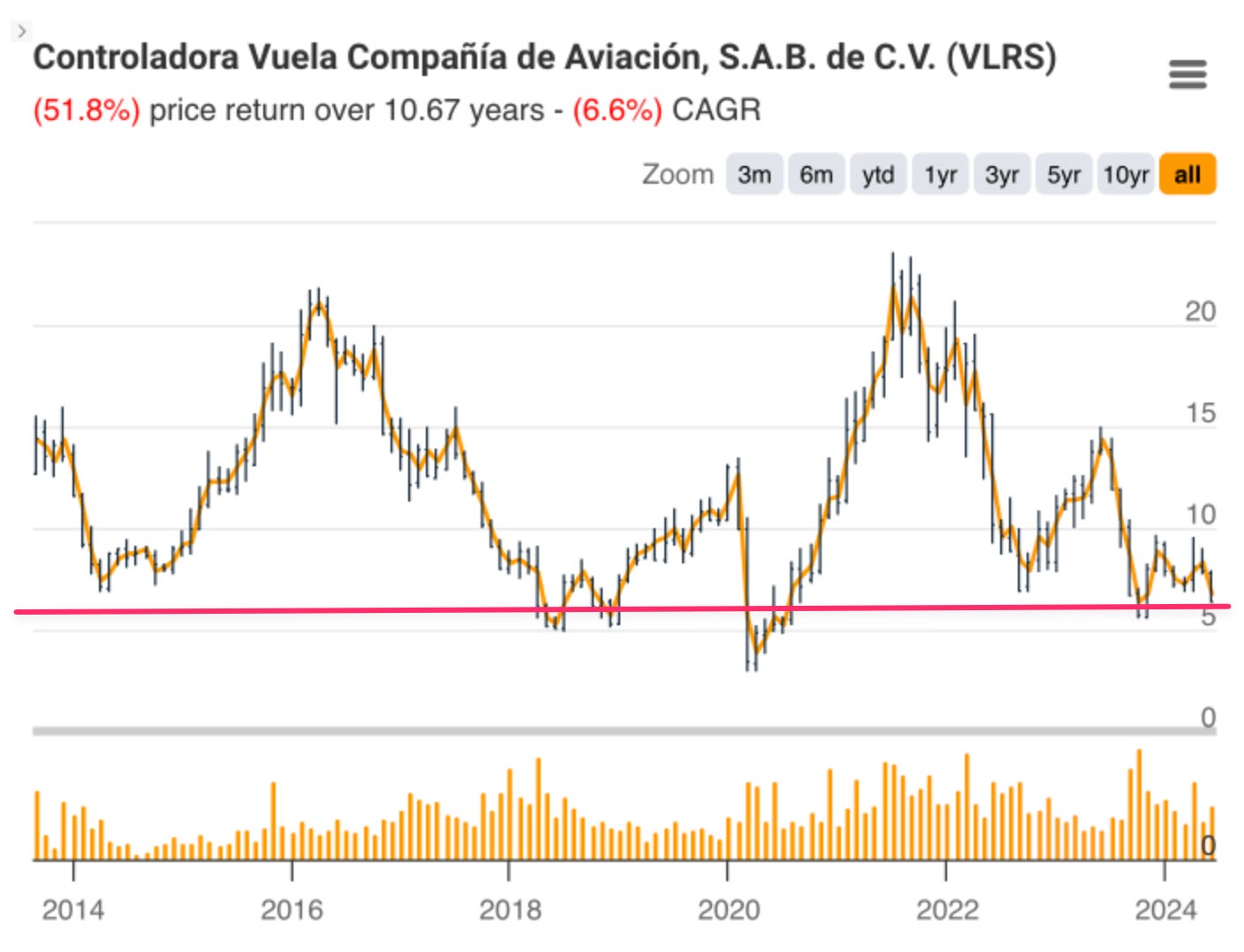

3rd lowest share price trough in its history (including pandemic)

VLRS Revenue deep-dive: Identifying VLRS's key revenue growth levers

1. Ancillary Revenue Growth is the way

2. Generating Passenger Volumes vs. Higher RASM

3. Doméstica o Internacional?

4. Improving Fleet Utilization - Squeezing more toothpaste out of the same tube

5. What's The Pratt & Whitney Situationship?

6. 📊 VLRS 3-Statement Model (download here)

Disclaimer: The contents of this document are NOT meant to serve as investment advice. Read our full disclaimers below.

VLRS is the largest Mexican ULCC (ultra low cost carrier), and is widely considered to have one of the lowest unit costs in the world. In fact, it was the No. 1 lowest-cost publicly-traded airline globally in 2020 — and has consistently been the lowest-cost publicly-traded airline in the Americas.

VLRS’s customers are mainly what the industry calls “VFR” flyers (visiting friends & relatives), which are composed of the substantial Mexican immigrant community working across the US border — who frequently flies back and forth to visit family during holiday seasons. As you can imagine, these are typically casual flyers who tend to book flights way in advance to save on flight ticket costs. However, unlike your average leisure traveller, they are an incredibly reliable and growing recurring source of revenue for VLRS.

VLRS and the other two domestic airlines also compete with the Big 6 US airlines when it comes to transborder travel between Mexico and the USA — which makes up about 45% of their total revenues. As you can imagine, the former group have a significant cost advantage in this commoditized market, with the USD:MXN exchange rate at 1:18:

Outside of international travel, VLRS also has plenty of growth runway in the form of domestic travel. Mexico’s travel industry still largely revolves around buses — the domestic bus industry sees 3 billion passengers annually, despite nearly 25% of such trips being of a sufficiently long distance (e.g. >6 hours) to consider taking a flight instead.

In stark contrast, Mexico only saw 120M flying passengers throughout FY23 — a whopping 3,000% less than annual bus passengers. This implies that Mexico’s domestic airline industry TAM has practically unlimited growth, simply from converting bus passengers to air travelers as the country’s per capita income grows.

The slide above shows how converting just 1% of bus passengers to air travel would yield 31M additional air passengers — equivalent to long-term industry TAM growth of 25%.

There’s also a macro story here, in light of US firms nearshoring their industrial/manufacturing operations from China towards Mexico. While this isn’t directly related to VLRS’s ULCC industry, the outsized growth implications from this macro trend is bound to increase the average discretionary wallet Mexico’s burgeoning middle-class population — which will bode well for VLRS’s top-line.

On top of that, Mexico is projected to experience phenomenal growth of their working age population, at least relative to most developed economies. The slide above shows the population pyramid of the country’s demographics, highlighting the organic growth tailwinds blowing behind the domestic ULCC industry — as the working age population continues to grow both in size and income levels.

This is where the commoditized nature of the airline industry reveals its double-edged benefit — people will naturally gravitate towards the cheapest flights, and Mexico’s burgeoning middle-class will serve as practically unlimited growth for VLRS. This is why I describe VLRS as the Southwest Airlines of Mexico — they are pretty much where Southwest was in the 70’s, when Herb Kelleher founded the LCC model that has become the baseline for the global airline industry today.

Another point to highlight is the recent restoration of Mexico’s airlines to Category 1 status by the FAA in Sept 2023. If you’re unsure what this is, all you need to know is that it’s basically an upgrade in Mexico’s flight safety ranking that will continue to improve air traveller volumes for all Mexican airlines, including VLRS.

As expected from the highly cyclical airline industry, most of VLRS’s recent woes have mainly been due to excess competition. There used to be 4 major Mexican airlines — but Interjet filed for bankruptcy last year after the pandemic brought a crushing conclusion to some overstretching they had committed to prior to the pandemic (e.g. ordering too many planes).

Prior to its collapse, Interjet had engaged in a multi-year price war in a desperate bid for liquidity. This depressed prices across the industry, which affected VLRS and the other two competitors. However, it also presented a once-in-a-cycle opportunity for the remaining airlines to pick up Interjet’s assets (planes & routes) following the latter’s collapse.

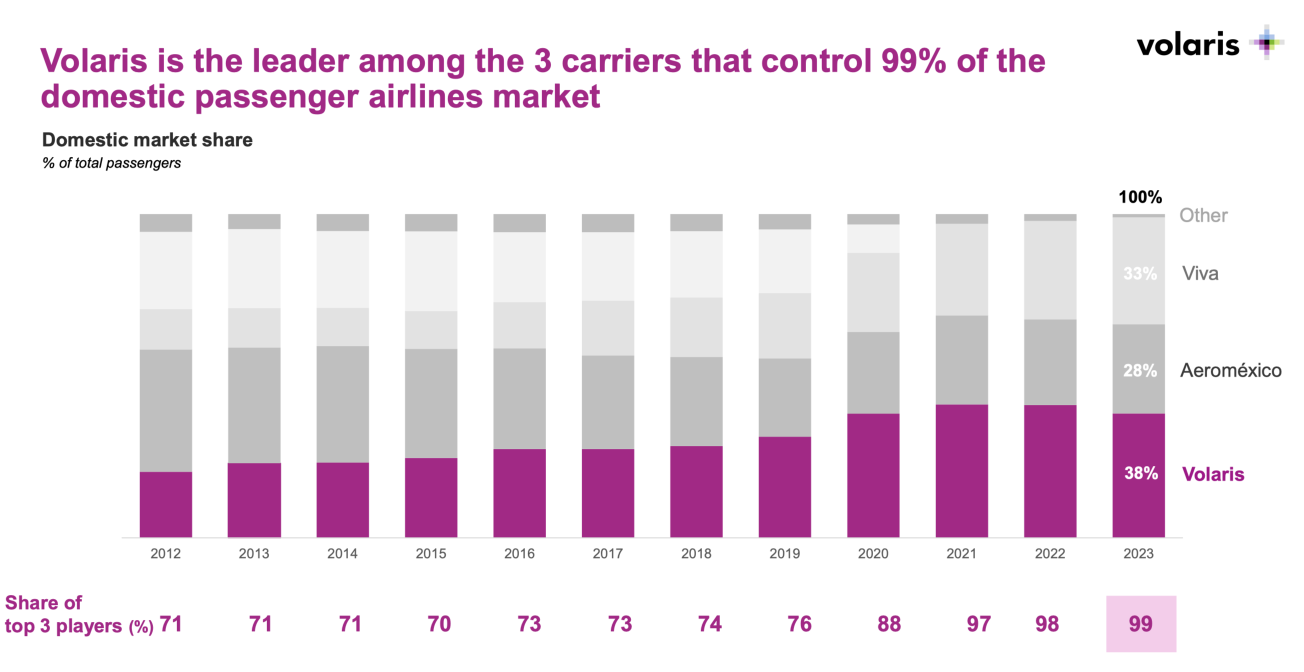

As a result, the Mexican LCC market today is a 3-player oligopoly, with Volaris, Aeromexico and VivaAerobus having 38%, 28% and 33% market share respectively:

One important point to note is that nearly half of VLRS’s routes do not overlap with either of its competitors (Aeromexico or VivaAerobus). I’ve read several sellside reports that mention how 40% - 50% of VLRS’s routes have zero competition except buses — a quick check with your preferred AI client should be able to verify this. Obviously these are likely to be the less profitable routes — but since they also have less competition, I’d wager that they still contribute materially to VLRS’s top-line.

So if their long-term prospects are so positive, why are their valuations today so dreary?

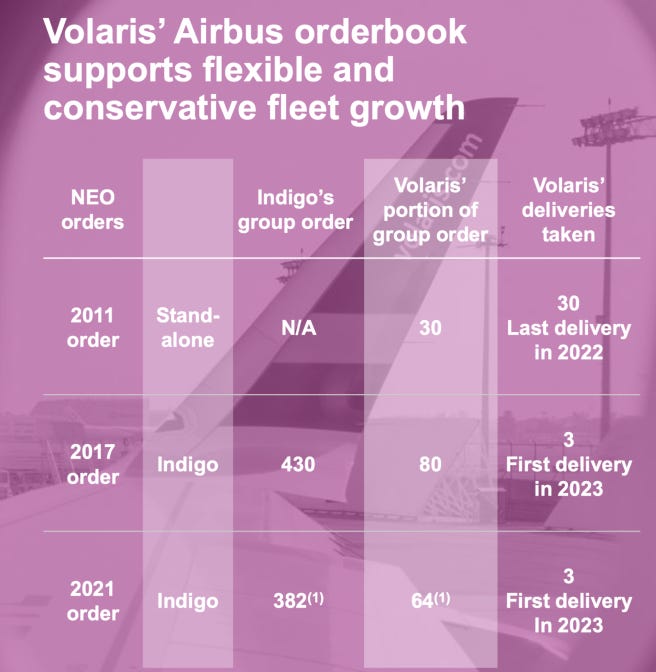

This is largely an idiosyncratic issue — Volaris is currently dealing with a huge capacity crunch owing to some of the Pratt & Whitney engines that it had ordered requiring accelerated inspections1. This isn’t a Volaris-specific issue, with the same recall also affecting AeroMexico, However, Volaris has much higher exposure to it than its peers, as they had been consistently adding new Airbus A320neo planes to their fleet in recent years:

As a result, management expects that it will ground 16-18% of VLRS’s fleet for the rest of year. And given the airline industry’s high operating leverage, this is likely to result in muted FY24 profits.However, the relatively benign impact of this short-term challenge to their long-term valuations makes the recent share price trajectory quite the head-scratcher.

Firstly, this is a short-term concern — it will in all likelihood be solved by the end of the year, and they’ll even receive compensation. VLRS’s CEO is even comfortable enough being candid to analysts that FY24 is likely to be a write-off, which doesn’t sound like someone with something to hide.

Secondly, this development does nothing to blunt any of the immense long-term tailwinds which we’ve discussed above. Furthermore, VLRS is currently in a Net Cash position with respect to borrowings (i.e. ex-leases) — and they’ve demonstrated positive OCF for the entirety of the past decade. At the very least, this implies that they’re not facing any sort of going concern risk.

While VLRS makes headlines for their record-breaking CASMs, the fulcrum of their valuation actually lies in their revenue growth. In this VLRS Part 1 report, we’ll break down and simplify their convoluted revenue model in order to identify the key levers of their revenues — and figure out which levers are the real needle-movers of their future revenue growth.

In next week’s VLRS Part 2 report, we’ll flesh out their fair value by doing a similar deep-dive into their cost structure (i.e. CASM), figure out their future profit trajectory and ROIC, and finally take a stab at determining what their fair value is.

Check out our previous articles:

VLRS Revenue deep-dive

Identifying VLRS's key revenue growth levers

1. Ancillary Revenue Growth is the way

2. Generating Passenger Volumes vs. Higher RASM

3. Doméstica o Internacional?

4. Improving Fleet Utilization - Squeezing more toothpaste out of the same tube

5. What's The Pratt & Whitney Situationship?

6. 📊 VLRS 3-Statement Model (download here)

To illustrate the latent growth in VLRS’s ULCC business, let’s begin by addressing their ULCC industry’s wider TAM growth.

As we saw above, VLRS has plenty of growth runway in the domestic market, simply from converting bus passengers to air travelers. Luckily for the domestic LCC industry, this aforementioned conversion of bus-to-air travelers is pretty much an organic process — as the average discretionary wallet of Mexico’s middle-class grows over time, they will likely gravitate away from buses towards more expensive travel options such as LCCs.

The reason why most potential converts aren’t choosing buses over planes doesn’t appear to be due to a lack of affordability. A quick scuttlebutt of bus fares for long-distance travel between popular locations in Mexico reveals that domestic bus fares are actually more expensive than their equivalent LCC ticket prices:

The bus fare from Mazatlán to Mexico City (1,000km, 15 hours) was USD115; whereas the same flight via Volaris Airlines cost USD111.

The bus fare from Guadalajara to Toluca (500km, 6 hours) was USD89; whereas the same flight via Volaris Airlines cost only USD29.

The actual reason why many Mexicans still prefer taking the bus over flying by air may surprise you. Bus fares typically allow passengers to bring 2-4 pieces of luggage with them, whereas air travelers have to pay additional ancillary fees if they want to bring more than their carry-on with them.

The inference that can be made is that many long-distance Mexican travelers tend to lug large amounts of souvenirs or equivalent back home when they visit family — which might make stomaching the long bus ride home more palatable than ponying up for extra LCC luggage fees.

Nonetheless, this is something that should easily resolve itself over time — as Mexican per capita income rises, it would becomes more acceptable to spend slightly more on ancillary LCC luggage fees for a shorter travel time. A 15-hour bus ride would sound like a nightmare to most Americans today — I don’t see why a Mexican with similar income levels would feel any different in 2035.

Ancillary Revenue Growth is the way

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.