✨ Supermax - the next Hibiscus

"We think no asset is so bad that there's not a price at which it's attractive for purchase, and no asset is so good that it can't be overpriced." - Howard Marks

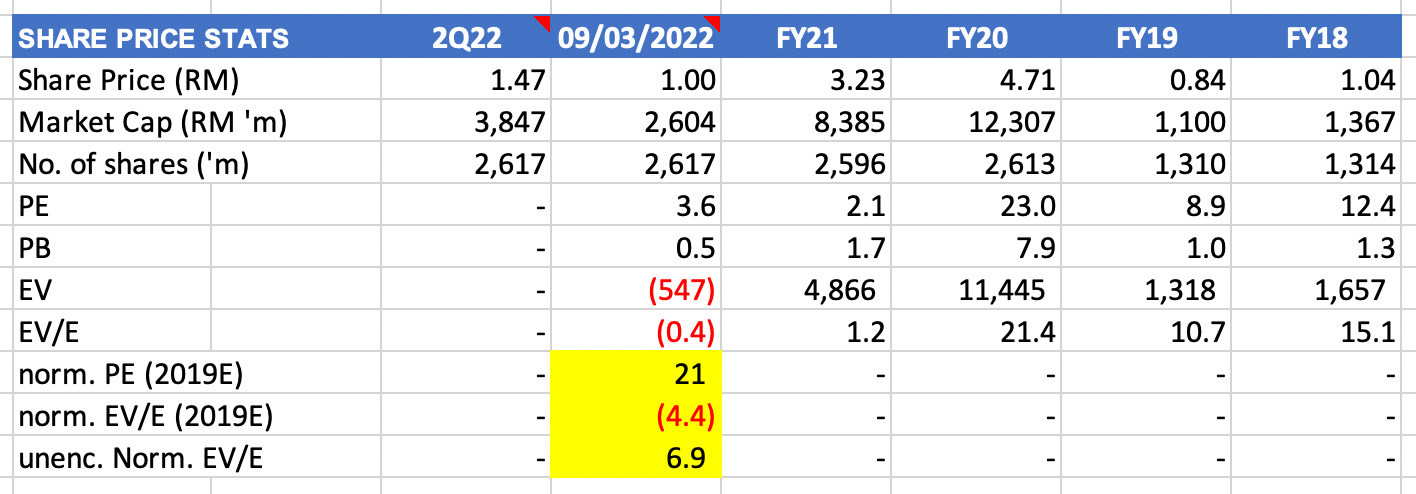

Supermax’s current Net Cash position of

(RM 3.1B)(see edit below) exceeds its entire Market Cap today (RM 2.7B) - after falling by -90% over the past 1.5 years. However, this is not a Net-Net investment thesis!

Edit (14/3/22): A kind reader pointed out to me how Supermax had capital commitments of RM 1.39B (Note 10 of their 2Q22 quarterly report) - which means that their Unencumbered Net Cash position is actually RM 1.76B, not RM 3.1B as previously mentioned. Sincere apologies for this oversight - however due to sheer luck, this new information barely changed the original investment thesis. Please find more details in the edits added in quotes in the middle & end of this article.

Supermax’s management has recently initiated share buybacks at scale - mitigating even the risk of opportunity cost. At the current pace of its recent share buybacks, Supermax could theoretically buyback 50% of all outstanding shares in 12 months!

The investment thesis for Supermax today is similar to my investment thesis for Hibiscus almost 2 years ago - which has seen its share price climb by +300% since then for almost identical reasons. (click the following links to read Hibiscus Part 1, Part 2 and Part 3)

In the 3rd quarter of 2020, as the world was being ravaged by the coronavirus, one stock in particular drew nearly the entire world’s attention. That stock was Top Glove, a Malaysian glove manufacturer which is currently the largest glove manufacturer in the world. In August 2020, Top Glove’s share price rocketed +500% YTD to RM 9.38 at its peak - as glove shortages plagued the healthcare industry, amidst doctors and nurses scrambling to arm themselves with protective wear while caring for COVID-19 patients:

As we all know by now, the first vaccine announcements were made soon after in Nov 2020 - and the entire sector’s share price has been cratering from their highs since then. Top Glove is back to trading at RM 1.90 today, which is a mere +22% up from what it was on the first trading day of 2020. Or put differently, its now down -80% from its 2020 highs.

There are several reasons behind this nosedive, which we shall go into later. However, this stock report isn’t about Top Glove. It’s actually about one of its smaller competitors named Supermax Corporation Berhad (Supermax). Like Top Glove, Supermax is also a glove Original Equipment Manufacturer (OEM) in the global supply chain - which manufactures commoditized gloves for heathcare brands like Kimberly Clark or Proctor & Gamble to slap their brands on. The only real difference between Top Glove and Supermax are their sizes - Top Glove is roughly 3x the size of Supermax in activity and about 5x its market cap.

As glove OEMs are a commoditized business, most of what happened to Top Glove applies almost 1:1 to Supermax as well. We can see from the chart below how Supermax’s share price had an even more meteoric rise and fall - rising +1,500% YTD at its peak in 2020, and having since fallen by -90%. Similarly, its share price today is only +50% from the first trading day of 2020:

However, there is one very big difference between Top Glove and Supermax - the former has a normal-looking balance sheet, while the latter has more Net Cash than its entire Market Cap. Based on its latest quarterly report, Supermax currently has a Net Cash position of RM 3.1B, while it only has a Market Cap of RM 2.7B. This means that if you buy their shares today, you’re basically being paid RM 400M to acquire the business.

Now I know what you’re thinking… is this another Net-Net play where we acquire a piece of a declining business, in the hopes of liquidating its net assets to realize value - and which could potentially end up being a value trap? Let me assure you right now that it’s not. Sure, there will be some elements of a Net-Net in the investment thesis - since you’re quite literally being paid to acquire the business - but there is also a lot more than that here. Let’s explore what those factors might be.

Supermax (7106.KL) Links:

Quick Primer of the Glove OEM Industry

To understand the glove OEM (original equipment manufacturer) industry, we need to travel back in time a little. Back in the day, gloves were typically made from rubber - or its cooler-sounding name, latex. The main competitive advantage that Malaysian glove manufacturers had at the time was their close proximity to raw materials - the small country was the top rubber exporter globally back in 1988, and is today still the 3rd largest rubber producer in the world (after Thailand and Indonesia). The reason for this was because the Malaysian tropical rainforest climate - with its regular rainfall of about 2000–2500 mm per year and average temperature of 26–28°C - made it an ideal haven for planting rubber commercially.

Given the highly commoditized nature of the sector and after decades of industry consolidation, one company emerged as the clear champion of the domestic glove OEM industry - Top Glove, which earned its reputation through producing latex gloves at scale. However, around the early 2010’s, the global healthcare industry started to shift en masse towards favoring nitrile gloves over latex gloves. This was because nitrile gloves - while slightly more expensive - were also more chemical-resistant, more puncture-resistant, and perhaps most importantly were suitable for use with patients with latex allergies.

It was in this backdrop that a new domestic competitor Hartalega burst onto the Malaysian glove OEM scene, and split the high-growth global glove manufacturing industry between Top Glove and itself (they have roughly equal market caps today). Hartalega’s main bread-and-butter was nitrile glove production, and it also managed to leapfrog Top Glove at the time by investing early and heavily into automation. Considering that the competitive bottleneck in most commoditized industries boils down to economies of scale (or branding, which is non-existent in this sector), Hartalega’s ability to cultivate maximum operating leverage through ramping up automation and reducing its reliance on manpower soon allowed it to catch up to Top Glove.

In the meantime, other lesser glove OEM companies like Supermax and Singapore-listed Riverstone were also able to thrive amidst the rapidly growing global healthcare market. As aging demographics in developed markets around the world (e.g. Japan, USA, Europe, and even China now) meant higher hospital admissions in general, this led to a secular increase in forecasted global glove demand over the long-term. Even as far back as 2017, investors recognized this long-term secular uptick in demand and began to price this expectation into the share prices of domestic glove manufacturers.

Then, COVID-19 happened in early-2020. As doctors and nurses around the world scrambled to outfit themselves with Personal Protective Equipment (PPE), the global healthcare sector found itself short on supplies in every imaginable quantity - gloves notwithstanding. The long and short of it was that due to the huge shortfall in supply, glove ASPs skyrocketed by +100% as glove manufacturers found themselves with order backlogs stretching years - with their customers willing to place orders years in advance to get priority in line. Coupled with glove factories running at maximum capacity 24/7 to keep pace with global demand, the double whammy of both increased unit prices and increased order volumes led sector revenues to stratospheric heights (Supermax YoY revenue: +1,000% trough-to-peak between 2020 and 2021).

However, all good things must come to an end, and what goes up must come down. As light slowly began to emerge at the end of the pandemic tunnel in 2H21 (amidst global vaccination rates picking up), global glove demand started to show weakness relative to the huge surge experienced at the beginning of the pandemic.

At the same time, many new entrants to the glove OEM industry also started appearing; while large Chinese competitors like Blue Sail Group and Intco Medical had taken advantage of the scale-up in global demand to ramp-up their operations, and began to pose a credible threat to Malaysian incumbents. The general idea was that since Chinese companies had way more access to capital than Malaysian companies, it was only a matter of time before they would eventually catch up to the Malaysian incumbents via developing superior economies of scale.

Also, remember how the Malaysian glove OEM companies used to have a structural cost advantage owing to their closer proximities to rubber trees? Well, the main raw material in the production of nitrile gloves is a chemical called butadiene - which can be manufactured in a petrochemical lab anywhere around the world. As the global healthcare industry pivoted towards nitrile gloves over latex gloves, this meant that the aforementioned cost advantage formerly held by Malaysian glove OEM companies also became non-existent going forward.

Putting this all together gives you the necessary context to understand how the glove manufacturing sector got to be the way it currently is, and how to assess its future going forward. It also explains why Supermax’s recent share price chart looks like this:

Supermax’s Valuation

Now, at this point I would usually be spouting an illegible string of forecasts regarding all the moving parts of Supermax’s business - in an attempt to accurately identify Supermax’s future prospects and derive a valuation for their shares. Some of these moving parts include:

butadiene spot prices,

future outlook for global glove demand,

incremental global manufacturing capacity from glove OEM competitors,

future ASPs for gloves,

etc.

Get a 30-day trial for FREE to read the rest of this 5,000-word report by clicking this button!

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.