There’s been a flurry of news recently surrounding the enthusiastic purchases of SIRI by Berkshire Hathaway. While many attribute these share purchases to Ted Weschler, I have reason to believe1 that these purchases might actually be at least partially influenced by Buffett.

Why? Because a SIRI investment bears all the hallmarks of an investment in OXY — something which I’ve analyzed extensively before in the article below:

OXY's Outsider CEO, Vicki Hollub & Warren Buffett's Next AAPL

Here's The Real Reason Why Warren Buffett is Enchanted by the High FCF Yield Occidental Petroleum (NYSE:OXY)

In my OXY article above, I explored what Buffett might have seen in SIRI which led to his acquiring of a massive 34% stake in it. While Occidental might be a juggernaut of an O&G firm following its Anadarko acquisition, there are really only a few needle-movers behind its valuation — as I’ve explored in painstaking detail.

The long and short of it is that as far as Buffett is concerned, he gets a pretty fixed x% yield on his OXY common stock investment at a given spot oil price. While Vicki Hollub ultimately decides how much in Berkshire preferreds OXY redeems, Buffett can offset those preferred stock redemptions with common stock purchases to maintain the fixed yield he receives via ordinary dividends.

With OXY’s commitment to return pretty much all of their FCF to common stockholders rather than reinvesting it into the ground (hint hint, Chevron), OXY pretty much represents a fixed yield investment to Buffett at a given spot oil price. And in light of Berkshire’s record $275B in cash & cash equivalents, this is especially attractive when you consider OXY’s capacity to absorb pretty much unlimited amounts of capital.

But how is all this related to SIRI?

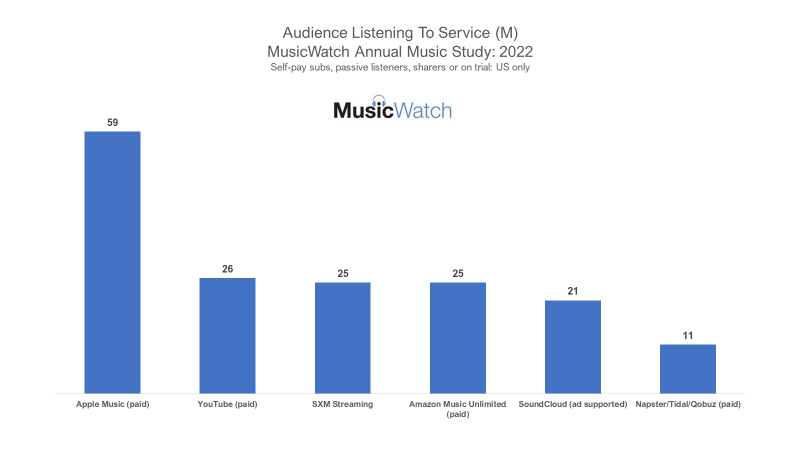

For the uninitiated, SIRI’s common shares are also widely recognized to be somewhat of a fixed yield investment2. They’re the largest satellite radio business in the United States, and it comes pre-packaged with nearly every car sold nationwide. Even in the streaming domain, they pretty much have half the paid subscribers as giants like Spotify and Apple Music:

However, as you can imagine, that also means that their future subscriber growth is rather capped, which is where the notion of SIRI being a fixed yield investment comes from3.

As my extensive analysis into SIRI reveals, its common stock possesses a similar investment yield profile as OXY. Its satellite radio business is also capable of absorbing similarly “infinite” levels of capital, upon which it can generate said yield on. This effectively turns SIRI into an FCF equivalent of OXY, minus the dividends and oil price volatility. To an investor, they’re both pretty much identical from an investment/FCF yield perspective.

In conclusion, I’d wager that the main reason behind Berkshire’s recent outsized purchases of SIRI is because the investment yield of its common shares resembles that of OXY — something that Buffett is also extremely familiar with.

However, as you can imagine, there’s actually a lot more to it beneath the surface — e.g. what yield Buffett is getting out of OXY and SIRI, or how such gigantic businesses can be reduced to a fixed FCF investment profile.

Wanna find out more about either? Check out my OXY and SIRI articles below!

Hey SIRI: Why Does Berkshire Own 25% of SiriusXM? (Part 1)

Did Berkshire increase its SiriusXM stake by 50% in Q1 alone? Also, it's 6% of Baupost's portfolio.

OXY's Outsider CEO, Vicki Hollub & Warren Buffett's Next AAPL

Here's The Real Reason Why Warren Buffett is Enchanted by the High FCF Yield Occidental Petroleum (NYSE:OXY)

Click one the links below for more articles about Value Investing!

Unpopular Opinion: Diversified Portfolio > Concentrated Portfolio

Value Investors = Business Owners. Here's The Irrefutable Proof.

How I Became 100% Convinced that Value Investing Was Superior

Disclaimer: This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the authors. To the best of the authors’ abilities and beliefs, all information contained herein is accurate and reliable. The authors may hold or be short any shares or derivative positions in any company discussed in this document at any time, and may benefit from any change in the valuation of any other companies, securities, or commodities discussed in this document. The content of this document is not intended to constitute individual investment advice, and are merely the personal views of the author which may be subject to change without notice. This is not a recommendation to buy or sell stocks, and readers are advised to consult with their financial advisor before taking any action pertaining to the contents of this document. The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties and other factors, most of which are beyond the authors’ control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.rightly or wrongly

“Old SIRI” stock pays a dividend; however the dividend status of the newly restructured “New SIRI2” stock is still up in the air.

Even if SIRI stops paying dividends in the future, their flattish but stable FCF resembles the interest yield of a fixed income investment.

What do you mean by capacity to absorb pretty much unlimited amounts of capital?