SIRI: Occidental Petroleum of the Media Sector (Part 2)

Coca-Cola is ex-growth too, but its trailing PE is 25x. SIRI's is 9x.

TABLE OF CONTENTS:

1. Why SIRI Is Just Like OXY (to Berkshire)

2. Understanding SIRI: What Moves Their Needle?

Revenue By Segment (SiriusXM/Pandora) + Type (Subscriptions/Ads)

i. Group

ii. SiriusXM

iii. Pandora

iv. Pricing Power

v. Pandemic Immunity (Macro agnostic)

vi. The Growth Opportunity: Podcasting

3. Profit Margins: Business-As-Usual

4. Satellite CAPEX & Post-Merger Debt

5. Optimal Capital Allocation: Can Be Improved Further?

6. Valuation: SIRI & The Growth Opportunity

7. Optionality: The Fulcrum of Asymmetric Risk-Reward

8. 📊 SIRI 3-Statement Model (download here)

In my previous SIRI Part 1 report, I asserted that Berkshire could very well be looking at SiriusXM (SIRI) as a Media version of Occidental Petroleum (OXY). For context, Berkshire currently owns 34% of OXY and 25% of SIRI.

If you’ve read my earlier OXY report, you’ll know that OXY has some very specific traits which made it particularly appealing to Berkshire. After going through SIRI’s historical financial statements, it struck me that it possesses similar risk:reward characteristics to OXY.

SIRI is widely regarded as being “ex-growth” — and with 1/3 of the US population already listening to SiriusXM, it’s easy to see where that idea might come from.

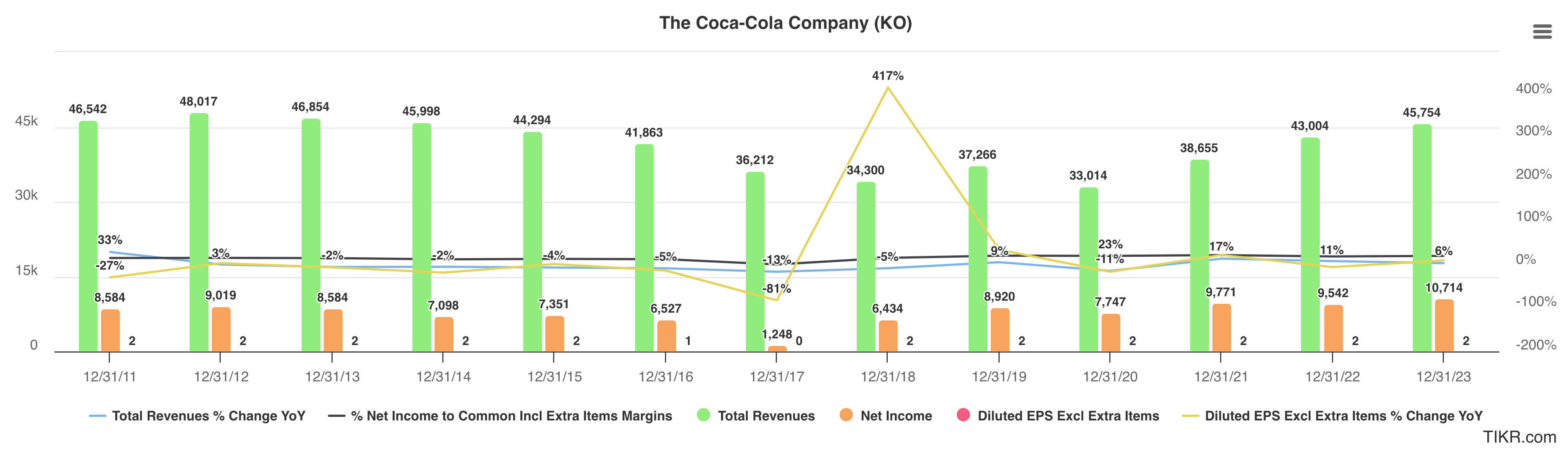

However, SIRI is not alone amongst Berkshire’s portfolio for being “ex-growth”. Another long-term portfolio position which might also fit this description would be Coca-Cola (KO), which Buffett has already held for the better part of the past 35 years. The chart below shows how KO’s revenues and profits haven’t budged since the beginning of the 2010’s, yet Buffett continues to “HODL”:

This means that the shareholder return of KO depends almost entirely on its valuation. Fortunately for Buffett, he acquired KO in 1989 when it was trading at an equivalent to today’s share price of $3 - $4 (current: $60). However, it’s valued at 25x PE today, a huge market premium to Buffett’s initial purchase despite being “ex-growth”.

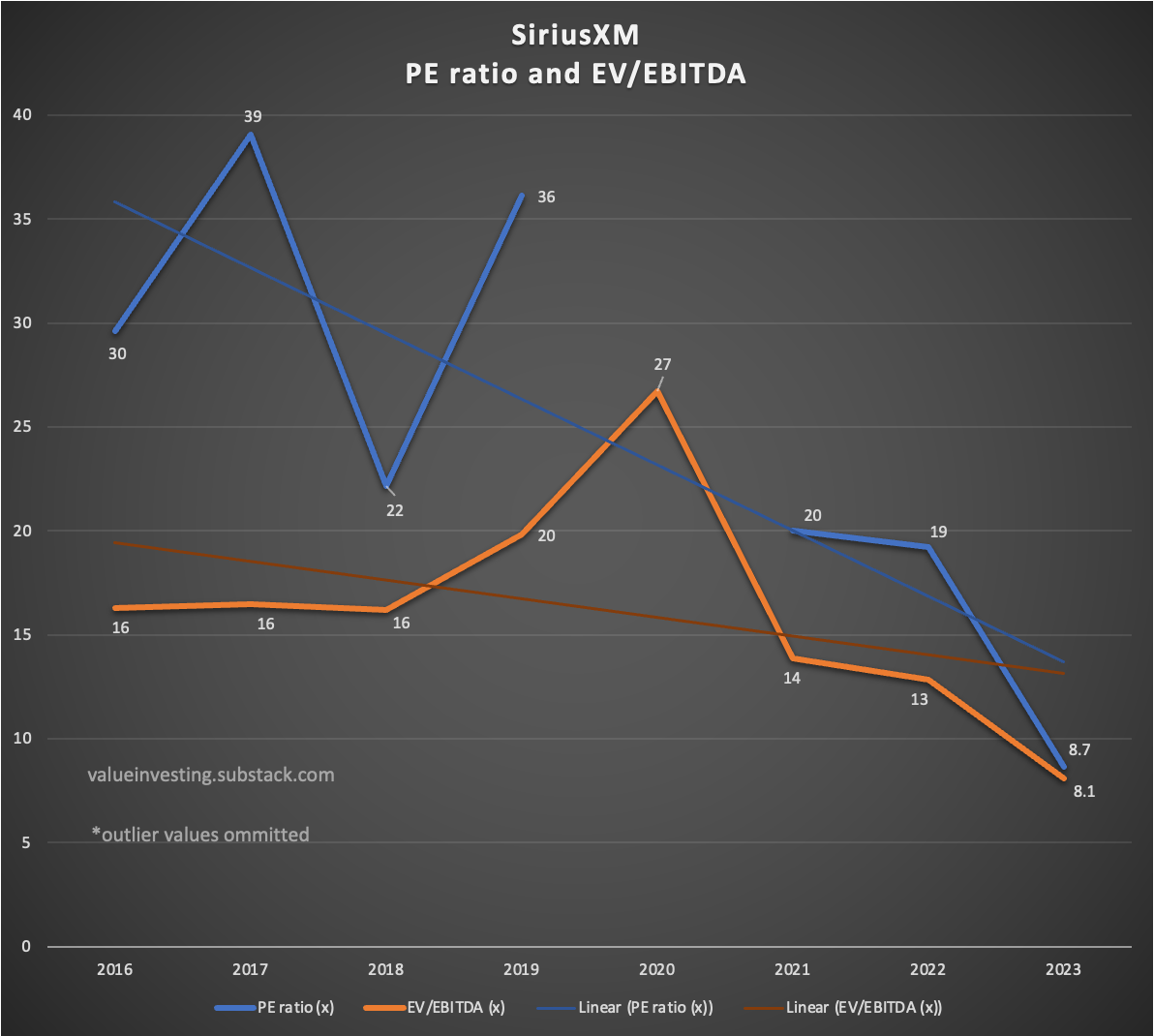

In comparison, SIRI is valued at 9x today — flipping that around implies an earnings yield of 11%. Furthermore, SIRI isn’t exactly zero-growth — as I shall explain below, it’s more like 5%.

Why would KO trade at 25x PE despite being ex-growth? The reality is that KO isn’t the only ex-growth stock which trades at 4% earnings yield — other mature cash cows at such valuations include Nestle (21x), Unilever (19x), Anheuser-Busch (27x), Kraft-Heinz (15x), IBM (19x)… the list goes on.

A quick glance at the chart below would demonstrate the ample opportunity for SIRI’s multiples to recover back to historical levels — their earnings have actually GROWN by the aforementioned 5% CAGR over this period.

So what’s got investors so tickled? SIRI does face some challenges to future growth — nothing that can’t be offset by a single-digit multiple, but challenges nonetheless.

However some of these are overblown, such as the “melting ice cube” narrative built into consensus valuations. As we’ve covered in SIRI Part 1, SiriusXM is likely in a better future growth position than Spotify in the streaming industry.

On a shorter timeframe, there is actually reason to feel slightly optimistic. A chunk of SiriusXM’s subscriptions are packaged free with new cars sales — and with new car sales plummeting amidst the recently hostile interest rate environment, SIRI’s paid promotional subs have declined too. Conversely, this means that should interest rates fall over the long-term, the latter might pick up steam as well.

On top of that, there’s also the recently announced price hike by Spotify. As we shall explore below, both SiriusXM and Pandora have plenty of pricing power.

Furthermore, I’d suggest that when Buffett made his initial purchases of Coca-Cola (KO) in 1988, it was going through a much more challenging time. At the time, KO wasn’t the single product businesses that it is today — it was an overburdened conglomerate with a multitude of failing businesses. I’d even go so far as to say that SIRI today looks better than KO in 1988.

Remember the ironclad rule of Howard Marks (paraphrased) — “Cycles Always Recycle”. What could the valuation of a dominant sector incumbent with pricing power look like once it gets past this cyclical trough?

As I mentioned in Part 1, one doesn’t require a lot of growth to justify a 9x earnings multiple. Just a little growth is enough — so let’s see if there’s at least a little growth in SIRI. That could make all the difference.

Disclaimer: The contents of this document are NOT meant to serve as investment advice. Read our full disclaimers below.In this report: 4,500 words (25 min reading time), 10 charts of SIRI’s historical performance, SIRI three-statement model

Why SIRI Is Just Like OXY (to Berkshire)

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.