Poking Holes in Einhorn's PTON Thesis

Fooling Some of the People All of the Time + Q1 commentary

David Einhorn of Greenlight fame recently discussed his Peloton thesis at the JP Morgan Robin Hood Investors’ Conference. His claim that PTON 0.00%↑ could rise to as much as $31.50 sent tongues wagging on CNBC — given that it currently sits at $8.50/share.

Woe be it for me to challenge the mind of one of value investing’s Greats, but a quick glance at his Peloton thesis reveals several pitfalls in his thesis. I call it a reverse Margin of Safety valuation.

To understand why, let’s start with Peloton’s business and financial models — which aren’t particularly complicated:

It generates 2 types of revenues at a certain Gross Margin:

Equipment revenues at effectively 0% GM,

Subscription revenues at 68% GM with low churn.

The business incurs OPEX, resulting in a flat FY24 adjusted EBITDA (pre-SBC):

Adj. SG&A stands at 44% of sales; Einhorn argues this could be much lower.

Their R&D spend is 2x Adidas’s despite generating 8x less revenues (i.e. 16x); while their stock comp is comparable to Spotify’s despite having 30x less revenues.

Einhorn’s thesis itself is also exceedingly simple:

Einhorn compares PTON’s cost structure and valuation to the peer median, and claims that both could “revert to the mean”.

If it does so, PTON would generate an average EBITDA of $450M, and trade at 9x - 32x EBITDA.

This would result in PTON’s fair value range of $7.50 - $31.50.

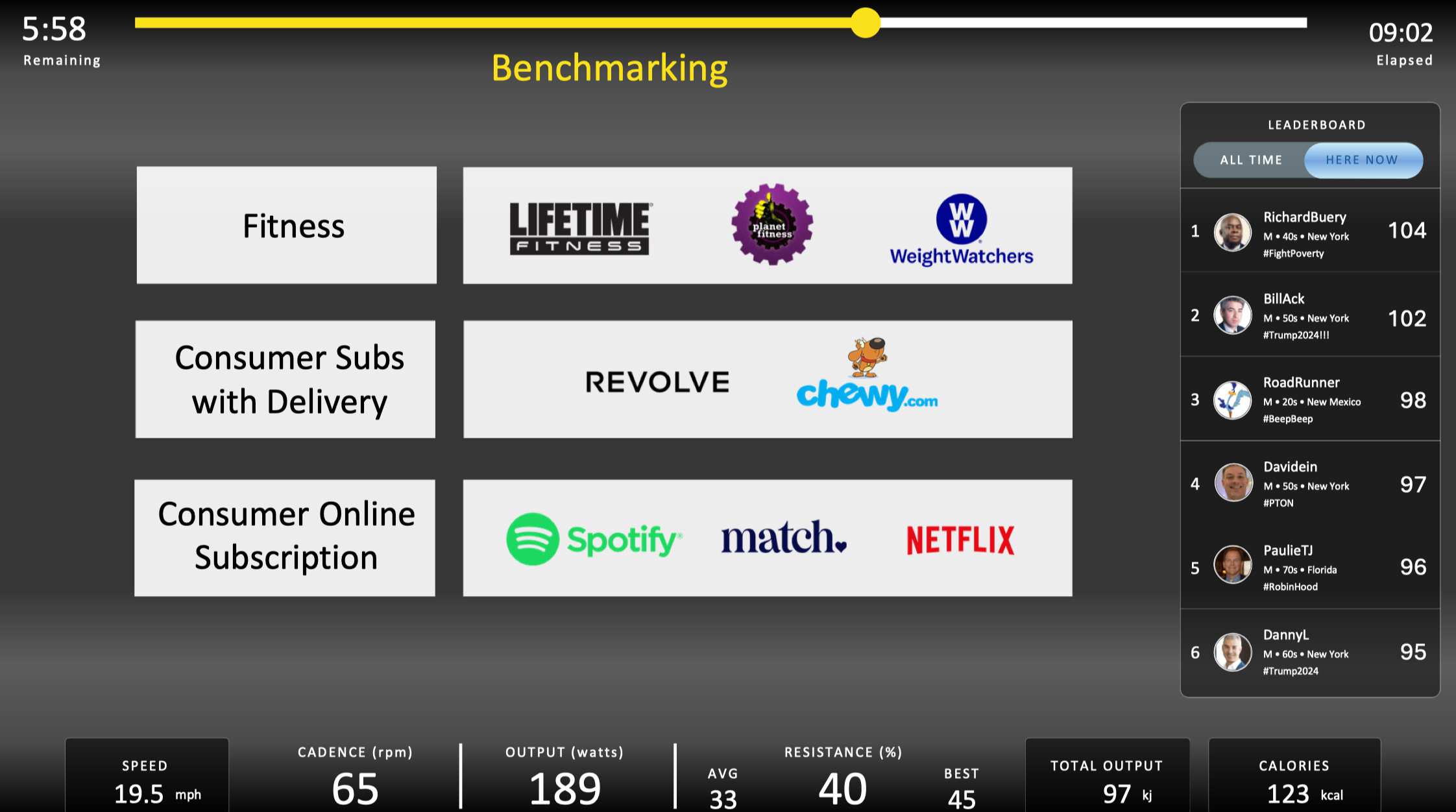

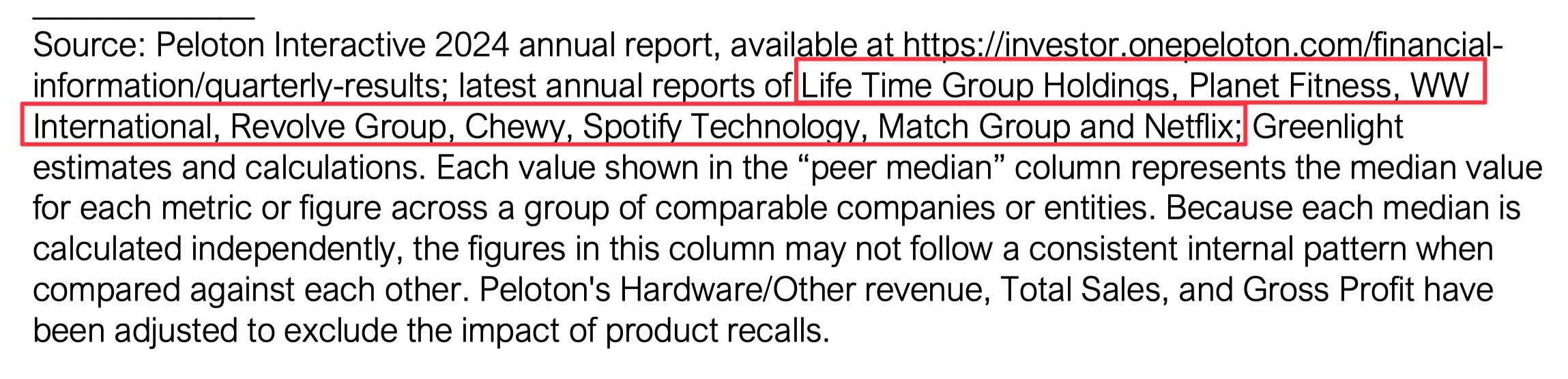

To keep things simple, let’s just stick to the data which Einhorn provides in his slides. The following slide shows the list of companies which he uses to develop his peer median benchmark:

Do you see the problem?

Einhorn is using top-of-the-line industry performers as his benchmark for peer median performance. Specifically, he claims that PTON could one day generate the same adjusted EBITDA margin as the likes of Weight Watchers, Spotify and Netflix.

And lest you think that I’m putting Einhorn’s peer median list of companies in his mouth simply based on one slide, he actually confirms his selected companies in a footnote:

To be fair, we see these kinds of arguments being made by the sellside to fool some people all the time (pun intended). But I don’t think anyone thinks that PTON could realistically improve its cost structure to one day match that of Spotify’s or Netflix’s. Chewy might be considered more of a “target peer”.

Einhorn’s optimism can also be seen in his description of PTON as “a classic razorblade model”, which is not untrue. The real problem is that they don’t earn a sufficient GM to keep the lights on (i.e. OPEX) despite having such a razorblade model. We’ll explore this deeper below.

Testing Einhorn’s EBITDA target

To dive a little deeper, it would seem that most of Einhorn’s optimism for improving PTON’s cost structure mostly lies behind cutting the fat in their R&D and SBC expense. Let’s see how well that holds up, shall we?

Fortunately, Einhorn bases his valuation on EBITDA — which leaves no room for subjectivity in his earnings numerator. To recap, his ideal average EBITDA target is $450M.

In FY24, PTON’s EBITDA amounted to a loss of -$330M. This implies that the aforementioned two cost improvements should result in an EBITDA target of $450M.

Let’s test the feasibility of that, shall we?

FY24 R&D expense was $304M — reducing that by a factor of 16x to match Adidas’s implies adding back $285M of savings to EBITDA1 .

FY24 SBC expense was $311M — reducing that by a factor of 30x to match Spotify’s implies adding back $300M of savings to EBITDA2.

Total savings to EBITDA = $585M, resulting in post-savings EBITDA of $255M3.

Unfortunately, even with these ginormous savings, the resulting EBITDA would still only be half of Einhorn’s target of $450M. Keep in mind this is after slashing Peloton’s R&D budget by 93%, and their SBC expense by 96%. No tech company would have any top employees left after doing that4 — nor would PTON have any cash flow remaining to pay any who stay.

And it still wouldn’t be enough. Not even by half.

I’m aware that this is unlikely to be exactly how Einhorn has modeled PTON’s cost savings — but if we’ve already cut employee costs by 90% and it’s still not enough, what will? The margin of error built into this scenario is already humungous, yet it still remains inadequate.

Et tu, Multiple?

If that weren’t egregious enough, Einhorn is basing his PTON valuation on a 9x - 32x multiple, on top of the aformentioned EBITDA target of $450M.

I have no problem with using peer multiples to justify your valuation. But for the same reasons as earlier, this just ain’t it chief.

To understand why, we need to look a little deeper into PTON’s “revenue quality”.

It’s no surprise that upper-income women cyclists make up >60% of PTON users. Peloton bikes resemble gym class passes rather than weight lifting equipment, with the former appealing better to women over men. And while Peloton does sell other equipment such as treadmills, the vast majority of members still opt for the bike — as evidenced by member interests mostly being cycling and strength training. (see chart below)

A monthly Peloton subscription of $24 - 445 can make a ton of sense when compared to your typical spincycle class, which can cost $24/session on its own. However, you’d also have to cough up nearly $3,000 upfront for the Peloton bike — many customers opt for the $49 - $64 monthly installment plan, which adds up to about $73 - $108 per month in subscriptions + bike installment.

This makes it a much steeper ask than the average gym membership of about $30/month — even before you consider the homemade hack some users are implementing to circumvent buying the expensive bike.

Herein lies PTON’s double-edged sword. While having a niche loyal target demographic is great for customer retention and ARR, it’s not exactly amazing for growth. How many more upper-income women cyclists out there can PTON continue attracting onto its platform? This is not a situation where Peloton bikes appeal to a mass market — it’s much more niche.

While it’s heartening to see Peloton’s member interests diversifying across more categories over time, the reality is that the bulk of its customers still prefer biking-related activities. This is not a social media app or e-commerce platform which you can scale into a general market — if you’re not already a biker or looking to be one, it just isn’t going to be an impulse buy.

The reality is that Peloton isn’t about to disrupt the classic gym membership anytime soon. It only represents good value when compared to boutique fitness classes or bike-related personal trainers. That implies a significantly smaller TAM than the former market.

“Revenue Quality” — Netflix This Ain’t

PTON bulls will point to how Peloton’s content spend via its in-app solution (i.e. using your own equipment) remains dramatically below its media peers, such as Netflix or Apple TV. I think you can immediately spot the flaw in this argument.

Firstly, let us acknowledge that content spend in the media industry is indeed dramatically wasteful. As I’ve discussed extensively in my Disney article, media industry dynamics result in high customer acquisition costs since the commoditized nature of the industry results in low switching costs. By that measure, Peloton’s in-app gym classes experience significantly lower churn, giving it much better unit CAC.

IGER: Post-Cable Malone | Disney Deep-Dive (Part 1)

Narrator: "Bob Iger is the Neo-Cable Cowboy. DIS is TCI All Over Again. Rebundling to Profitability In 2025"

However, I think most people would find it hard to draw a parallel between watching Game of Thrones on HBO vs. signing up for a Peloton gym class. While they can both be technically classified as “media”, the… qualitative nature between the two cannot be any more different. In fact, couch surfers and gym goers are by some accounts represented on opposite ends of the spectrum.

I simply do not think you can expect the same revenue scalability from a Peloton in-app class vs. watching Stranger Things on Netflix while stuffing your face with pizza. This brings into question the “revenue quality” of PTON vs. the chosen peer median.

Q1 Upside Surprise & New CEO

I actually started writing this article prior to yesterday’s Q1 results and the announcement of the new CEO. Let’s explore if there were any material changes.

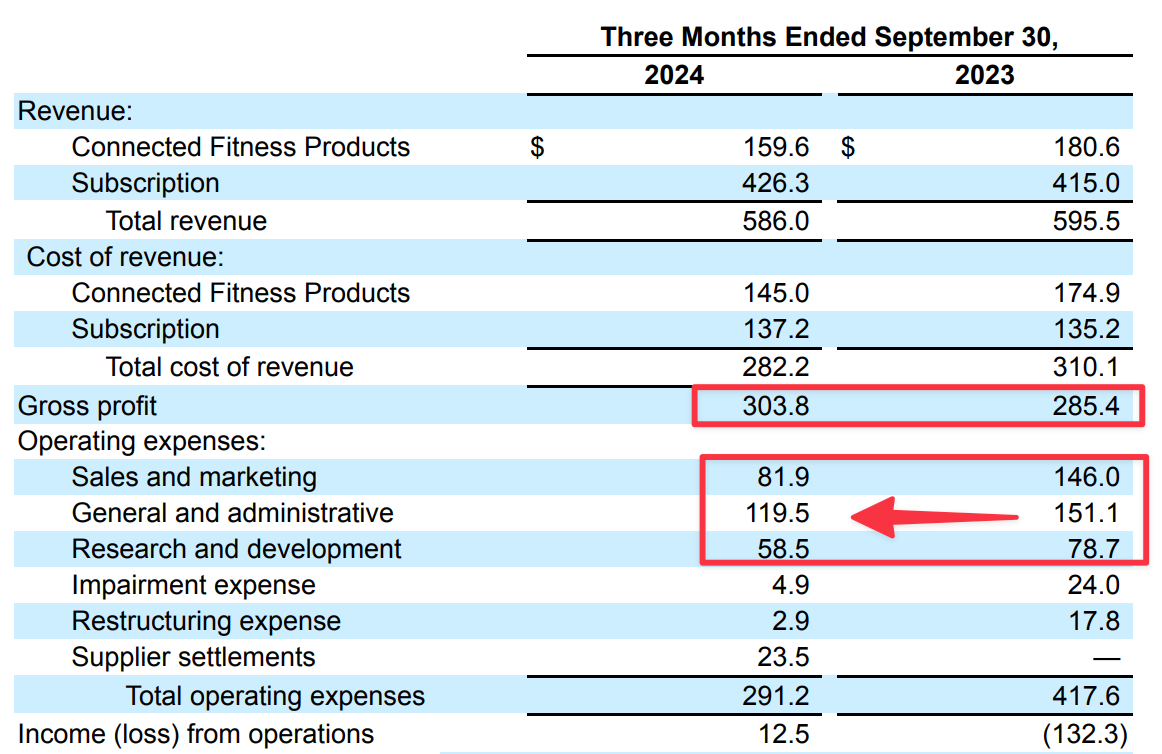

Q1’s surprise breakeven quarter came mostly on the back of a reduction in all 3 major components of SG&A. As we can see below, most of the increase in Operating Income resulted from S&M, G&A and R&D expenses reducing by about 30% in aggregate:

However, it’s worth noting that Gross Profit actually didn’t improve by much YoY. This is noteworthy since, as we saw earlier, cutting OPEX alone isn’t going to cut it if we want to justify Einhorn’s EBITDA target of $450M.

The main highlights from yesterday’s Q1 earnings call include:

FY25 target to deliver run rate cost savings of $200M.

Increasing GM via greater focus on Connected Fitness, International and male members.

New CEO is well-suited for improving LTV/CAC and thus deleveraging the balance sheet.

One issue I have with yesterday’s nearly +30% share price pop is that none of these are actually news. An incremental $200M in run rate cost savings barely moves the needle next to FY24’s total OPEX of $1.7B; and promises made to improve GM remain simply that, promises.

I also don’t want to pour cold water on the announcement of the new CEO yet — but given his background and Einhorn’s penchant for numbers, the cynic in me has to wonder whether the new CEO is about to repeat Dollar General’s mistake of MBA-ifying the business at the expense of common sense.

The missing piece of the puzzle amidst yesterday’s good news is that PTON simply doesn’t have a lot of things going for it which can seriously move its needle. In the absence of material revenue growth, the only other thing that would significantly help in achieving Einhorn’s EBITDA target is a dramatic improvement in Gross Margins. I simply fail to imagine how those can improve substantially, given that subscription GM is already at 68% and equipment GM growth is a dead-end.

Dollar General: 6% NM? No Longer Necessary

At depressed valuations, 6% Net Margin is unnecessary. But what should it be?

Fooling Some of the People All of the Time..?

The sum of all this very much brings Einhorn’s EBITDA projections into question. Even if PTON somehow manages to cut its cost structure to the bone (and risk losing all its employees in the process) in order to achieve his target EBITDA margins, they’d still need to double revenues to hit his $450M EBITDA target. Does it seem likely that PTON’s target demographic of predominantly upper-income female cyclists can help it scale its revenues in such an explosive manner?

More importantly, PTON’s aforementioned “revenue quality” does not appear to be deserving of Einhorn’s carefully crafted peer median EBITDA multiple of 9x - 32x. Admittedly, I can see 9x happening — but by Einhorn’s own admission, that would only result in a fair value of $7.50/share; which is 12% below yesterday’s closing price.

Keep in mind that assumes Einhorn’s target EBITDA margins can be achieved. Maybe I’m just short on imagination, but his plan sounds like the equivalent of performing an L(o)BO(tomy) on a business that has yet to turn a profit.

I would be remiss if I didn’t mention how Einhorn’s use of EBITDA discounts the impact of debt on valuation. PTON has $1.3B of Net Debt, which would result in an Enterprise Value which is 40% higher than their $3.2B market cap. This wouldn’t actually be a problem — if their run rate OCF wasn’t still in the red.

That sorely calls into question the appropriateness of using EBITDA to represent PTON’s normalized earnings, as I’ve demonstrated at length in the following article:

Is EBITDA Really Bullsh*t?

How John Malone Used EBITDA Correctly vs. How Valeant Pharmaceutical Abused It Instead

To be clear, Einhorn does end his presentation by framing PTON’s situation as having “lots of optionality”. Quite frankly, I don’t disagree with his take — PTON is probably as uncorrelated to macro as any stock can be, which has value in a highly uncertain world. However, he also claims that he arrived at his valuation without assuming any growth in subscription revenues, nor any price increases. That doesn’t quite stick the landing for me.

I want to clarify that I haven’t actually done a proper deep-dive into PTON yet, so maybe I’m still missing something. However, based on the data provided in Einhorn’s presentation alone, it certainly seems like a reverse Margin of Safety situation to me.

Click one of the links below for more articles about Value Investing!

Unpopular Opinion: Diversified Portfolio > Concentrated Portfolio

Value Investors = Business Owners. Here's The Irrefutable Proof.

How I Became 100% Convinced that Value Investing Was Superior

Disclaimer: This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the authors. To the best of the authors’ abilities and beliefs, all information contained herein is accurate and reliable. The authors may hold or be short any shares or derivative positions in any company discussed in this document at any time, and may benefit from any change in the valuation of any other companies, securities, or commodities discussed in this document. The content of this document is not intended to constitute individual investment advice, and are merely the personal views of the author which may be subject to change without notice. This is not a recommendation to buy or sell stocks, and readers are advised to consult with their financial advisor before taking any action pertaining to the contents of this document. The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties and other factors, most of which are beyond the authors’ control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.$304M x 15/16 = $285M in savings

$311M x 29/30 = $300M in savings

-$330M + $585M = $255M

keep in mind that most of a Tech company’s R&D expense goes to paying employee salaries, not “actual R&D”.

There’s a budget $13/month membership, but that one doesn’t include “gym classes with other people” privileges.

i dont think you use a proper math funnel though. Instead of just SBC & R&D, you should look at total expense cut (these 2 only to make a point). Now Quarter OP is 40mn, mean a cut of 70mn to achieve 110mn Quarter OP, 70mn out of 260mn OPEX is 30% OPEX cut, not impossible & this is OP not EBITDA.

Of course maybe cant cut tht much without impacting loyalty or growth, but the math is easily workable.

Really interesting analysis and critique of Einhorn's PTON thesis. Your focus on cost cutting measures present a clear picture PTON has a lot more to do to justify the proposed $31.50 share price. But I do believe can increase subscription prices. With multiple subscription offerings across its products and low churn rates (monthly churn ~2%) customers would be willing to pay extra to keep using PTON's products especially due to how expensive the equipment can be the cost of not using a 3000 bike seems a lot more than just paying a $44 dollar subscription maybe even a $60 or $70 subscription.