Is the P/B Ratio Still Relevant in the Modern Day?

What does the P/B ratio really mean? It represents the premium that shareholders are paying to acquire the reinvestment capacity of the equity (i.e. ROE)

In the days of yonder, the term value investing was colloquially used to refer to buying shares of companies that were trading at prices below their balance sheet value. This attribution arose because the father of Value Investing, Benjamin Graham, had a habit of buying stocks that were trading below the value of their Net Tangible Value - or in some extreme cases, those that were trading below the value of their Net Working Capital (i.e. net-net stocks). The idea here was that by buying these stocks, one could liquidate the company and realize an immediate profit in excess of the price paid for their shares.

However, the legitimacy of this value investing narrative has been challenged in recent years - due in no small part to the recent outperformance of stocks who do not necessarily hold large quantums of tangible value on their balance sheets (e.g. Tech stocks). We could go into a long and convoluted debate about whether Tech stocks actually deserved their clout amidst a decade of an ultra-loose monetary policy - but suffice to say, it has stirred a debate in the investing zeitgeist about whether value investing remains relevant as an investment strategy anymore.

I have been exceedingly clear in the past about my views about what value investing actually means - and perhaps more importantly what it doesn’t (link above). To summarize my thoughts in my previous articles, Benjamin Graham did not buy net-net stocks simply because he wanted to realize their liquidation value. He bought them because they provided downside protection by virtue of the margin of safety offered from buying shares below their working capital value - while at the same time providing an adequate investment yield owing to their low share prices relative to underlying intrinsic value. In other words, he invested in them because they represented the philosophy of value - i.e. Value Investing. This is exactly how Buffett approaches value investing by the way - notwithstanding the fact that he buys companies with moats at fair prices:

However, I’ve already told that story before, and you can read my previous articles linked below if you’d like to find out more about the value investing philosophy. What we’ll be discussing today rather is whether the P/B ratio is still relevant in the modern day. Whether deserved or not, the fact remains that over the past decade, the shares of businesses with a higher representation of Intangible Assets on their balance sheets did outperform those of businesses with a higher share of Tangible Assets on their balance sheets. And therefore, the question is justified - Does the P/B ratio remain a relevant valuation metric in the modern day?

My Value Investing Philosophy Primers:

Gathering KPIs and segment data is a time sink for investors.

Stratosphere.io gets you the financial data you need with beautiful out-of-the-box graphs for your research process.

It gives you the ability to gather:

10 years and 10 quarters of financial data, company specific KPIs and segments

Stock idea generation & snapshots

Beautiful data visualizations

Check out their powerful research platform with an easy-to-use interface and enjoy the impressively detailed data set today.

Much Ado About Nothing

When most people think about the P/B ratio’s role in business valuation, they tend to interpret it through the lens of a direct relationship between a company’s share price and book value. This means that they will try and find out if a company’s historical share price is correlated to its book value - in order to determine if the P/B ratio is a useful approach towards performing stock valuation on that stock.

There are many reasons why this can actually be a useful exercise. For many old economy stocks (like those found in the Financial and Manufacturing sectors), a company’s book value still remains a useful proxy for estimating its future profits. This is because these businesses tend to generate profits as a function of their tangible assets - e.g. a bank might generate interest income based on how many loans have been made, while a factory can churn out more widgets to sell if it has made more investments in plant & machinery. The is basically an ROIC model - on a given rate of ROIC, a higher rate of capital investment will yield greater profits.

However, this direct and visible relationship between valuations and tangible assets starts breaking down in other types of businesses. For instance, many Tech businesses like Google or Tesla would consider expenses on hiring top talent or cultivating network effects as a proxy to their “capital investments” - even if current accounting standards have yet to consider such expenses as CAPEX. Even certain old economy businesses like Coca-Cola would consider the majority of their asset value lies in their Intangible Assets such as their Brand Asset - which wouldn’t be recognized on the balance sheet under current accounting standards.

This divergence between book value and profit performance by such companies has led to doubts in the public sphere over the relevance of the P/B ratio as a valuation metric in the modern day - or at least one that is not all-encompassing, to the point of doing more harm than good. This concern actually holds some water when you consider that we already have a much more universal valuation metric - the P/E ratio - which directly measures the relationship between a business’s profits and its share price. Indeed, the P/E ratio does a much better job of drawing an apples-to-apples comparison between the valuation of different companies across various sectors.

However, does this imply that we should completely resign the P/B ratio to the annals of history as a dinosaur of a lost era? Has it truly lost its meaning in the modern-day investor zeitgeist? Does it serve so little residual value, that it would be better to dismantle it and banish it forever into the boulevard of broken dreams?

Ever the contrarian, my personal take is no. In fact, absolutely no. The P/B ratio remains alive and well as a valuation metric in the modern day - and it is my intention today to convince you of its continued significance in the modern day.

The P/B, the ROE & the Earnings Yield (Context)

To understand how the P/B ratio can still be relevant as a valuation metric in the modern day, we first need to clarify what valuation actually means.

When people use use the term valuation in its colloquial sense, what they really mean is pricing. In other words, it is used to ask “how do we estimate what the share price will be within a certain period of time” - more commonly known as the “target price”. This can be in reference to the target price of a particular share within the next 12 months, 2 years, 5 years, etc. As such, the classification of target price is more akin to the disposal price or exit price of an investment after some predetermined point in time (e.g. in the PE industry).

In contrast, valuation refers to a company’s intrinsic value - which has a very different connotation from price. Think about why you might buy a $1.50 hotdog from Costco - the price is $1.50, but most people can agree that it tastes better than a $4 hotdog at the football stadium. Even without providing standardized descriptions for the intricacies of hotdog beef texture and flavor, you can already differentiate between the concepts of price and value. The same goes for stocks - I’ll let the Oracle of Omaha himself finish my sentence:

In Buffett’s quote above, he makes a very clear distinction between these two concepts - price and value. The best way I’ve heard someone explain this difference to me in the context of buying stocks is, “we completely ignore the share price; what we’re concerned about is the value of what we’re buying”. A company’s price refers to what you pay to get its value - with that value being the cumulative net/free cash flows into perpetuity. (which Buffett describes as owner’s earnings, and I personally describe as shareholder’s earnings)

And while these two usually go hand-in-hand as prescribed by the EMH, it is possible for a company’s price and its value to diverge significantly - unlike what the EMH prescribes. When prices and value diverge sufficiently, that’s what we call a margin of safety. Notably, an increase in the divergence (or gap) in prices and value do not only happen when stocks are moving in an upwards trajectory - they can also increase in a downwards trajectory. And vice versa.

However, the point I’m trying to make here is that a company’s value refers to its cumulative net cash flows into perpetuity - not the price at which you acquire that value. And it is in this vein that the P/B ratio finds its relevance as a useful valuation metric - even in the modern day. Don’t worry if you’re not following; you’ll understand what I mean by the end of this article.

Firstly, think about what the P/B ratio means. The numerator ‘P’ obviously refers to the price of the company at any given point in time. With that out of the way, let us focus on the denominator ‘B’ - which refers to the ‘book value’ of a company. ‘Book value’ is just a colloquial way to refer to a company’s Total Equity - or its Net Assets. This is because a company’s Total Equity is simply the net value of its Total Assets and Total Liabilities. Hence, a company’s P/B ratio is simply the multiple of its current share price over (or below) its book value or Total Equity (e.g. P/B = 2.0x).

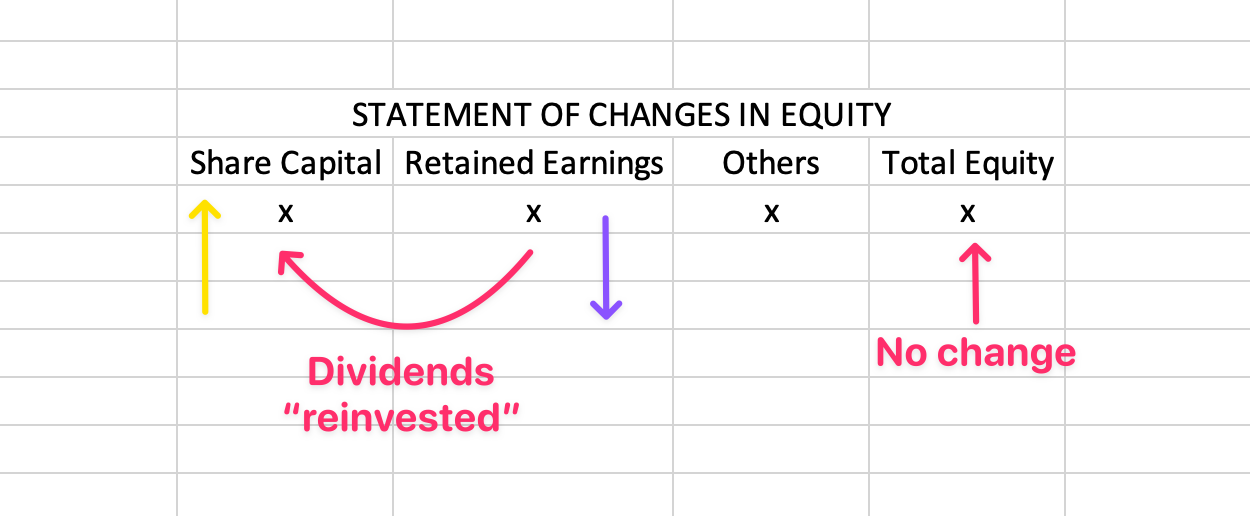

Secondly, we need to understand another tangential performance metric - the ROE. A company’s ROE is simply its Net Profit / Total Equity - and is supposed to reflect shareholder ROI. If you think about the composition of Total Equity, >90% of its value tends to be made up of just two components: Share Capital and Retained Earnings. Sure, there are plenty of other reserve accounts under Total Equity, but in most companies they’re usually quite insignificant compared to these two. Even the occasional outsized Merger Deficit just tends to be used as an offsetting mechanism for Share Capital.

The Share Capital reserve account is quite self-explanatory - it’s the initial investment capital of the business as contributed by shareholders. Retained Earnings, as the name implies, are simply the cumulative Net Profits of the company which haven’t yet been returned to shareholders as dividends. The analogy to draw here is that of a bond investment - an equity investment can be likened to a bond which yields a fixed interest rate annually; but rather than paying out the interest, this “bond” retains the interest coupon and uses it to buy more identical bonds. Hence, the use of the term “retained” - don’t worry if you’re feeling lost, we’ll explore this concept in greater detail later.

As most of you already know, the Net Profits of a company get added to Retained Earnings under Total Equity. Then when a company pays out dividends, those dividend amounts get subtracted from Retained Earnings. This is where the Retained Earnings reserve account gets its name from - they are simply accounting earnings which have been retained in the company, and which haven’t yet been returned to shareholders as cash dividends (i.e. returned earnings). When those accounting earnings have been returned to shareholders as cash dividends, they are then subtracted from Retained Earnings - because those accounting earnings are no longer retained and have been returned as cash. Following so far?

Now let’s take a step further. Imagine a scenario where: i) a company pays out cash dividends to shareholders out of its Retained Earnings. And then ii) those same shareholders immediately reinvest those dividends back into the company - by buying newly issued shares from the company (the share price involved here doesn’t matter, as it involves the same amount of capital). This would result in an increase in the company’s Share Capital by the exact same amount as the decrease in Retained Earnings. From a balance sheet perspective, there would be no change in the company’s Total Equity - the only visible change would be a shift in value from Retained Earnings to Share Capital.

Now let’s compare this with another scenario - where the company simply doesn’t issue dividends to begin with. The aforementioned capital movements wouldn’t happen and would simply remain in Retained Earnings - and Total Equity would remain unchanged. Hence a company that doesn’t pay dividends is equal to one that i) does pay dividends to shareholders, who then ii) reinvests those dividends back into the company. In other words, the amounts in Total Equity simply reflect the total cumulative net investments by shareholders from Day 1 up to the present-day.

This means that the ROE is actually an accurate proxy for shareholder ROI - as it reflects the investment yield of shareholders over the cumulative life of the business. For instance, if a company’s ROE is 12%, that means that the Net Profits of a company is 12% of its Total Equity - or that shareholders had earned a 12% ROI on their cumulative investment in the business that year. Of course, both a company’s Net Profit and Total Equity can fluctuate from year-to-year - so the “true” shareholder ROI would actually be the company’s average long-term ROE - not simply the ROE of any given year.

Thirdly, let us introduce one last formula into the mix - the Earnings Yield. The earnings yield is a company’s Net Profit / Market Cap or EPS / Share price - it is simply the inverse of the PE ratio, and can be used interchangeably. Notice the similarity here with ROE - they both use Net Profit as the numerator, and only differ in the denominator - with ROE using Total Equity while the earnings yield uses Market Cap.

We’ve already established how the ROE reflects shareholder ROI as it divides Net Profit by Total Equity. In comparison, the Earnings Yield is even more straightforward - since it divides Net Profit by Share Price, which immediately reflects shareholder ROI based on current investment prices. In contrast, ROE uses Total Equity as its denominator, which could be derived from outdated historical cost values.

Hence, we can very assuredly say that the Earnings Yield is an accurate representation of shareholder ROI for investors who acquire their shares in public markets. Whereas ROE might be a better indicator for those who acquired their shares at pre-IPO share prices in private markets.

Thus, when estimating a company’s value as an investment (defined as the company’s net cash flows into perpetuity) - we are simply looking for shareholder ROI, with the performance indicators to monitor being the ROE or Earnings Yield. Of course, both of these indicators have to be adjusted for the long-term average Net Profit of the company rather than taken at face value - which does involve subjective estimations of future Net Profits - but in principle, they serve as extremely sound yardsticks for shareholder ROI.

Finally Answering The Question

Now that we’ve established our objective in company valuation, the question remains - how is the P/B ratio relevant as a valuation metric in the modern day?

To quickly recap, we have explored how both the ROE and Earnings Yield accurately reflect shareholder ROI at different investor entry points. The former uses Total Equity as its denominator, and hence better reflects shareholder ROI for investors who bought shares at pre-IPO historical prices; whereas the Earnings Yield uses the current share price as its denominator, and therefore better reflects shareholder ROI for investors who bought shares today at current market prices. However, in principle they are one and the same - they both reflect shareholder ROI.

To repeat, the only difference between ROE and Earnings Yield is that the former’s denominator is Book value while the latter’s is Market cap… do you see where I’m going with this? The P/B ratio is related to them, as it is simply represents Market Cap / Book Value. As such, the difference between a company’s ROE and Earnings Yield is but the P/B ratio - i.e. Earnings Yield x P/B = ROE.

The reason why investors in public markets tend to ignore ROE - even though it makes intuitive sense as a form of ROI - is because public market investors tend to acquire shares at current market prices; and therefore the ROE (which is calculated based on historical cost) feels less relevant as a form of shareholder ROI. However, we have also established above how we can use the Earnings Yield instead of ROE to solve this conundrum - since it’s basically the same thing, except adjusted for market prices. And since the P/B ratio ties the ROE and the Earnings Yield together, it is a great mechanic to gain a sense of “true” shareholder ROI. Allow me to demonstrate how this works with a real-life example below.

I’ve previously written about a glove manufacturing company called Supermax - whose share price has taken a tumble amidst the recovering pandemic environment. From its Aug 2020 peak, its share price has cratered by -93% to-date - prompting investors to run for the hills, and analysts to incorporate the most dastardly outcomes into its valuation. But while everyone else is preoccupied with what future glove ASPs and discount rates to use in their valuation models, the value investor in me has deigned to approach Supermax’s valuation from a different angle.

Let us start with a reasonably conservative assumption - that Supermax’s future long-term earnings can at least match their pre-covid FY19 earnings. This is actually quite a conservative assumption, since the global glove industry is still growing at its pre-pandemic upwards trajectory of 10% CAGR - while the pandemic itself should have provided a permanent secular uplift to the industry’s forward earnings, oversupply situation notwithstanding. But for convenience’s sake, let’s just use Supermax’s FY19e of RM 124M as their steady-state earnings assumption.

If so, then Supermax’s earnings yield based on their current market cap of almost exactly RM 2B is about 6.2% (124/2000). Hence, at this steady-state earnings assumption, Supermax’s shares would be equivalent to a bond with an interest rate of 6.2%.

Now this would be a great investment if your required rate of return was only 6.2%. However, the gold standard for shareholder ROI is closer to 15% - about 2.4x the current investment yield of Supermax’s shares. So the question becomes - how do we get that 6.2% investment yield up to 15%?

Remember how we discussed earlier that Retained Earnings are equivalent to shareholders “reinvesting their dividends” back into the company? These “reinvested dividends” can then be used to buy more assets to grow the underlying business. As a capital-intensive business, Supermax may decide to allocate its “reinvested dividends” towards acquiring more glove machines to upgrade its assembly line - maybe it buys more machines, maybe it switches out old machines for newer more efficient ones. The end result is that it generates more profits (i.e. earnings growth) on higher amounts of capital investment earning the same ROE. This earnings growth should then allow the aforementioned steady-state earnings yield assumption of 6.2% to eventually grow into 15% - since equity instruments are perpetual investments by nature.

Hence, let us now estimate how realistically Supermax can eventually increase it from 6.2% to 15% - by “reinvesting dividends” into incremental capital investments yielding the aforementioned steady-state ROE. Dividing 15% by 6.2%, we would require Net Profits to grow by a minimum of ~2.4x over “perpetuity”. Depending on your definition of “perpetuity”, the required earnings growth would be different - it would be 9.1% CAGR over 10 years, 4.5% CAGR over 20 years, or 3.0% CAGR over 30 years. Hence, in order to grow our shareholder ROI from 6.2% to 15%, we would require a minimum earnings growth of 3.0% - 9.1% CAGR from Supermax going forward. Sounds pretty reasonable, right?

However, this earnings growth of 3.0% - 9.1% is expected to be generated by “reinvesting dividends” into incremental capital investments - which are yielding the steady-state ROE, not the earnings yield. This could be a problem if the company’s earnings yield is significantly lower than the ROE - as is the case most of the time, since the ROE’s denominator of Total Equity tends to reflect historical cost rather than much higher current share prices. As an example, a company like Apple may sport a 160% ROE based on the historical cost of its book value - but its earnings yield based on current share prices would only be 4.3% (i.e 23x PE). This is because you are paying a much higher premium to acquire Apple’s book value (i.e. cumulative net investments) from other investors - since they will also be aware of the superior quality of Apple’s book value, and will be asking a fair price for it.

This is where the P/B ratio comes in handy. Since Earnings Yield x P/B = ROE, the P/B ratio will tell you “how much premium” you are paying to acquire that company’s book value. To use the Apple example above, you are paying a 37x premium over book value (160/4.3) in order to acquire that ROE reinvestment capacity. Even without going into the nitty gritty, that 37x premium (i.e. 37x P/B) alone should give you a sense of whether it is still worth pursuing Apple shares as an investment or not. Simply by glancing at the P/B ratio, we can have a decent clue as to whether the reported ROE represents “true” shareholder ROI.

In Supermax’s case, their P/B ratio is currently a cool 0.4x. However, even if we were to strip away their immense Net Cash balance of RM 2.8B from their book value to account for their equally immense Capital Commitments of RM 3.0B, it would still result in an adjusted P/B ratio of just 0.91x. If we round that up to P/B = 1.0x, we can conservatively say that there is no premium between the ROE and Earnings Yield - and therefore any “reinvested dividends” made at the business level will contribute equally to both old and new shareholders alike.

As we have already determined above, the minimum required earnings growth to bump Supermax’s current earnings yield of 6.2% to our required rate of return of 15% is between 3.0% - 9.1% CAGR (over a 10-30 year investment horizon). A quick glance at Supermax’s current adjusted P/B ratio of 1.0x could also have brought this low bar to your attention - especially in the manufacturing industry, where the P/B ratio isn’t the default valuation metric as in other industries (e.g. the Financial sector). Of course, the P/B ratio by itself doesn’t tell you how attainable that 3.0% - 9.1% required earnings CAGR is - but that’s why we use it in conjunction with other valuation metrics, such as the P/E ratio. Remember, it’s only meant to be a filter.

And who better to lend credibility to this narrative… then Supermax’s management themselves! The company has restarted its share buyback spree after going on a lull - and has been consuming shares from the open market like a starved gypsy over the past month or so. I highlighted this in my recent article - check it out below!

This article isn’t meant to be a detailed analysis of Supermax as an investment - it simply seeks to demonstrate how the P/B ratio still serves a useful function to the investor even in the modern-day. It ties the future reinvestment capacity of the business (i.e. ROE) to the price of admission to the business, and represents the premium that shareholders are paying for the business’s equity reinvestment capacity (i.e. ROE). And since ROE represents shareholder ROI at the business-level, it provides a direct link to the underlying value of the business - which is ultimately what all value investors are investing in.

Of course, that doesn’t mean that you should just rely on the P/B ratio as a valuation heuristic without understanding the context that you are using it for. For instance, something like Apple may have a 160% ROE - but it doesn’t have many remaining opportunities to “reinvest dividends” back into its net assets to generate that sort of yield. It could buy back shares from the open market to exploit that old investment yield capacity - but that would only yield an 4.3% earnings yield, due to the much higher 37x premium or P/B it would have to pay today at current market prices.

However, the P/B ratio still does a marvelous job of acting as a filter - just like its brethren P/E ratio works great when only used as a filter. Therefore, the P/B ratio clearly justifies its existence by representing the premium that shareholders are paying to acquire the reinvestment capacity of the equity (i.e. ROE). It would be heresy to claim that it has lost relevance as a valuation metric in the modern day - far from it, in fact.

This is true even when evaluating capital-light businesses such as those in the Tech sector - since even if what they would normally consider as “capital investments” usually get expensed rather than capitalized (e.g. talent, brand development), their cash costs would ultimately still be reflected in the P&L over the long-term - and therefore would be accounted for by the average long-term ROE.

Long Live the P/B ratio! May its utility never die, now and forevermore.

Check out my latest stock report about Pentamaster HK below - currently trading at just 9x PE!