Was John Maynard Keynes A Value Investor?

Did you know that the Father of Keynesian economics switched from being a Cyclical business cycle forecasting investor to a Long-term "buy and hold" Value investor?

Happy New Year! In the spirit of season’s greetings, I’ve been working on a collaborative article withAndrew Smithfrom theGoatfury WritesSubstack. Together we’ve written about Lord Maynard Keynes, the famed economist whose legacy perpetuates to this day in the form of our contemporary Keynesian countercyclical fiscal policy. Here’s Andrew’s article — head over to show your support to him!

Keynes once famously tried his hand at macro trading, based on his legitimate skillset as a world-renowned economist. As this Financial Times article explains, he quickly got wiped out and proceeded to switch to a long-term “buy and hold” strategy. The relevant quotes in that article can be found below:

The most obvious lesson is that failure is a good teacher. Eighteen months after the Paris adventure, Keynes was speculating in the volatile postwar currency markets. Things went very well indeed for a while, and Keynes turned a profit of £6,000 in a few months — relative to the wages of the time, about £1m today.

He wrote with evident satisfaction to his mother: “Money is a funny thing . . . As the fruit of a little extra knowledge and experience of a special kind, it simply (and undeservedly in any absolute sense) comes rolling in.”

All too easy — and, of course, it wasn’t as easy as it looked. A few months later, Keynes had been wiped out. He managed to borrow more and get back into profitability, but the lesson, learnt in his late thirties, was invaluable. In 1929, when the Wall Street Crash began, Keynes was as blindsided as anybody but far quicker than many to react.

A second lesson emerged as I tried to make sense of Keynes’s strategy: don’t expect consistency. Keynes began with outrageously impulsive adventures in art and currency, switched to cyclical equity investments on the theory that he could forecast the business cycle and, finally, abandoned cyclical forecasting in favour of the kind of long-term value investing made famous by Benjamin Graham and Warren Buffett.

Keynes even used these apparently contradictory tactics simultaneously: the economist Eleonora Sanfilippo notes that during the market crash of 1937, Keynes stuck to a “buy and hold” strategy on behalf of King’s College, Cambridge, whose investment funds he managed, while selling much of his own portfolio in the teeth of the bear market. This may reflect his own financial constraints, or the fact that his personal portfolio had been faster-growing and less diversified and he was keen to lock in the gains.

No wonder it is hard to draw easy conclusions about Keynes’s approach. Wasik provides a list of what he argues are Keynes’s essential investment principles. They include “Don’t move with the crowd” but also “Invest passively”. If that sounds like a contradiction to you, you are not alone.

But then Wasik is inspired by a man who wrote, “My central principle of investment is to go contrary to general opinion,” but also, “It is generally a good rule for an investor, having settled on the class of security he prefers . . . to buy only the best within that category.”

In his 1936 General Theory Keynes wrote that, “Our basis of knowledge for estimating the yield 10 years hence of a railway, a copper mine . . . a building in the City of London amounts to little and sometimes to nothing”, but in 1942 he explained, “I am generally trying to look a long way ahead and am prepared to ignore immediate fluctuations.”

Isn’t it surprising that the man known for inventing the most widely-implemented economic policy in the world (including in US and China today) ended up settling on value investing as the optimal investment strategy? One would have imagined that such a star-studded economist would be the most qualified person alive to excel at divining the macro winds and subsequently become an expert macro trader (“cyclical equity investments (aimed at) forecasting the business cycle”). Yet even he eventually realized that a long-term “buy and hold” strategy prevailed over all others, i.e. value investing.

On the economics front, John Maynard Keynes was the person who first introduced the concept of Keynesian economics — the most widely practiced economic policy today. This was a novel approach to government stimulus during his time — since prior to that, governments tended to apply the concept of Austrian economics, which basically involved a liberal hands-off approach towards government interference in free markets. This resulted in Herbert Hoover, the president during the Great Depression of 1929, basically taking a hands-off approach to government stimulus during the Great Depression. It resulted in America's worst, most depressive recession ever, which lasted until WW2 rolled in where high military spending boosted the US economy and finally lifted it out of its Lost Decade.

In contrast to Austrian economics, Keynes’ concept was novel in that it recommended that governments stimulate or provide stimulus during recessions to smooth out market cycles. The way it worked was like this. During good times, governments would shore up their balance sheets by taxing the strong real economy; and when market cycles inevitably turned, governments could then use their shored-up balance sheet to stimulate the economy in order to reduce economic drawdowns or the severity of the recession. This would provide smoother volatility to market cycles and allow the economy to get back onto its feet faster — at the expense of government spending, which usually involved increasing government debt.

However, once the economy was back on its feet, governments could then recover their budgets more quickly than if they had taken a hands-off approach — by taxing the recovering economy more quickly than otherwise, the tax income of which could be used to pay back any debt it had assumed during the past market cycle. This would reshore its balance sheet in preparation for the next round of stimulus when the next recession rolled in.

In theory, this should end up smoothing market cycles over time, because you have higher lows and lower highs. Ultimately, this should lead to more stability in the real economy, greater business predictability, higher economic efficiency, and also less pain felt during recessions for the common man. In theory, this is a closed-loop system and should work in real-life.

However, this doesn't work as well as intended in practice — due to the existence of the four-year election cycle present in most democratic capitalist economies. What usually happens is that in order to win elections, the government of the day will stimulate the economy whether there is a recession or not. An example of this can be seen in the Trump administration's 2017 tax cuts, which gave big corporations Keynesian stimulus despite there actually not being any recession to speak of.

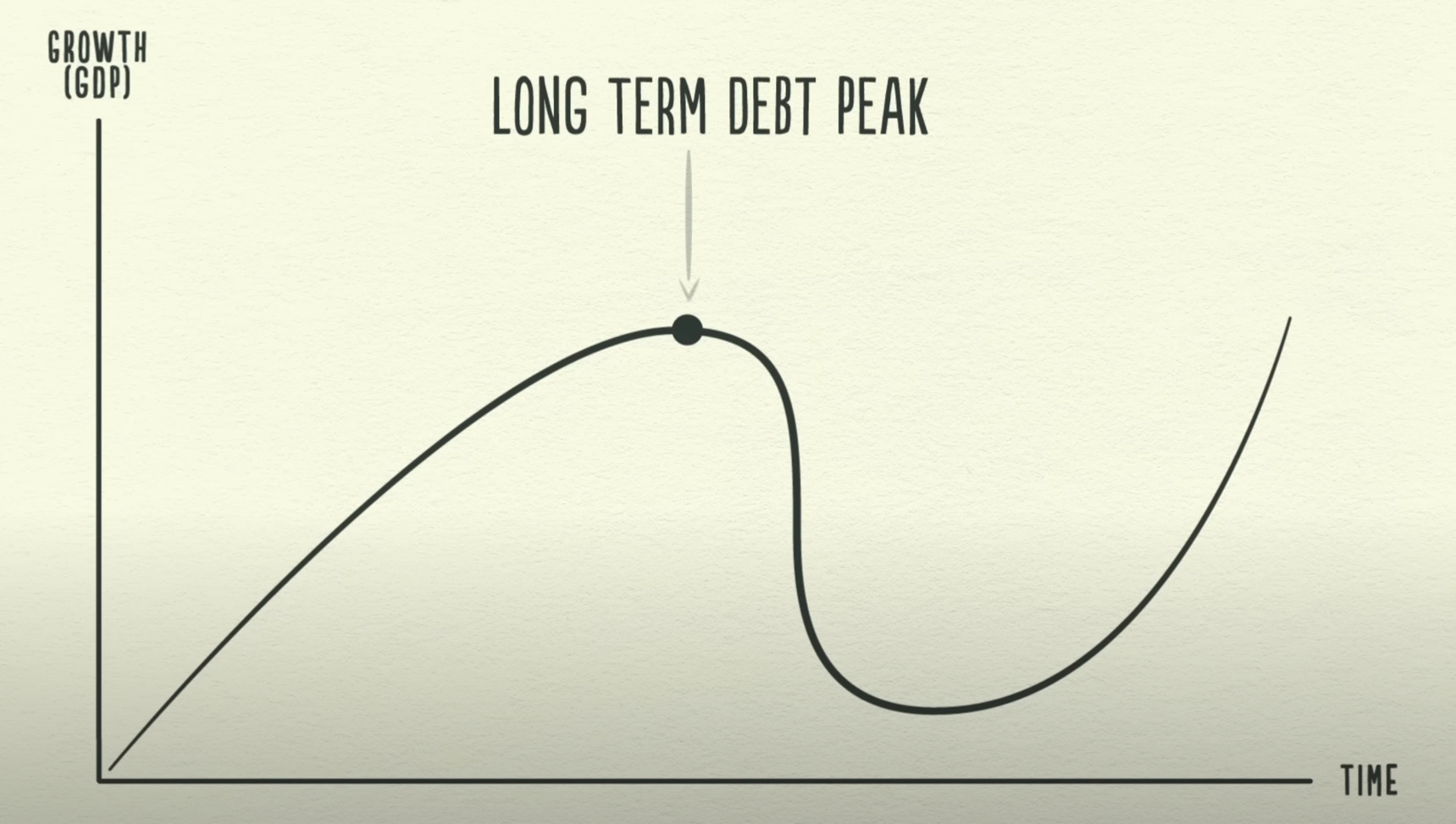

Each time the government stimulates the economy, it does this at the expense of taking on more government debt — presumably with the intention to pay it back later when the economy recovers. However, if governments are politically incentivized to spend in this manner whether or not there is a recession — and never pay back the debt taken on during the past market cycle — then it eventually results in governments taking on an infinite amount of government debt, as the old debt taken during the past recession never gets paid back in full. This results in incrementally higher government debt to GDP over successive market cycles.

As a result of that, what ends up happening is that the government debt gets paid back a little each time the real economy recovers — but never in full over any given market cycle. This eventually creates a huge colossal government credit cycle or government debt cycle. If you keep doing this and zoom things out over 10 market cycles (with each market cycle being 5-8 years), you end up with a gigantic 50-80 year government credit cycle — with such a large amount of government debt that inevitably even the government will not be able to pay back all this debt. Even the US government, which has the luxury of printing its own currency, cannot sustain infinite debt expansion.

And when that inevitable government debt bubble pops, its impact is to cause the real economy to regress back to the starting point of the entire inflated government credit cycle of the past 50 years, as opposed to just the past 5-8 years of the typical market cycle. In theory, the cycle will need to be paid back in full before it can begin recovering — and since the cycle had been delayed for so long, it would need to pay back all the sins of its past debt over the past 50-80 years before it can begin to recover again. That would imply a much longer recession than even the Great Depression of 1929, which could end up spiraling into a perpetual recession, such as Japan's Lost Decades.

In theory, Keynesian economics is definitely an improvement to Austrian economics, as we can clearly observe that market recessions are both smoother as well as shorter after it was introduced, as compared to before. Unfortunately, if all it does is kick the can further down the road, it doesn't solve the actual problem; it just kicks the can down the road.

And that's the problem that we face today with Keynesian economics. It’s actually quite timely to be discussing this now, because the entire developed world happens to currently be at the tail-end of such a government credit cycle — which began around the time that the Fed governor of the early 1980s, Paul Volcker, broke the back of inflation. And it’s been 40 years since then — implying that if a Great Depression of a government credit cycle nature the way I've been describing actually materializes, we could potentially be in for a 40-year recession. Only theoretically, of course.

Having said that, Keynesian economics has worked in real-life before when its prescriptions are strictly followed by governments. An example of this can be seen in the Australian economy, which hasn’t really had a deep recession for most of the past three decades (not counting the global pandemic). When applied correctly, Keynesian economics certainly can be practically implemented — but that’s a whole other can of worms.

Disclaimer: This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the authors. To the best of the authors’ abilities and beliefs, all information contained herein is accurate and reliable. The authors may hold or be short any shares or derivative positions in any company discussed in this document at any time, and may benefit from any change in the valuation of any other companies, securities, or commodities discussed in this document. The content of this document is not intended to constitute individual investment advice, and are merely the personal views of the author which may be subject to change without notice. This is not a recommendation to buy or sell stocks, and readers are advised to consult with their financial advisor before taking any action pertaining to the contents of this document. The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties and other factors, most of which are beyond the authors’ control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.

| A guest post by

|

This came together really well, Aaron! Nicely done. The finished version is sharper than the earlier drafts you shared with me.