Evergrande: A Deep Dive (Part 1)

How the embattled property conglomerate got to where it is today

Evergrande’s woes are not a function of fraud, but overbuilding.

With Inventory Days hovering at around 4 years, they have been pulling forward future revenue growth in an unsustainable manner.

With Payable Days hovering at around 3 years, a portion of payables likely consist of commercial bills and should be treated as debt.

Evergrande isn’t facing a solvency issue so much as it is facing a liquidity issue.

Part 1 sets the context for Evergrande’s current situation.

Part 2 will discuss whether Evergrande will be bailed out, the impact of contagion risk, likely next moves by Chinese policymakers, and how investors should respond.

There has been no shortage of negative press since news of Evergrande broke earlier this month, covering the economic events surrounding the property titan which transpired to lead to this debacle. News headlines have included Evergrande being a Ponzi scheme, riots by its WMP investors outside their headquarters, offers to exchange liabilities for unbuilt properties, and shady accusations of executives redeeming their investments well in advance of the public. While it was fun to follow the news, eventually curiosity got the better of me - and I wanted to get down into the trenches to see whether there was any truth to the headlines.

What you’ll find below is the conclusion of my financial research that unpacks what REALLY went down at Evergrande - all visible from their publicly available financial statements. It’s a story about avarice, malfeasance, hubris, deception and sordid political involvement amongst the highest ranks of the CCP.

Actually I’m just kidding, it’s about none of that. But it does tell you about how Evergrande got to be this way, what its future might look like, and how Chinese policymakers are likely to react.

In Part 2, I will also try to interpret Evergrande’s current circumstances in the context of the wider Chinese economy (e.g. will they get bailed out? how high is contagion risk?), and suggest some proposals about the likely path that Chinese policymakers might take with regards to this default. I will also go beyond the scope of just Evergrande to try and paint a picture of what the Standing Committee and the PBOC might be visualizing concerning the Chinese economy today, and make a guess about what their motivations and likely next steps might be.

Also, a huge thank you to my friends Daniel, Kaung and Shih Chao for helping me with this project. Your assistance has been immeasurable in the writing of this report, and for that I extend my gratitude.

Is Evergrande a Ponzi scheme?

There are many theories floating around about Evergrande, but the one that has been getting the most attention among investing circles so far is that Evergrande was running a quasi-Ponzi scheme of sorts. The way this would have worked would have gone something like this:

Evergrande starts by borrowing a certain sum to build the first house.

Before that house has been completely built, it would sell the house to a home buyer (i.e. pre-sale).

Using the cash inflow from that pre-sale as collateral, it would turn around and borrow more money. (even before the first house is completed)

This newly borrowed money would then be used to build a second house.

Rinse and repeat.

Very quickly, you can see where the problem lies. If the new money earned from the pre-sale of the first house is used to build the second house… where will the money to repay the borrowing for the first house come from? Obviously this model is an oversimplification - but it illustrates how without perpetual growth, the entire house of cards collapses on itself, i.e. a Ponzi scheme.

In search of answers, my friends and I worked on a financial model of Evergrande dating back to 2008 - the earliest available annual report on their IR website. Here’s the 30,000 feet view:

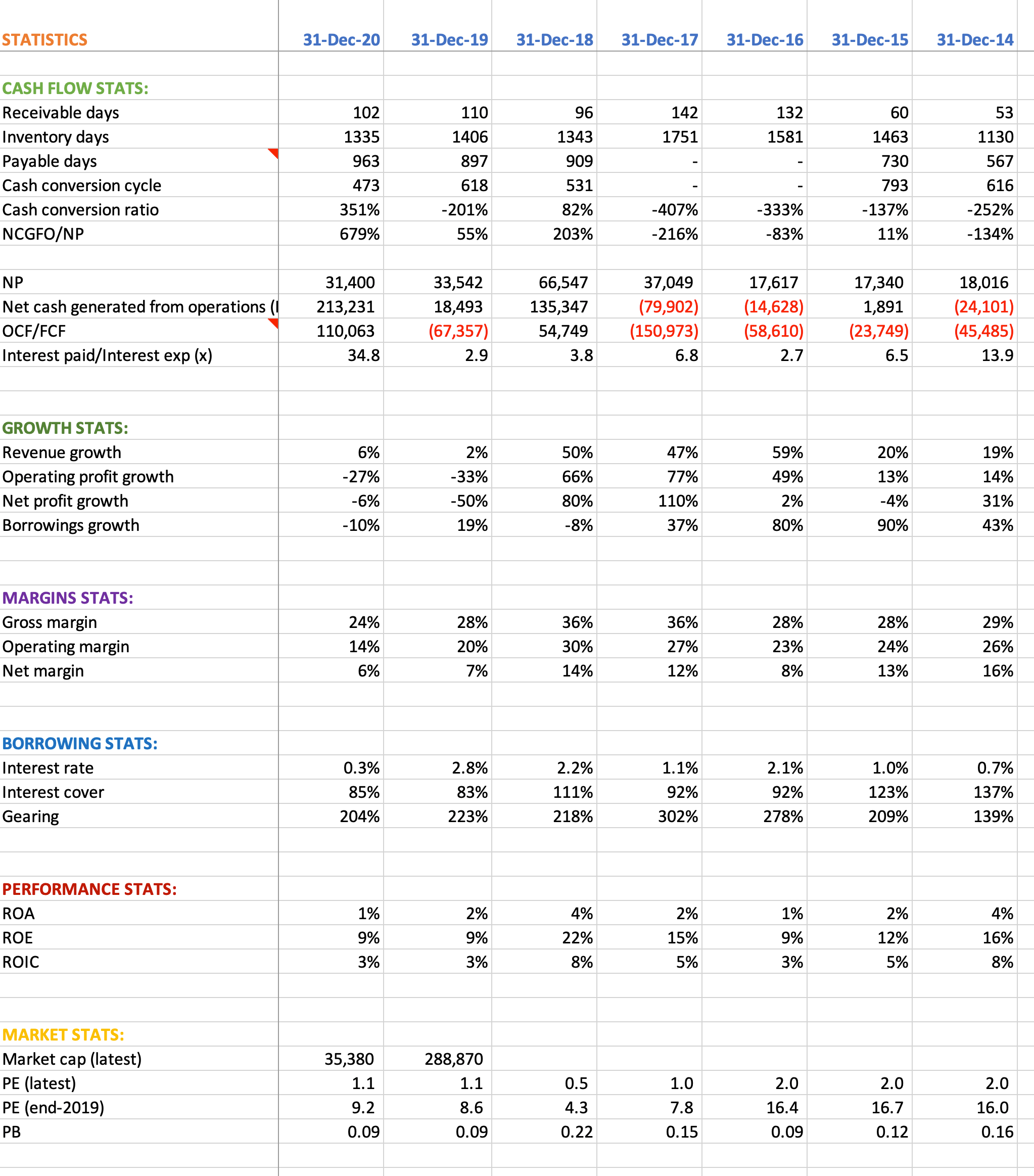

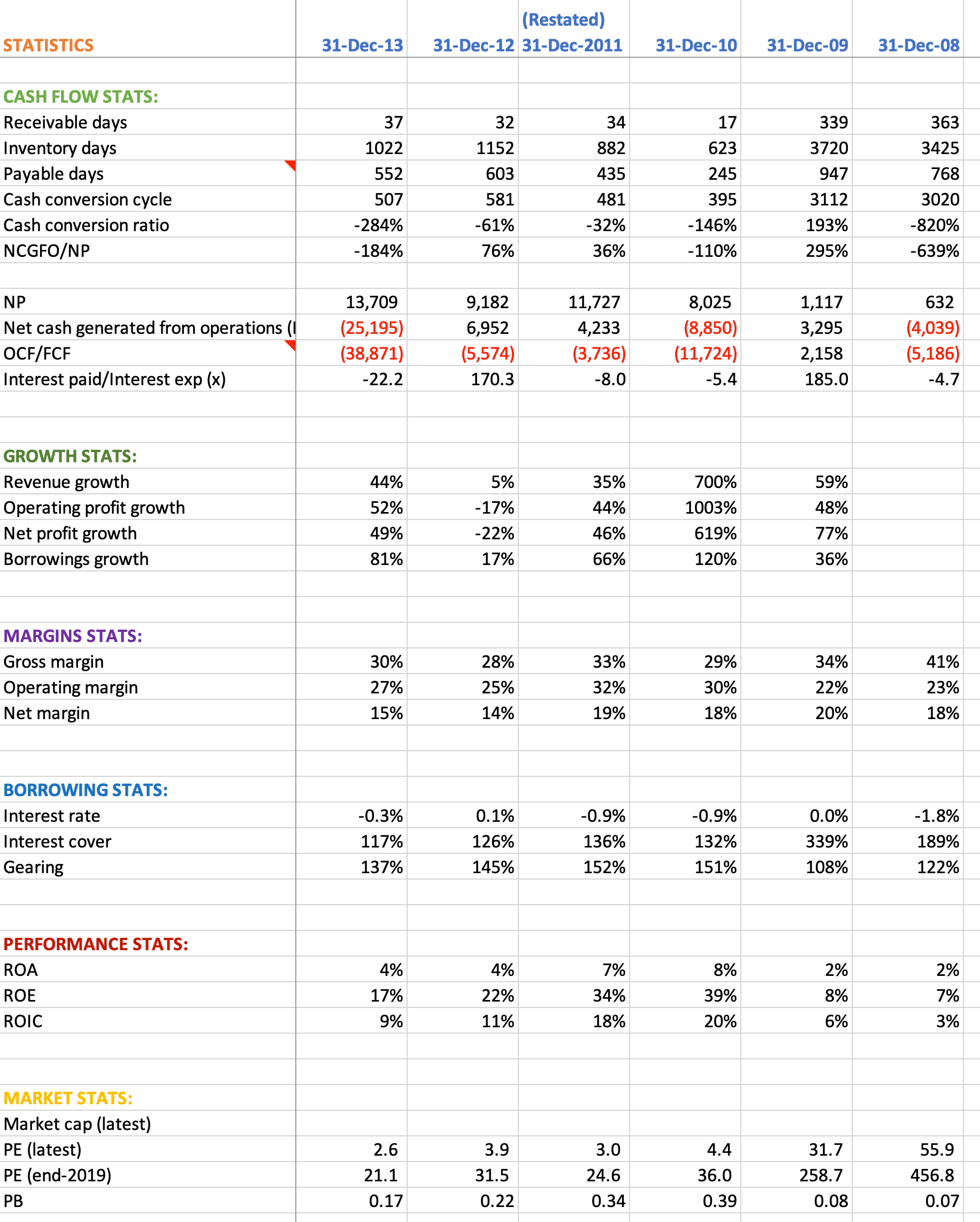

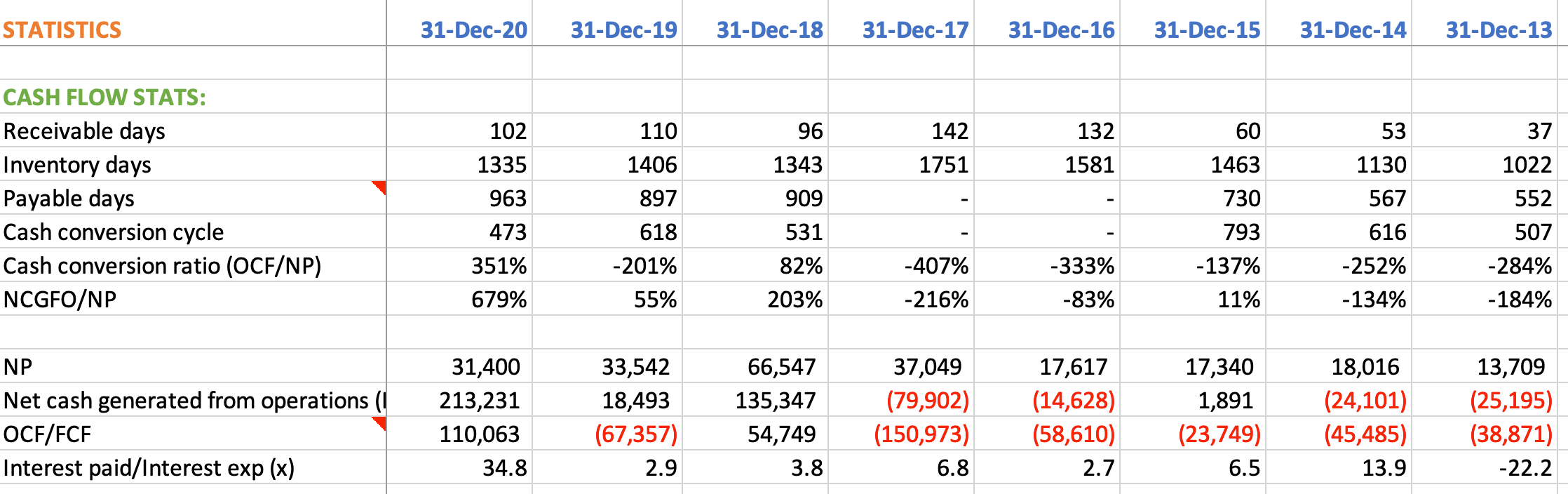

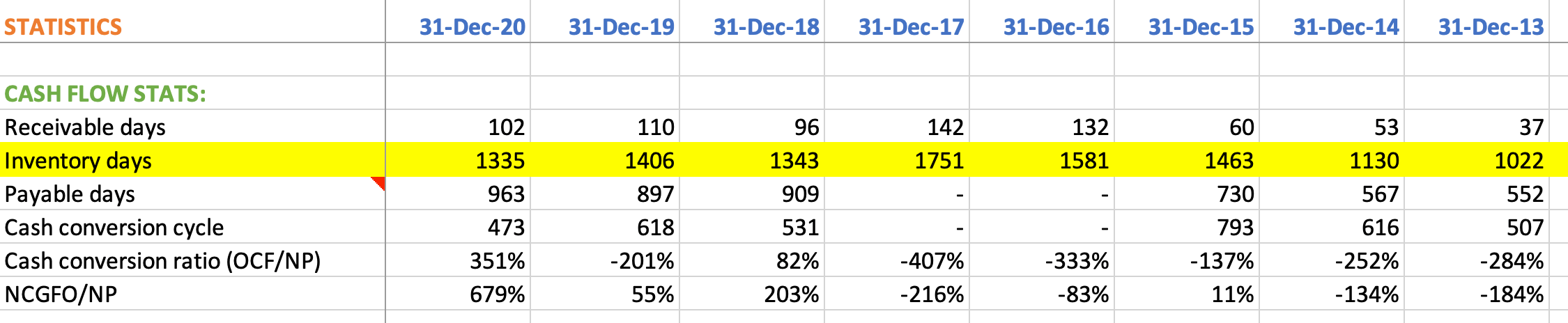

So right off the bat, we can see that their cash flow statistics are terrible. Receivable days are actually okay, likely because they engage in pre-sales of homes. But Inventory days are eye-peeling, regularly hovering around the 4-year mark for the past five years. Likewise, Payable days have been consistently between 2-3 years.

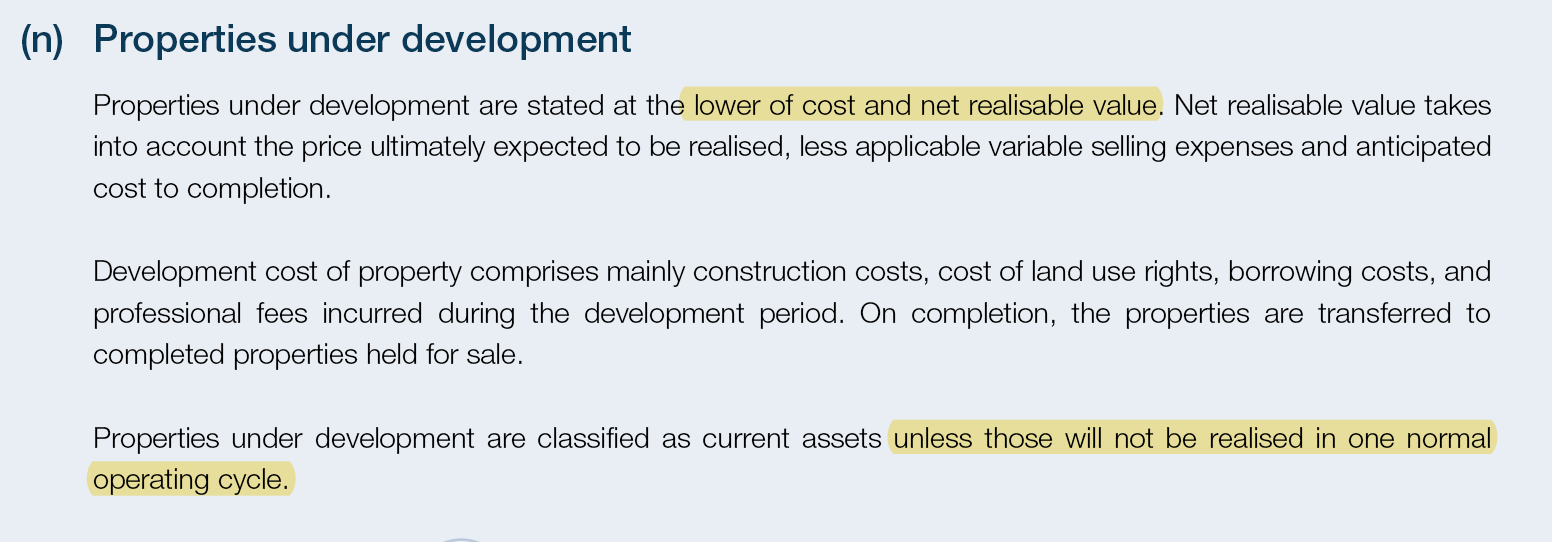

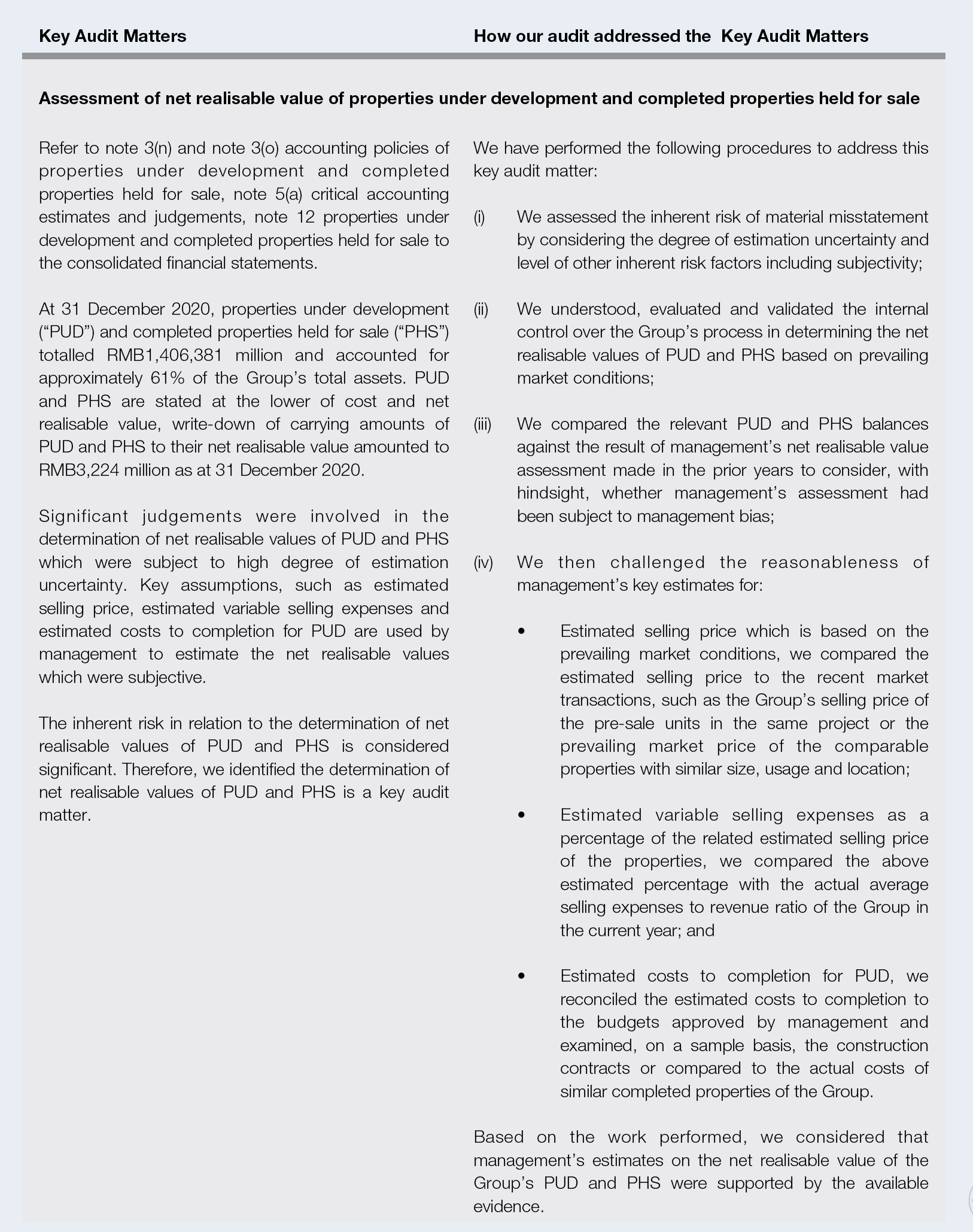

Inventory days are easily addressed - these are likely the infamous unsold properties that Evergrande has since become infamous for in the news. This include Inventories, Properties under development, and Completed properties held for sale. As seen below, it is the Properties under development (PUD) that is causing the build-up of Inventory Days - which lends credibility to the assertion that they are severely overbuilding empty homes.

Since these PUDs are recognized at the lower of cost and net realizable value - and that unbuilt properties likely don’t have much excess net realizable value to costs - these accounts reflect actual building costs incurred. I’m not entirely sure what a “normal operating cycle” consists of, but at least we can be reasonably sure these aren’t just piles of steel rotting away in a junkyard somewhere.

Next up is Payable Days. Evergrande’s payables are such a topic of interest, I thought they deserved their own section.

Payable Days

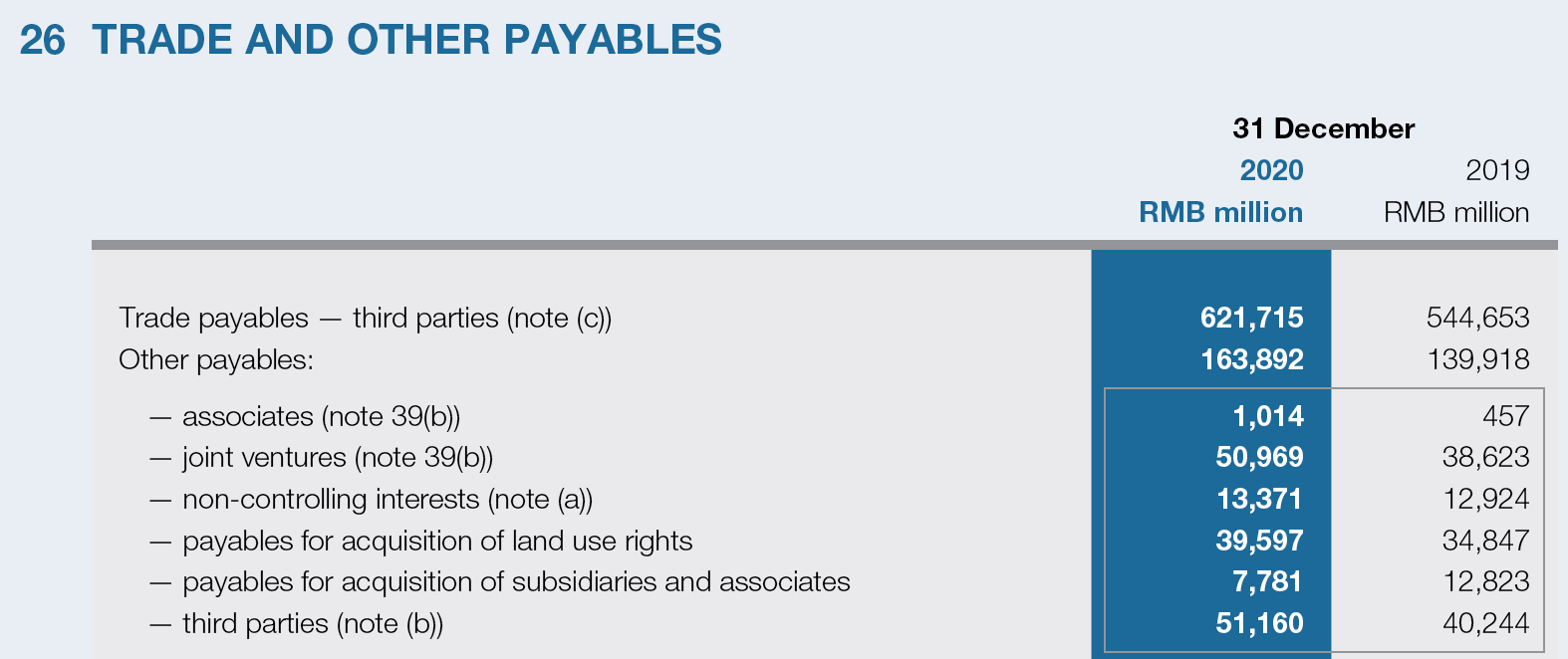

Evergrande’s payables are likely inflated because they consist of commercial bills to suppliers - this Bloomberg article explains the phenomenon well. Basically what happens is that instead of paying suppliers for their services, Evergrande extends to them a commercial bill and tops it up with some sweeteners - perhaps by offering to compound the loan balance at a higher interest rate. Evergrande’s commercial bills are tradable in the market, which means that it’s easy for the supplier to liquidate them. Hence, they are in actual fact borrowings even though they are not presented as borrowings - as stated in the above article. In fact, payables have become so important as funding options to the Chinese real estate sector that regulators have begun asking suppliers to disclose the nature of their commercial bill holdings.

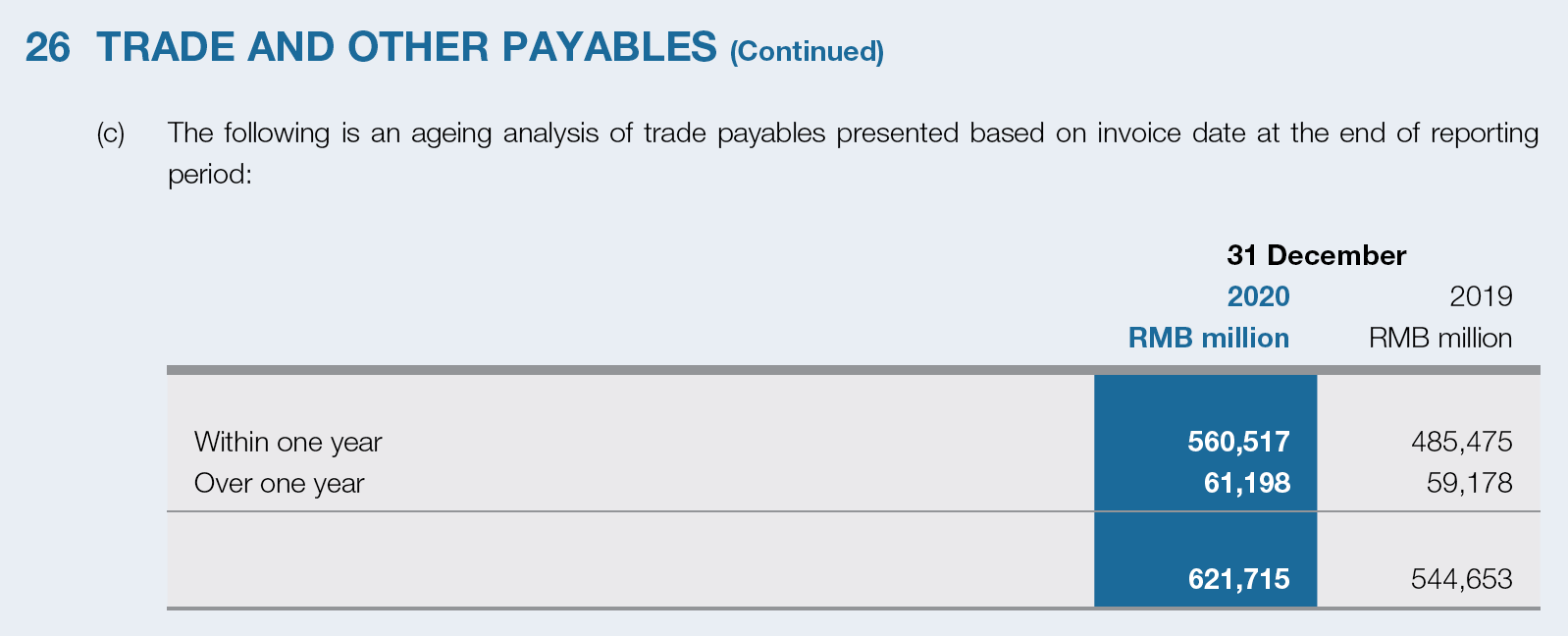

However, trying to confirm this suspicion is an exercise in futility, as the available disclosures only show an ageing analysis of Trade Payables to “third parties”. Oh well. I did find something even more fun though:

So apparently, cash advances from non-controlling interests amounted to a chasm-inducing RMB 2,640 million. These off-balance sheet liabilities are very reminiscent of Ant Financial’s off-balance sheet liabilities under the heading Unconsolidated Structured Entities, which I discussed in a separate article here (paid):

Also, you probably don’t need me to tell you that a 15% annualized interest rate is enough to cause heartburn. Even Ant Financial’s micro-loan borrowers - who were basically subprime borrowers taking unsecured short-term loans to buy iPhones on Single’s Day - were charged approximately 12% annualized interest. To be charged 15% interest by your non-controlling interests tells me that there was some strong-arming of credit terms going on due to unfavorable borrowing conditions - these could be explained by WMP investments made to retail investors by said non-controlling interests, or internal fund-raising campaigns made to executives like the “Chaoshoubao” (loosely translated “ultra-high yield treasure”) crowdfunding product:

One crowdfunding product issued to executives was called “Chaoshoubao,” which means “super return treasure.” In 2017, Evergrande tried to obtain project financing from state-owned China Citic Bank in Shenzhen, which required personal investment from Evergrande’s executives. The company then issued Chaoshoubao to employees, promising 25% annual interest and redemption of principal and interest within two years. The minimum investment was 3 million yuan. China Citic Bank eventually agreed to provide 40 billion yuan of acquisition funds to Evergrande.

If you’re wondering whether these employees became myopic to the risks involved in these investment products due to greed, you’d be mistaken. The report goes on to imply that employees were pressured to participate in these campaigns by their superiors. Anyone who’s ever worked at a toxic workplace will understand what I’m talking about - if you didn’t participate, you’d likely end up becoming the unloved middle child of your department.

Another alternative explanation can be summed up in the following quote from the same article. It captures the supplier dynamics involved so vividly that I’m just going to lift the relevant section straight from the article:

In addition to the 571.7 billion yuan of interest-bearing debt on its books, it is no secret that developers like Evergrande have huge off-balance sheet debt. But the amount at Evergrande is not known.

In the early stage of projects, developers need to invest a lot of money, which can significantly increase debt on the balance sheet. Companies often place these debts off their balance sheet through a variety of means. After presale of the project, or even after cash flow turns positive, these debts would be consolidated into the balance sheet in the form of equity transfer, according to a property industry insider.

For example, 40 billion yuan of acquisition funds Evergrande obtained from China Citic Bank were invested in multiple projects. Among them, 10.7 billion yuan was used by Shenzhen Liangyang Industrial to acquire Shenzhen Duoji Investment. As Evergrande doesn't have an equity relationship with the two companies, this item was not required to be consolidated into Evergrande's financial statement. Evergrande used leveraged funds to acquire equities in 10 projects, and none of them were included in its financial statement, the prospectus of its chaoshoubao shows.

Evergrande has sold equity in subsidiaries to strategic investors and promised to buy back the stakes if certain milestones cannot be reached. Such equity sales are also a form of borrowing. In March, Evergrande sold a stake in its online home and car sales platform Fangchebao for HK$16.4 billion ($2.1 billion) in advance of a planned U.S. share sale by the unit. If the online sales unit does not complete an initial public offering on Nasdaq or any other stock exchange within 12 months after the completion of the stake sale, the unit is required to repurchase the shares at a 15% premium.

Evergrande's hidden debts also include unpaid payments to acquire equities. Dozens of small property companies have sued Evergrande demanding cancellation of their equity sales agreements with the company because Evergrande failed to pay them. They are Evergrande's partners in local development projects. Evergrande usually paid them 30% down for equities but declined to pay the rest even after the project was completed, according to the lawsuits. A plaintiff's lawyer told Caixin that Evergrande's project subsidiaries do not want to hurt local partners, but they have no money to pay as sales from the projects have been transferred to the parent company.

I’m understand why so many people are drawing comparisons between Evergrande and Lehman, but this sounds a lot more like what Enron was doing. The way this could have possibly worked in the context of payables to non-controlling interests is like this:

Evergrande would promise to support a joint-venture (JV) development project that was de jure held on the supplier’s balance sheet, but was de facto worked on by Evergrande. The supplier would then fund the CAPEX of the JV, with Evergrande investing just a small stake in it - those CAPEX would then be represented by a “cash advance” made by the supplier to Evergrande. Once the project was completed, the JV would be acquired in full by Evergrande, hence consolidating the development project onto Evergrande’s books and paying the supplier in full for the trouble.

Obviously this is all tinfoil theory so take it with a pinch of salt, but if true it would explain why there are RMB 2.6B worth of “cash advances” made to non-controlling interests (of all parties) at 15% interest rates. It might also imply the existence of many more off-balance sheet unbuilt properties in existence.

And it might also explain how these kind of eye-popping cash collection figures of RMB 653.16 billion are achieved - when not only is there nowhere near that amount of cash on the balance sheet, but their OCF has been consistently negative over time (i.e. both cash collections and CAPEX netted off at the same time in one lump sum, when these development projects are “acquired”):

Which brings us to the next topic…

Operating Cash Flow (OCF)/Free Cash Flow (FCF)

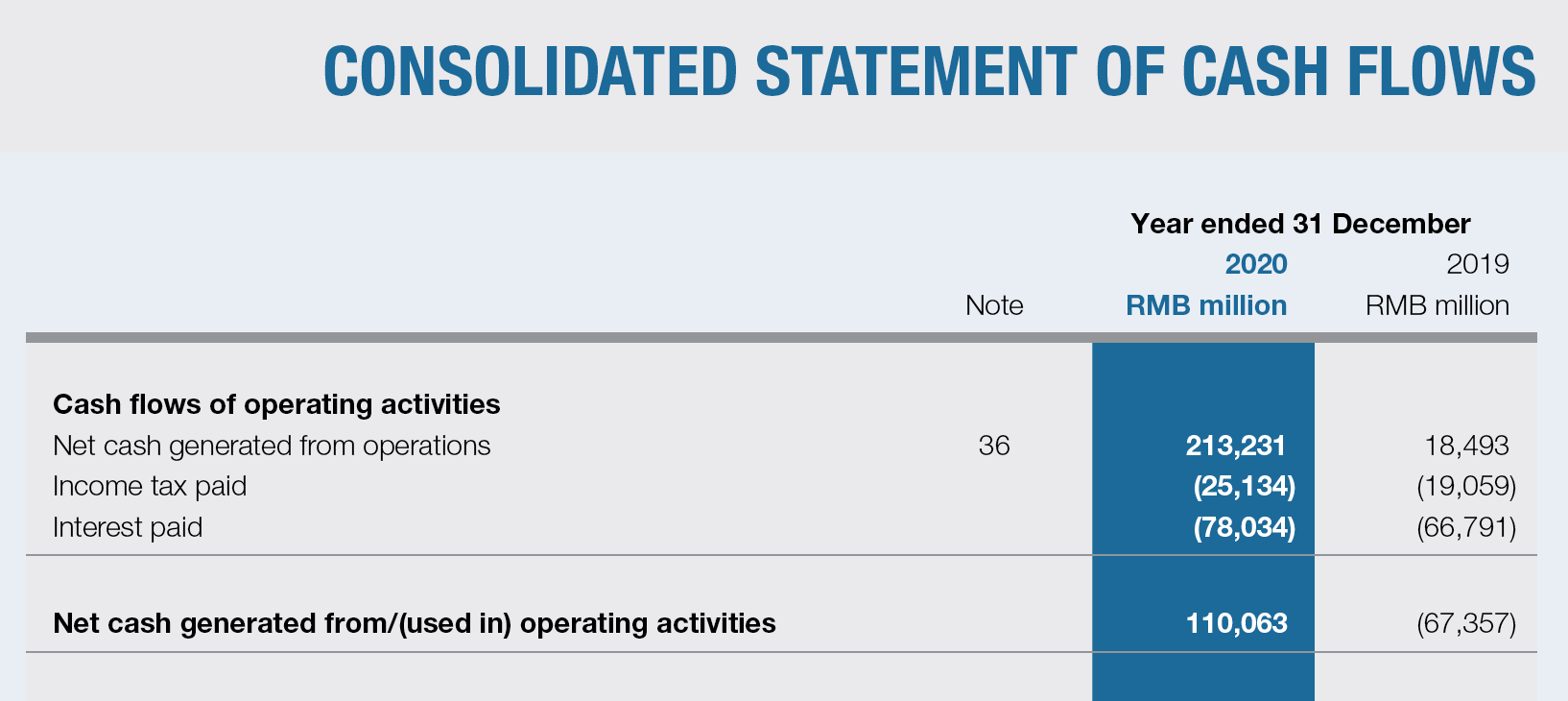

So here’s the thing about Evergrande’s cash flow - there is none. As we can see, in the past 7 years (I only used 7 years because there’s no space to show all years here) there has only been two years of positive OCF/FCF. I’m treating OCF and FCF as equal here because Evergrande’s depreciation/amortization amounts are negligible (FCF = OCF - depreciation).

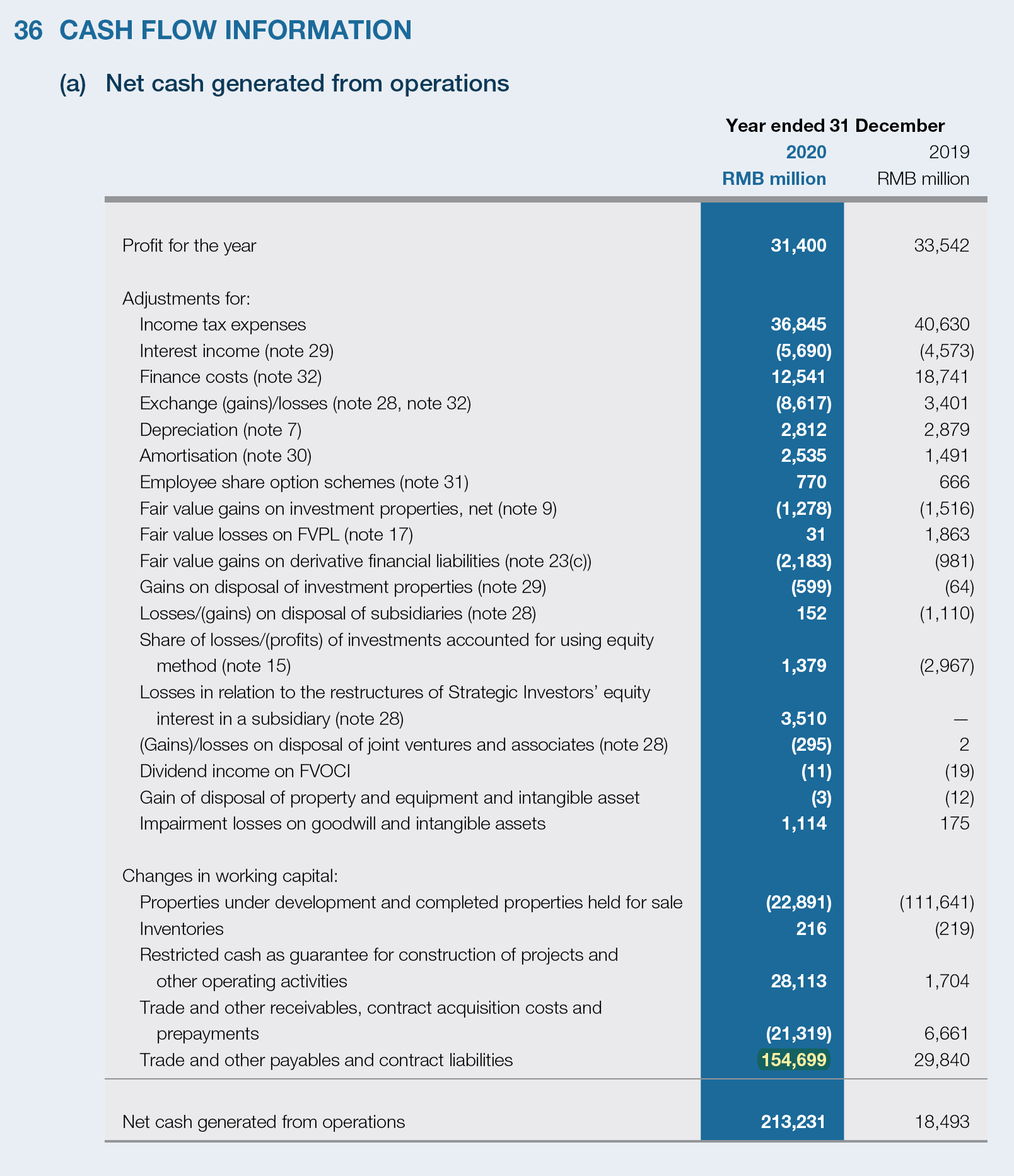

Notably, there is also another line item of interest called Net Cash Generated From Operations (NCGFO). What makes this particularly interesting is because this is how Evergrande presents its Operating Cash Flows:

And then it goes on to disclose the details of NCGFO in note 36:

Maybe it’s just me not having much experience with analyzing Chinese companies, but I’ve never seen a company split its disclosure of OCF into the notes before. This is why NCGFO was interesting. Anyway, moving on.

In both the years of 2018 and 2020 when its OCF was positive, it was because of the presence of large amounts of changes in Trade and other payables and contract liabilities. So the OCF was only positive in those years due to working capital adjustments.

In other words, we can basically say that Evergrande has never reported a positive OCF before since its listing (there was one time in 2009, but that was also because of large changes in trade payables (lol). Which is a little strange, considering that it has also been consistently profitable in every year since its listing. Considering how there should be only timing differences between Net Profit and OCF, it strikes me as suspect how they have been able to regularly post both positive NP and negative OCF for literally over a decade.

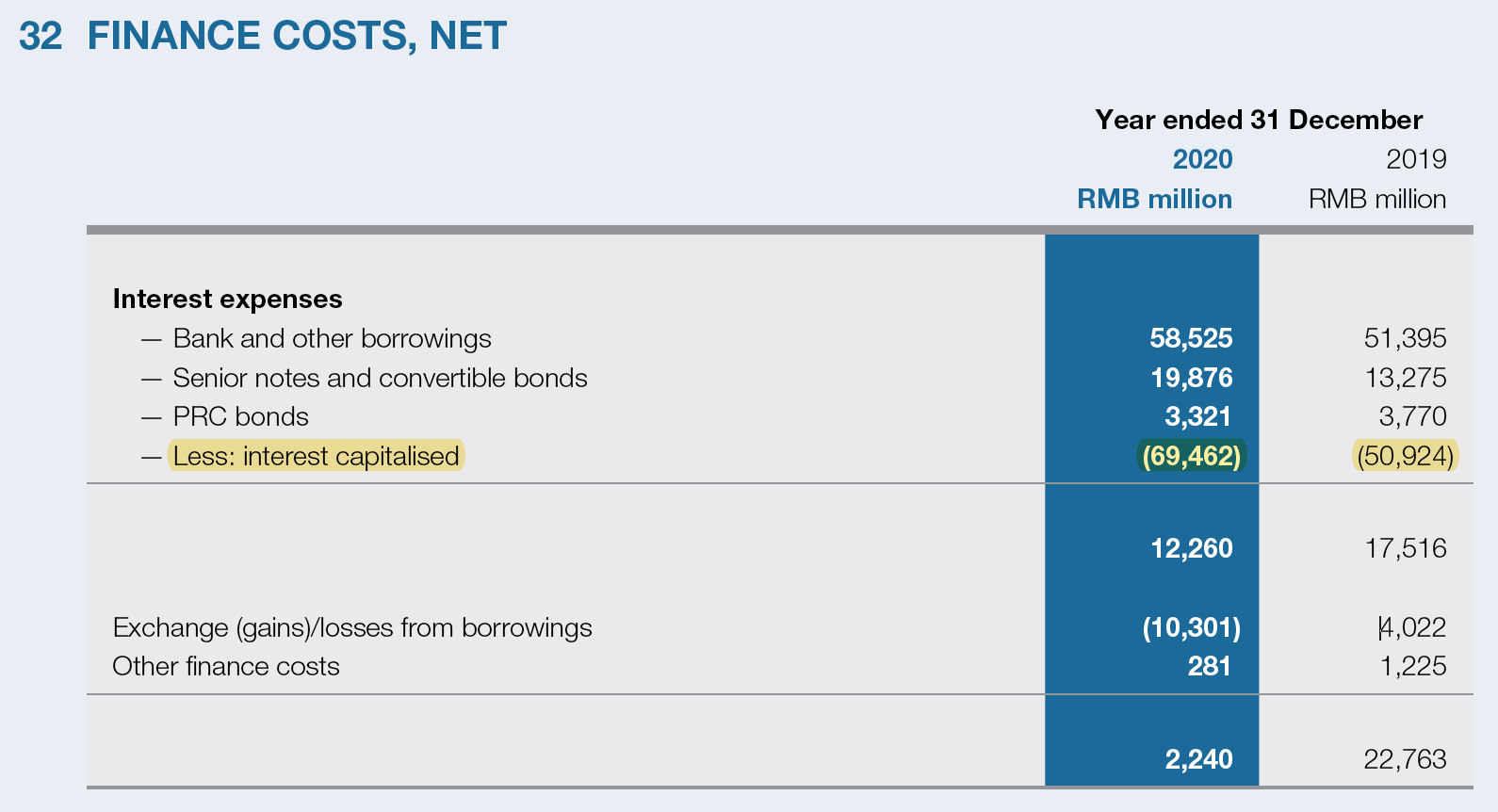

Digging deeper, we realize that the culprit of Evergrande’s consistently negative OCF is actually Interest Paid:

Which again is weird, since the ratio of Interest paid/Interest expense is ginormous:

What makes up this difference? Mainly capitalized interest expense:

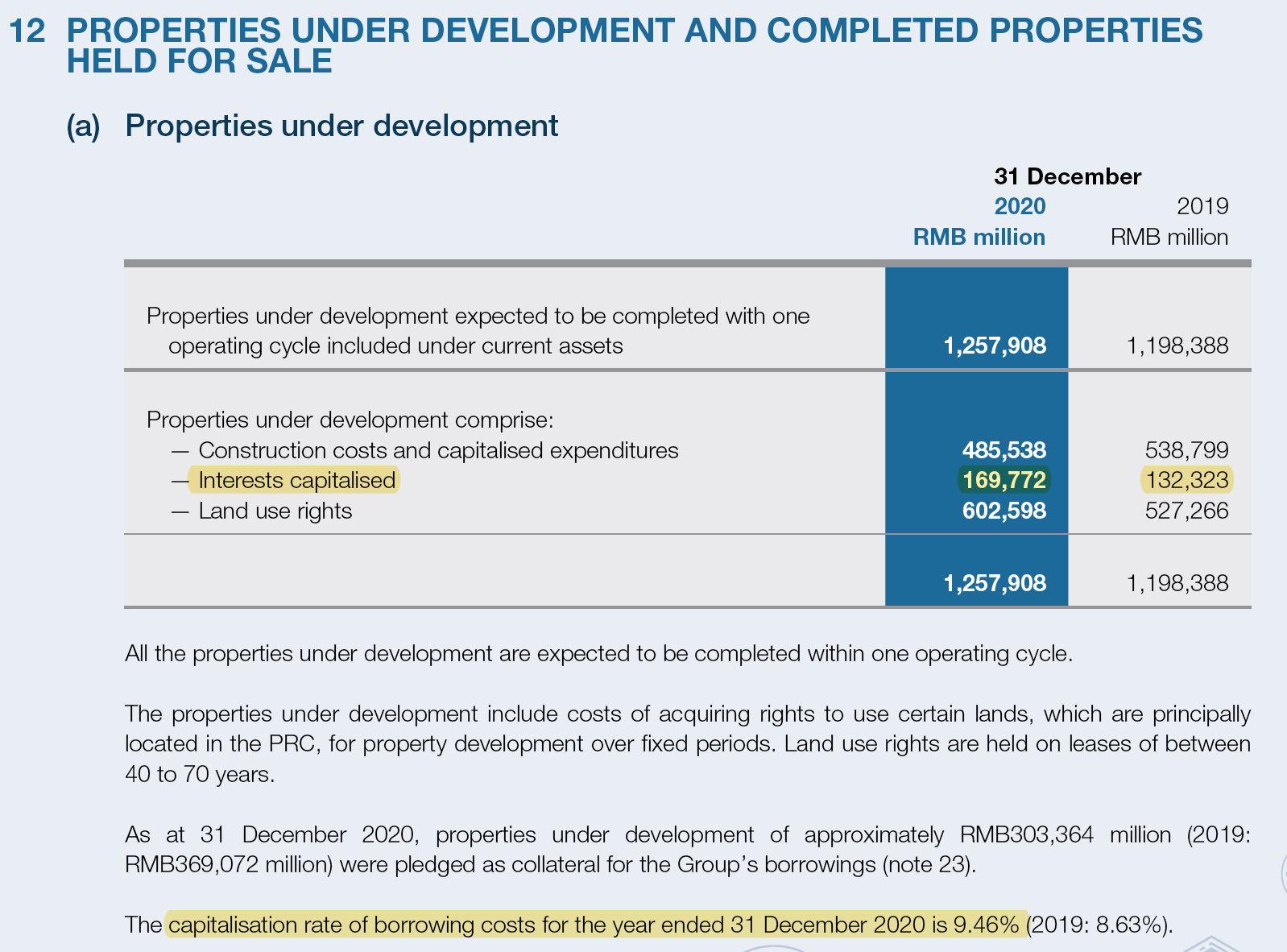

Where are those capitalized interest expenses being capitalized to? Properties under development (PUD):

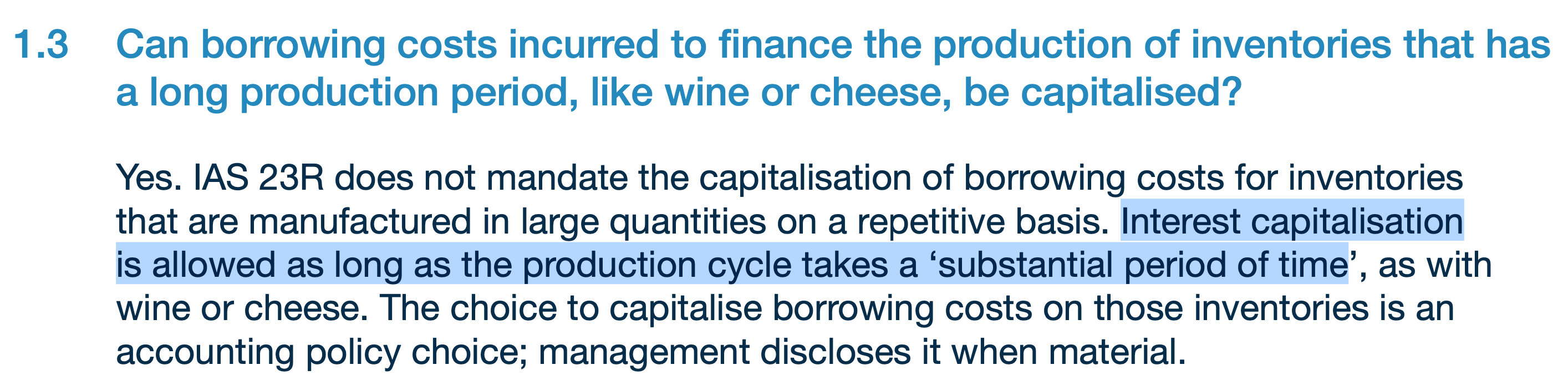

Are they allowed to do that under accounting standards? According to Page 3 of this PWC report, yes:

The reason why I’m going through all this in such rapid-fire motion is because ultimately there is nothing fishy going on here. The capitalized interest expenses of Evergrande have been accorded legitimate accounting treatment. (but as you can imagine, it took me way longer to actually figure this out)

However, it does help to explain where all that OCF actually went. The OCF generated by Evergrande each year is being used to build more houses, and the capitalized interest alone is enough to wipe out all OCF. Which then raises the question: how many houses are they actually building??

As an angry Brit might be wont to say: a whole bloody lot, I’ll tell ya that.

The Overbuilding Conundrum

Now in case you’ve forgotten by now, the whole point of this exercise was to find out whether Evergrande was a Ponzi scheme or not. At first glance, the persistent disparity between Net Profit and OCF might lend support to that theory - since no cash is actually being generated from operations. However, as we’ve seen above, the negative OCF is actually he result of massive amounts of capitalized interest, and we can actually afford to give them the benefit of the doubt.

However, what we can clearly observe is the fact that they are severely OVERBUILDING! Firstly, how do you accumulate 4 years worth of housing inventory, when the typical low-performance baseline for the industry is being unable to sell an overhang unit within 90 days after completion? Secondly, how on earth do you generate enough capitalized interest expense to be able to wipe out ten year’s worth of OCF like clockwork? At RMB 169,772 million of capitalized interest expense and the stated 9.46% capitalized interest rate (pic above), does that mean that the principal balance of the borrowings involved on capitalized interest alone amounts to RMB 1,794,630 million?? (i.e. almost RM 1.8 trillion, or USD 277 billion)

I’m going to be completely honest, I actually tried to reconcile this staggering figure with the asset side of their balance sheet, but wasn’t able to derive anything conclusive. Their Total Liabilities in FY20 amounted to RMB 1.95 trillion, while their Total Borrowings only amounted to RMB 717 billion — so how on earth are they capitalizing interest expense on RMB 1.8 trillion of liabilities? I’d imagine most of these capitalized interest expenses are coming from those aforementioned “Trade Payables to third parties” and “Cash Advances from Non-Controlling Interests”. Three red lines, my donkey.

So let’s sum up everything that we’ve just discussed and tie it into a neat little bow. Is Evergrande a Ponzi scheme? I would say no.

First of all, their low receivable days actually suggests that they are regularly transforming accounting Revenue into cold hard Cash — likely because of their pre-sales business model. It is also incorrect to say that they rely on incoming cash from new investors to repay obligations to old investors (i.e. Ponzi scheme), since their OCF ex-capitalized interest is actually hovering at acceptable levels (for Evergrande):

However, what we can say with a high degree of confidence is that their capitalized interest expense is way too high for comfort - and therefore that they are overbuilding way too much for comfort. So even though they aren’t actually engaged in a Ponzi scheme, I think there are similarities between its overbuilding and an actual Ponzi scheme.

Recall the business model that I suggested earlier:

Evergrande starts by borrowing a certain sum to build the first house

Before that house has been completely built, it would sell the house to a home buyer (i.e. pre-sale).

Using the cash inflow from that pre-sale as collateral, it would turn around and borrow more money. (even before the first house is completed)

This money would then be used to build a second house.

Rinse and repeat.

Again, the problem here is that if the new money earned from the pre-sale of the first house is used to build the second house… where will the money to repay the borrowing for the first house come from?

The way I think that Evergrande keeps the story running is by borrowing even more. By borrowing even more, they can now use those newly borrowed funds to repay old investors - and then keep refinancing those borrowings into perpetuity. We can see this trend below in how Borrowings growth far outstrips Revenue growth (because they never actually repay those old borrowings). We’re going to leave out Payables growth for now, although the portion that reflects commercial bills should also be included too:

This illustrates how without a constant revolving door of investors to keep the investor treadmill running, the entire house of cards collapses on itself - similar to a Ponzi scheme. However, it should also be made clear at this point that Evergrande wasn’t selling vaporware - it managed to eventually sell the houses that it built, and money was eventually earned to repay its investors. So it’s also not true that they exclusively relied on new investors to repay old investors, i.e. a Ponzi scheme.

Unfortunately for them, that eventually usually meant about 3-4 years later - which means that they were significantly overbuilding. This is evidenced by their outrageously high Inventory Days, which regularly exceeded 4 years. So while they were not engaged in an actual Ponzi scheme, they usually found themselves short on cash to repay old investors because they had overbuilt - and would need to raise more money from new investors in order to repay old investors in the meantime. Fundamentally, it is an overbuilding issue; because if they didn’t overbuild, they actually would have the cash on hand to repay old investors, and wouldn’t need to borrow more.

Since Evergrande’s revenue is accounted for based on the percentage of completion method, an inflated COGS would actually lead to higher revenues. This gives management perverse incentives to encourage overbuilding in order to maximize revenues. As long as they can keep the investor treadmill running, everything would be fine. But once new investors stop entertaining their calls for more funding, they would no longer be able to repay old investors without liquidating all their overbuilt Properties Under Development. This is exactly what is happening with Evergrande today.

It is widely recognized that Evergrande isn’t facing a solvency issue so much as it is facing a liquidity issue. If Evergrande were given sufficient time to process an orderly liquidation of their assets, they would actually have the ability to pay back their debts in full. The problem today is that they have to pay back their debts now; and if they had to perform a fire sale of assets at 50% of book value in order to meet current debt redemptions, they would likely be unable to fully service those debts.

In summary, we can conclude that Evergrande’s woes are fundamentally an overbuilding issue, and that it’s not a Ponzi scheme.

Now that we’ve understood the nature and source of Evergrande’s problems, we can actually take a gander at what its future might look like. In Part 2, I’ll be exploring what fate holds in store for Evergrande in the next 6 months - including pressing questions such as:

Will Evergrande get bailed out?

How high is contagion risk from an Evergrande fallout?

What is the current state of the Chinese economy as it relates to Evergrande?

What might the next moves of Chinese policymakers likely be?

Should you buy/sell Evergrande’s shares today?

For the answers to all these and more, click the link below to read Evergrande Part 2!

Interesting reading:

VIC writeup on Evergrande | Asian Century Stocks’ Michael Fritzell (2018)

How Evergrande could turn into China's Lehman Brothers | Nikkei Asia

What Does Evergrande Meltdown Mean for China? | Michael Pettis

Interview with Jordan Schneider of ChinaTalk | Compounding Curiosity