ROIIC, Pricing Power & The Outsider CEO | DISNEY Financial Deep-Dive (Part IV)

“This boils down the entire Disney financial analysis to just one all-encompassing financial metric — How & Where can Disney invest to generate ROIIC?”

Table of Contents (Part 4):

In William Thorndike’s seminal value investing manual The Outsider CEOs, the author does the equivalent of a PhD study which seeks to identify what CEO leadership traits deliver the greatest LT share price outperformance. The starting point of his study begins with two extremely high criteria: 1) the share prices of the companies run by qualifying CEOs had to outperform GE’s during the tenure of its legendary CEO Jack Welch; and 2) outperform the share prices of their own industry peers during each candidate’s respective long-term tenures as CEOs.

However, the results of his study were utterly surprising — each of the 8 CEOs he profiled shared very “Outsider” leadership traits which challenged the premise of corporate America’s status quo. These traits included an undying focus on maximizing ROIC over growth, a willingness to shrink for efficiency, adopting a measured, logical approach to operations — and most importantly, making Optimal Capital Allocation the first priority in corporate strategy.

These leadership traits stood in stark contrast to the status quo of corporate America, which celebrated more traditional leadership traits such as charisma, vision, risk-taking and hustle culture. Despite that, all 8 Outsider CEOs were some of the best-performing CEOs in the entire history of modern corporate America. They include:

The 8 Outsider CEOs:

Warren Buffett: CEO of Berkshire Hathaway Inc.

John Malone: CEO of Tele-Communications Inc. (TCI)

Henry Singleton: CEO of Teledyne Inc.

Katharine Graham: CEO of The Washington Post Company

Tom Murphy: CEO of Capital Cities Broadcasting Corporation

Bill Anders: CEO of General Dynamics Corporation

Dick Smith: Founder and CEO of General Cinema Corporation

Bill Stiritz: CEO of Ralston Purina Company

Shared Outsider CEO Traits:

They were all long-term thinkers who focused on creating enduring value.

They were all value-conscious and disciplined in their capital allocation.

They were all decentralizers who empowered their employees to make decisions.

They were all frugal and mindful of costs.

Most people would have recognized Warren Buffett and John Malone in the list above; diehard value investors will also recognize Henry Singleton of Teledyne, Tom Murphy of Capital Cities and Katherine Graham of the Washington Post — all dear friends of Buffett.

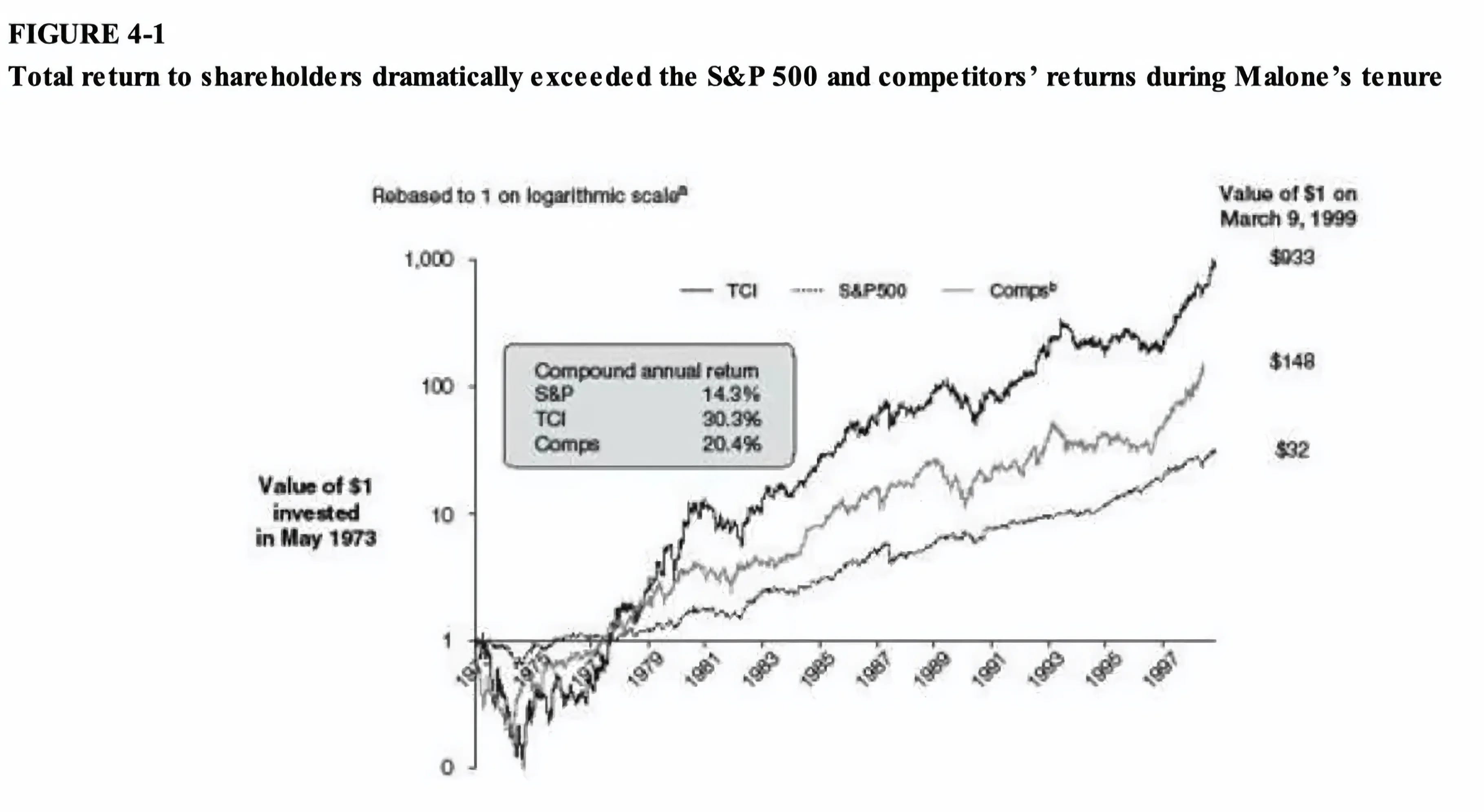

Malone was the subject of our Disney Part 1 report, where he explored how his cable company TCI rewarded its shareholders with 30% CAGR over his 25-year tenure as CEO — beating even Buffett’s record at Berkshire. We also noted similarities between some of the things which he implemented at TCI (that led to its success) to the things that Disney CEO Bob Iger is currently institutionalizing at Disney+ today.

Readers of Malone’s bestselling biography Cable Cowboy will also recall how Malone employed the structural benefits of economies of scale in the Cable industry to its full extent in order to drive down unit costs — culminating in TCI gaining quasi-monopoly bargaining power over its customers and suppliers. He pioneered both the use of EBITDA and the incredible “Aggregator Moat” of the Cable industry, which served as the bottleneck of the entire industry and made Cable companies one of the best businesses to own during his generation (prior to its disruption by Streaming).

With Disney+ already engaging in Rebundling and the rest of the industry following suit, there is overwhelming evidence that the natural trajectory of the modern-day Streaming sector will likely climax in the same impenetrable “Aggregator” moats for the two sector incumbents — Netflix and Disney+. The implication here is that there’s a good chance the US Media industry will eventually consolidate around a duopoly, with the two sharing over 50% market share together.

As we shall explore further in this report, Disney’s Streaming business (DTC) is likely to experience Pricing Power going forward following its Rebundling destiny. Much of the Pricing Power generated under Disney’s DTC and Experiences segments are a function of management’s ability to implement Optimal Capital Allocation in order to maximize value at each respective business. In this Part 2 report, we’ll see how Iger can apply this “Outsider’s” approach to ROIC in each of its respective business segments — Entertainment, Sports and Experiences.

Iger’s recent contract extension to end-2026 reflects the board’s confidence in his ability to see Disney through the necessary internal revolution that Disney+ will need to implement in order to transition to DTC. If he can successfully mitigate the execution risk, he will be laying the foundation for Disney to catapult to the apex of the US Media industry — perhaps with global ambitions in store for his successor after he steps down in end-2026. The magnitude of the changes in store until Iger’s departure is so dramatic that I firmly believe that Iger’s legacy has the potential to match that of John Malone’s — and compete for the latter’s title of Cable Cowboy (or Streaming Spirit). One thing Disney shareholders can be dastardly sure of — your company will be barely recognizable by end-2026.

As we saw in Part 2, when Buffett acquired his initial stake in KO 0.00%↑ at 15x-29x PE in 1988 and 1989, it was still a failing conglomerate which had spread itself thin across a mishmash of industries. However, Buffett saw what everyone else didn’t at the time — its internationally scalable Coca-Cola brand. Disney today has similar business potential baked into its beloved Disney-branded entertainment IP library — especially given the new global scalability of the Streaming industry.

Similarly to KO in 1988, Mr Market is overly concerned today with Disney’s ST underperformance to see what will be obvious to any scuttlebutting Disneyland guest — a wealth of valuable Intangible Assets with a practically infinite shelf life, and whose Brand value to consumers literally transcends generations. As Disney’s CEO, Iger is poised to reintroduce Disney’s beloved characters to an entire new generation of consumers worldwide, who will hold them dear in their hearts for life — and become the engine of Disney’s growth until the turn of the next generation. China, India, Indonesia, watch out… Mickey Mouse is coming for you.

History doesn’t repeat itself, but it rhymes. This is the story of Iger’s Coca-Cola moment.

Bob Iger on his predecessor Michael Eisner, in his autobiography The Ride of A Lifetime:

Michael’s biggest stroke of genius, though, might have been his recognition that Disney was sitting on tremendously valuable assets that they hadn’t yet leveraged.

One was the popularity of the parks. If they raised ticket prices even slightly, they would raise revenue significantly … building new hotels at Walt Disney World [and] expansion of theme parks.

Even more promising was the trove of intellectual property — all of those great classic Disney movies — just sitting there waiting to be monetized. They began selling videocassettes of the classic Disney library to parents who’d seen them in the theater when they were young and now could play them at home for their kids. It became a billion-dollar business.

… the Cap Cities/ ABC acquisition in 1995, which gave Disney a big television network, but, most important, brought in ESPN.

(big thanks to TSOH for bringing this wonderful quote to my attention)

IGER: Post-Cable Malone (Disney Part 1)

This is the Disney Part 3 report. Click here to read the Disney Part 1 report.

DISNEY: What If You Could Buy Coca-Cola Together With Buffett In 1988? (Part II)

$DIS is trading at 20x Parks EBIT (ex-Media) ALONE. How is Parks EBIT still growing at 16% CAGR? Pricing Power. And is Streaming at an inflection point to turn into a "Profitable Growth" business?

DISNEY: A Misunderstood Compounder with ESPN's Brand Moats & Parks' Pricing Power (Part III)

Financial Deep-Dive into 1) the Branding Moats of ESPN: The Netflix of Sports and 2) the Engines of Pricing Power behind Experiences

I want to give a huge shoutout to Alex from The Science of Hitting Substack (TSOH), who very graciously allowed me to lean on his research while analyzing Disney. His incredibly detailed insights into Disney were extremely helpful in conducting my research, and I will be generously linking back to his articles throughout my report. I consider TSOH as the premier investment newsletter for Big Tech on Substack; in the same way that I consider SemiAnalysis for Semiconductors. Please visit his newsletter at the link above and show your support to him.

Click the Sections below to see our latest articles!

KPI: Conceptualizing ROIC in the Parks & Media Businesses

ROIIC = incremental Net Profit (NP) / incremental Invested Capital (IC)

IC = Total Equity + Net Debt

ROIIC stands for Return on Incremental Invested Capital. A positive ROIIC means that for every dollar of incremental invested capital, the company needs to generate incremental profits with at least the same yield (ROIC) or higher. In financial terms, a positive ROIIC would imply future ROIC remaining steady or climbing (i.e. not declining).

Disney has recently introduced a newly reorganized reporting structure, splitting its former DMED segment (Media) into two distinct segments: Entertainment & Sports. Meanwhile, much of its former DPEP segment (Parks) is now under a similar reporting structure: Experiences. The carving out of Sports as its own distinct Media segment demonstrates how management and the board thinks about ESPN’s significance towards Disney’s future.

To understand where Disney has further room to generate ROIIC and improve business efficiency, we first need to understand what that could look like in practical terms. In this section, we’ll do a deep-dive into the various domains where Iger can best exploit untapped opportunities for incremental cost optimization and sustainable growth amidst Disney’s sprawling and diverse businesses.

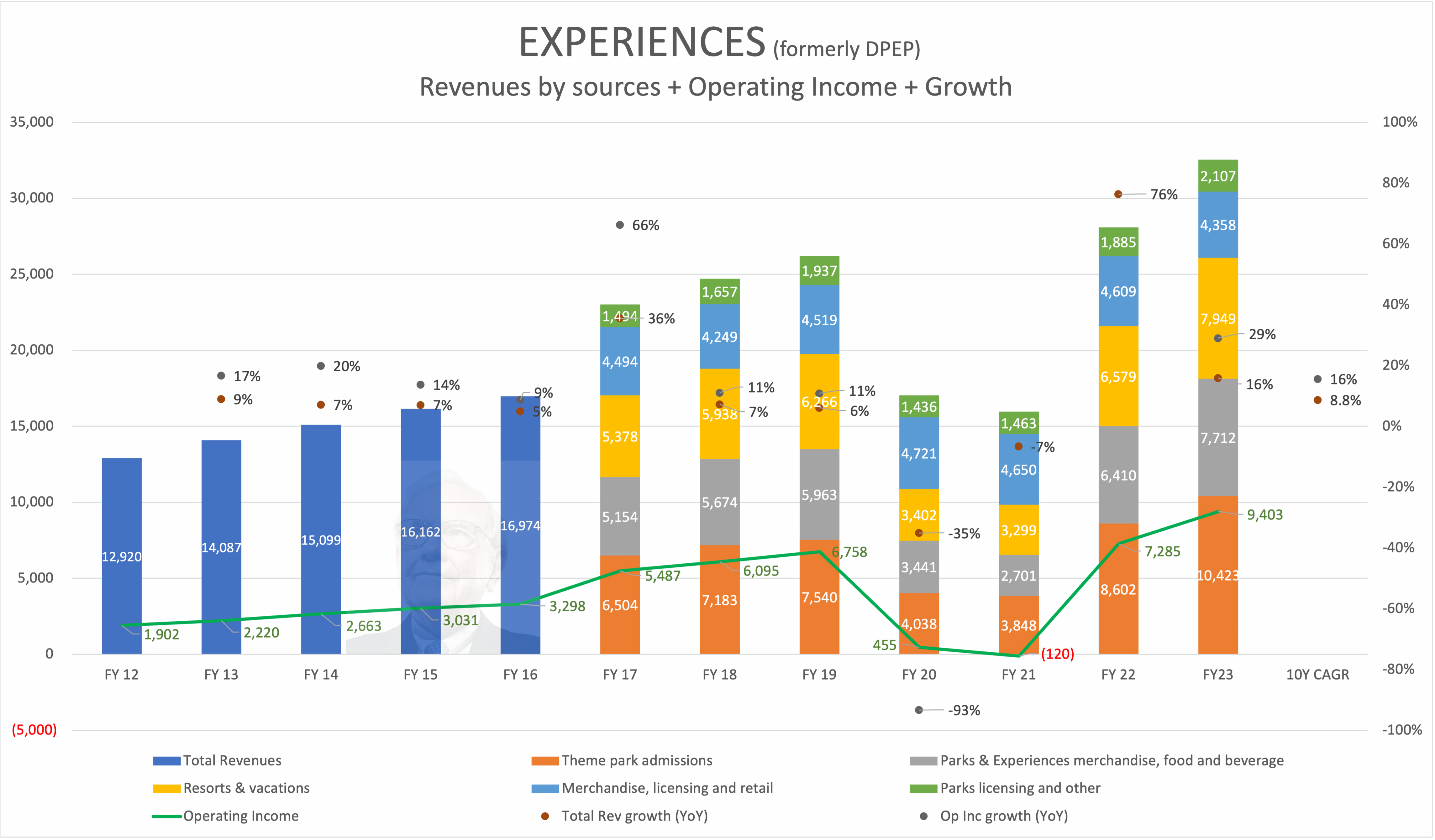

Experiences (Parks)

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.