✨ Berjaya Corporation (BJCORP: 3395.KL) - Part 1

Radio show host: "What do you think BJCORP's shares are worth? Between RM 5.00 - RM 10.00?" CEO: "Yes. Closer to RM 10.00." Current share price: RM 0.25

BJCORP’s new CEO Jalil joined the company in March 2021, and has been public about how he thinks its shares are severely undervalued. The investment thesis for BJCORP is a turnaround thesis.

Despite looking like a conglomerate on the surface, >80% of BJCORP’s revenue actually comes from the Consumer sector - which dramatically increases the feasiblity of the turnaround, compared to a traditional conglomerate.

BJCORP was very badly run in the past - hence the base-case scenario is for them to simply return to industry baseline performance. No magic tricks are expected from the new management team.

If they can do that, the conservative 5-year CAGR estimate is north of 40%; while the optimistic 5-year CAGR estimate is up to 70%.

Did you know that BJCORP has listed long-term warrants? You can juice up the above returns even further, while adopting only marginal incremental risk.

In his short time at BJCORP, Jalil has demonstrated himself as a capable business operator, with a significant focus on prioritizing optimal capital allocation - arguably Buffett’s topmost key performance metric.

Company Links:

“You can absolute make the same amount of money in Emerging Markets like ASEAN as you can from more developed markets like the USA or China - because of the existence of significantly less market competition.”

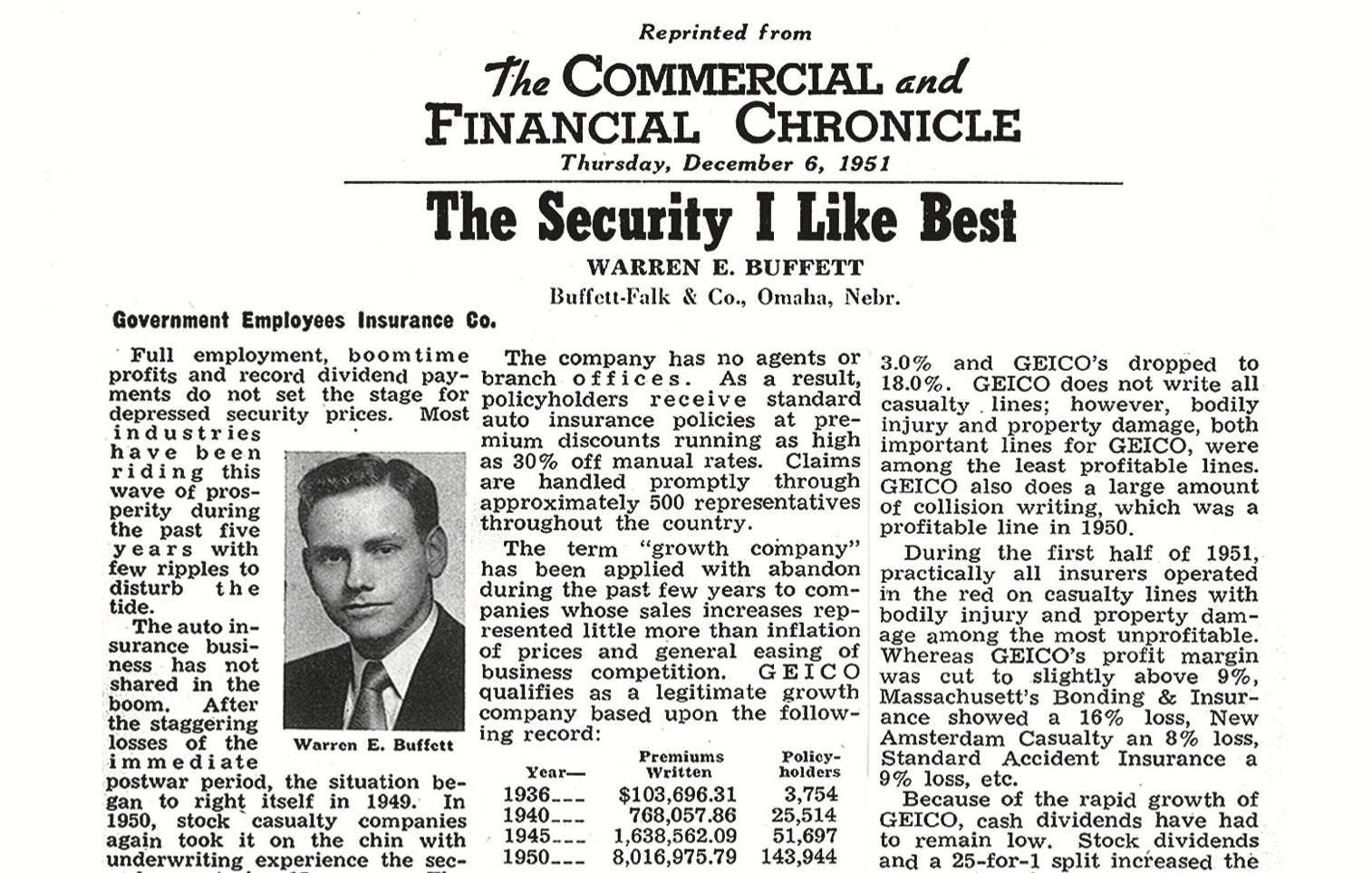

In 1951, a mild-mannered young man by the name of Warren E. Buffett wrote an article in The Commercial and Financial Chronicle newspaper titled The Security I Like Best. The security he was profiling was none other than GEICO, the insurance company which exclusively served government employees at the time - contributing to its significant cost advantage versus its peers. Today, GEICO serves as one of the approximately dozen pillars within Buffett’s $600B empire Berkshire Hathaway, providing the long-touted insurance float which has been said to have contributed up to 50% of the entirety of Berkshire’s historical returns.

While I’m not trying to allude to the notion that Berjaya Corporation’s (BJCORP) outlook shines anywhere near as brightly as GEICO’s did then, it is most certainly the ASEAN security that I like best today. The current share price can only be described one way - mispriced - where the presence of the Efficient Market Hypothesis (EMH) is completely absent. The bid and ask prices of its shares today may as well be set by a 5-year old chimpanzee throwing darts at fish in a barrel, and this is a sentiment shared by others as well.

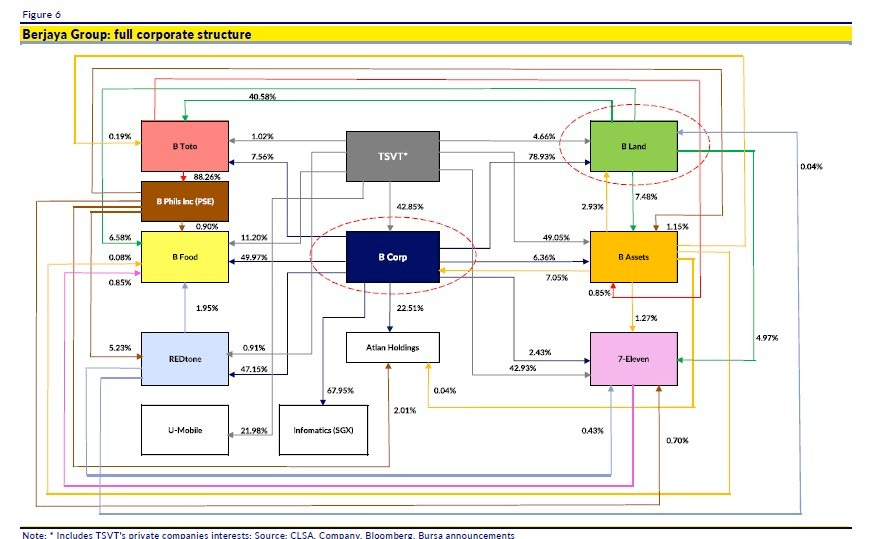

To be fair, this is by far the largest small-cap company I have ever come across, for the simple reason that this company is actually a conglomerate - but whose share price has since fallen to small-cap levels. BJCORP is actually the parent company of all the listed Berjaya companies owned by the founding Tan family (‘berjaya’ means ‘success’ in Malay), as evident by the mindboggling complexity of its ownership structure:

As you can see from the chart above, this web of entangled ownership shared between all the listed Berjaya companies is an absolute nightmare to untangle. I’d like to take this opportunity to apologize to all my loyal readers for going MIA over the past two weeks - because the more answers I sought from this company’s financial statements, the more questions it begot; and I ended up tunneling into rabbit hole after rabbit hole trying to find answers for the new questions that kept cropping up.

In many ways, my learning experience when analyzing this company resembled my learning experience when I was first studying macroeconomics - visualized as trying to understand many individual pillars of knowledge, but where you needed to understand some parts of other pillars before you could fully comprehend the one you were currently on.

In the end, I decided that it was futile trying to develop an airtight comprehension of this conglomerate’s financials in a reasonable amount of time - and decided that I would just type out whatever I had already analyzed in Part 1, while leaving the rest for Part 2. Rest assured that I fully intend to make up my research report quota by the end of the year.

For the sake of visualization, Part 1 will compose the entirety of the bull-case investment thesis and its context; while Part 2 will do a deep-dive into the relevant listed Berjaya companies to provide further insight into the dark, arcane blind spots that might reside within its accounts, and figure out where the upside may lie. Without further ado, let’s get spelunking.

Introduction

The investment thesis behind buying BJCORP’s shares today can be described as being a turnaround. For the uninitiated, a turnaround refers to a corporate exercise where new capable management is brought by shareholders into a dying company to revitalize it, and breathe new life back into its desiccated corpse. For obvious reasons, being an investor in successful turnarounds can be extremely profitable, as the share price of the company prior to the successful turnaround is likely to be depressed. But at the same time, successful turnarounds are quite rare, as poor businesses tend to be poor for good reasons.

As such, most investors tend to shy away from investing in turnarounds as the uncertainty involved is usually high. If you’ve read my earlier report about Why Value factor investing > Growth factor investing, you’ll understand what I mean when I say that investors hate uncertainty - because it makes the future difficult to forecast:

However, I would consider BJCORP’s turnaround a little different from the generic definition of the term. When most people talk about turnarounds, they tend to refer to the sort of monumental endeavor which involves lifting mountains to turn a gigantic 100,000 ton ship around by 180 degrees in a split second - e.g. Pat Gelsinger’s effort to salvage Intel after losing market share to AMD for a decade; or Joe Papa being invited to revive Valeant after its infamous bust under Mike Pearson.

Compared to that definition, I think the more accurate way to describe BJCORP’s requirements would be “clean-up” - rather than “turnaround”. Rather than requiring some sort of spiritual reevaluation in the corporate ethos, all BJCORP needs is a little spring cleaning of their dusty storeroom. All the ingredients for success are already in place - the only change that needs to be implemented is a reorganization of the wares which are already sitting on the shelves, rather than requiring an order of a new batch of inventory. The reason for this is very simple - BJCORP used to be very badly run (for reasons which I’ll go into below), and all they need to do to get things back in order is to return to industry baseline performance, and give the existing business assets a chance to shine.

So if that’s the case, what has changed in the past few months to warrant such a drastic revaluation of the business? The answer is the new CEO Jalil Rasheed (LinkedIn), who announced his entrance into the company in mid-March of 2021. In the 2nd quarter of 2021, he went on a buying spree of BJCORP’s shares - and now owns approximately 3.6% of the company’s outstanding shares:

While Jalil’s resume does carry some substantial pedigree (he used to be the CEO of one of Malaysia’s sovereign wealth funds PNB), the successful execution of this investment thesis does not rely on the masterful capabilities of a Steve Job-esque genius to pull off. Rather, all it takes is someone with a good head on his shoulders, and has the baseline capabilities to operate as a CEO of a large listed company. In that context, I have ample confidence that Jalil is more than capable of delivering.

Before we dive headfirst into the investment thesis, I would just like to leave you with something to ruminate over as we pour over the analysis of BJCORP. In mid-July 2021, Jalil gave an interview on the most popular local business radio station BFM. At the 35:42 mark of this interview (navigate to the 35:42 timestamp), the host asked him point-blank what he thought BJCORP’s shares were worth.

Jalil answered very confidently - between RM 5.00 to RM 10.00, and perhaps closer to RM 10.00. Keep in mind this is a stock which is currently trading at roughly RM 0.25, implying an approximately 30x upside if we assume the lower bound of that range of RM 7.50:

I understand that the potential for conflict of interest exists in his words, but that is just an unnecessarily way-out-there share price target to provide accountability on. In fact, if Jalil was in fact trying to push the stock with that sentence, I’d wager that he actually failed to achieve his objective - by virtue of the fact that people will wonder whether he’s insane. Which means that there is likely some merit to his estimate of BJCORP’s intrinsic value. Also take a look at some recent crazy insider buying activity by BJCORP’s founder Tan Chee Yioun in the above screenshot.

If you want a bit more context behind his estimated target price of RM 7.50, I’d recommend rewinding back to a slightly earlier timestamp of the same interview. At the 34:07 mark, the host provides a summary of the entire interview, which adds a bit more color about why Jalil might think that BJCORP’s shares are worth 30x what they are currently trading at (3,000% upside). I’d highly recommend just listening to this insightful interview in its entirety.

For more insight into Jalil’s management style (by the way, he’s only 39), you can also have a look at his excellent Twitter thread here:

Also to learn more about him as a person, check out this very classy recent interview with him in a local celebrity magazine:

As I’ve alluded to earlier, the research scope of this conglomerate is so much more vast than your average Malaysian small-cap, that I genuinely do not believe it will be the best use of your scarce reading time to expound on the entirety of BJCORP’s financial context in Part 1 of this report. Instead, I will focus on delivering the investment narrative in Part 1 as efficiently as possible (this report is already 10,000 words long) - and then provide a further deep-dive into their MD&A and notes of their latest annual report in Part 2, for those who want more financial context to Part 1’s investment narrative. Given BJCORP’s share price performance over the past few months, I find it extremely unlikely that its share price will jump in the space of a week or two anyway.

Hence, the way I’ve decided to structure Part 1 of this research report will be as follows:

Background of the company - to provide historical context until Jalil’s appointment as CEO in March 2021

Jalil’s management style and his corporate strategy for BJCORP

Financial analysis of BJCORP's financial statements - from their annual report

When I’m done, you’ll understand why it took me two weeks to research this company and 10,000 words to type out Part 1 of this report.

(The above links which jump to the relevant chapters will only work in the desktop version of Google Chrome. If you’re using a different browser, please scroll to the relevant chapters below.)

Black Friday SALE! Get more ASEAN stock ideas like this and access to all our previous research reports for 10% off! Limited time only… promotion ends in 3 days!

Background of BJCORP

Get a 30-day trial for FREE to read the rest of this 10,000-word report by clicking this button!

As you can see above, BJCORP is a large company with a corporate empire that spans several sectors. Analyzing a conglomerate is equivalent to analyzing 5-6 different companies, since each sector has its own idiosyncratic characteristics.

Keep reading with a 7-day free trial

Subscribe to Value Investing Substack to keep reading this post and get 7 days of free access to the full post archives.